Broadcom Plunges Nearly 14% After Hours, Is It an AI-Created Golden Pit or a Waterfall Coming?

Broadcom's Q2 revenue grew 48% year-over-year to $22.2 billion, with AI semiconductor revenue reaching $10.8 billion. Despite strong financials and robust cash flow, the stock fell sharply as AI guidance, though forecasting over 200% growth, missed analyst estimates. Management confirmed a focus on "chips only," impacting expectations for integrated systems. The sell-off was attributed to excessively high market expectations rather than fundamental weakness, with significant order backlogs extending to 2028 and unchanged long-term AI revenue targets reinforcing underlying strength. Analysts largely maintain positive ratings, seeing the pullback as a buying opportunity.

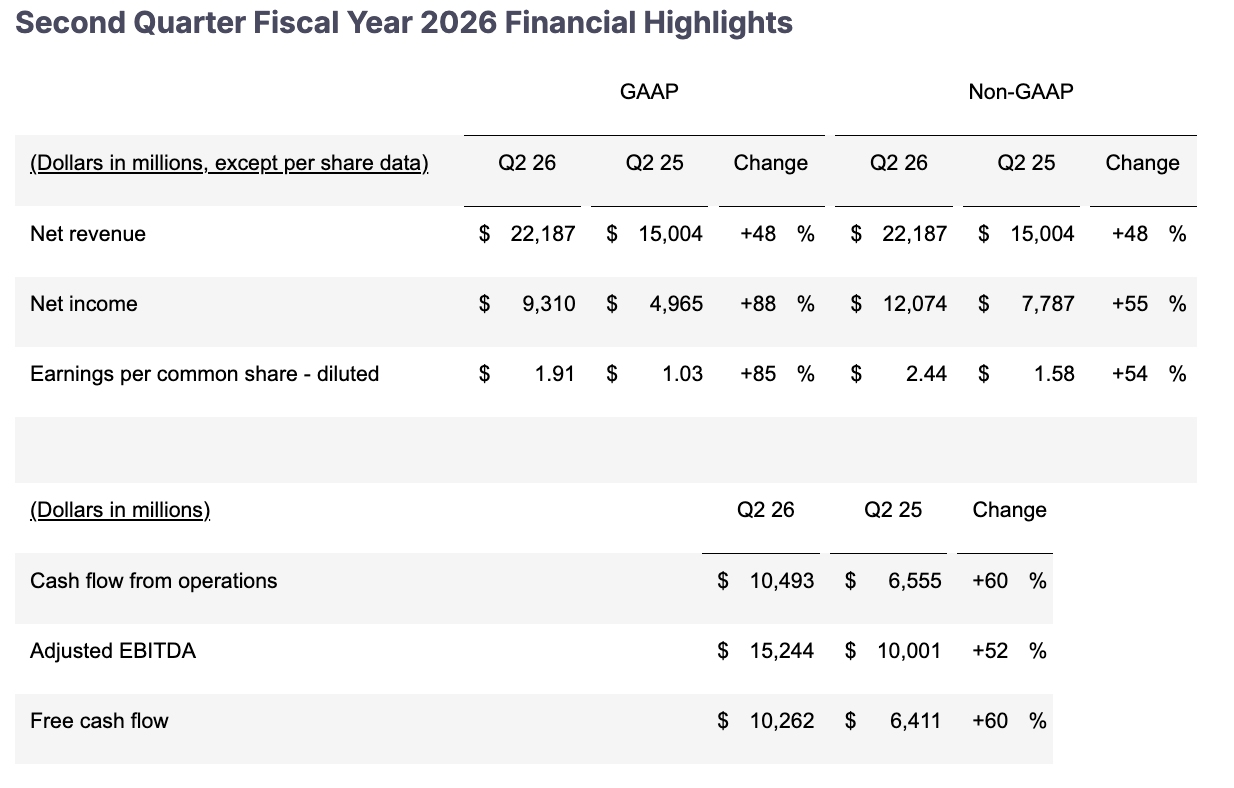

TradingKey - After U.S. market close on June 3 ET, Broadcom ( AVGO.US) shares plummeted, at one point diving more than 15% before ultimately closing down 13.78%. Financial results showed second-quarter revenue of $22.2 billion, up 48% year-over-year, the highest quarterly growth rate in nine years. Adjusted earnings per share was $2.44, up 54% year-over-year. Operating margin climbed to a record 67%, and adjusted EBITDA reached $15.2 billion (a 69% margin), both exceeding guidance.

[Broadcom Financial Data, Source: FY2026 Second Quarter Financial Report ]

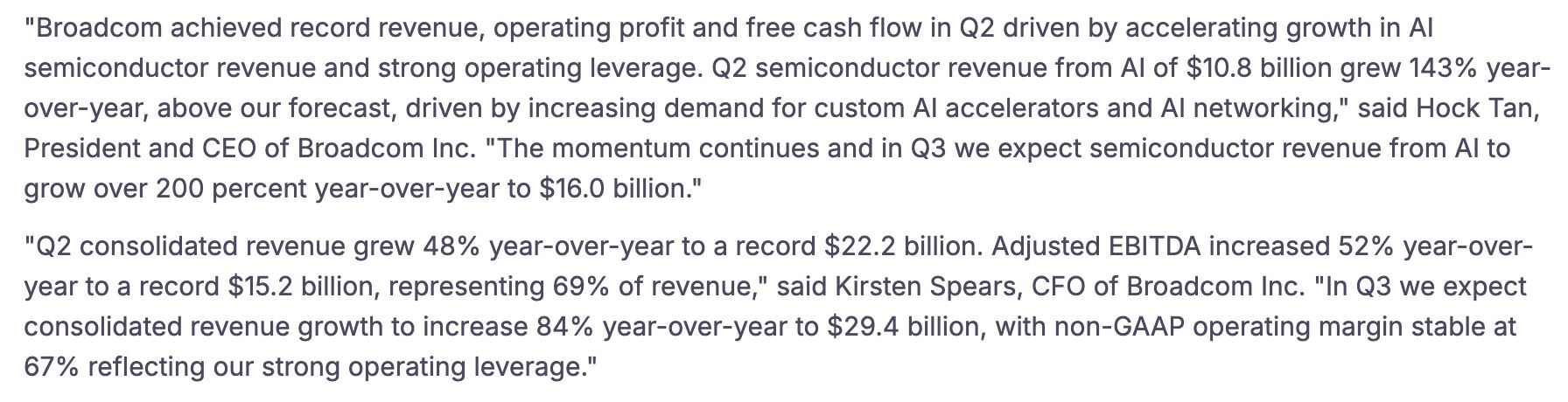

Hock Tan stated that AI semiconductor revenue reached $10.8 billion, up 143% year-over-year, marking the thirteenth consecutive quarter of positive growth and representing nearly half of total revenue.

Furthermore, operating cash flow stood at $10.49 billion and free cash flow at $10.26 billion, reflecting an extremely robust cash flow performance.

Merely meeting expectations is, in fact, falling short of market expectations.

Following the release of its earnings report, the share price suffered a massive sell-off. The crux of the issue was that market expectations were already anchored too high, and Broadcom failed to deliver the "upside surprise" that investors were looking for.

Ahead of the earnings release, the stock had surged more than 65% from its late-March low, marking a year-to-date gain of approximately 40% and adding over $300 billion in market capitalization within just five trading days. Under such a razor-thin margin for error, the market was anticipating a report that would "beat across the board," whereas the reality was merely a solid performance that was "broadly in line with expectations."

Core Divergence in Earnings Reports

The core divergence in this earnings report is concentrated on two levels.

AI guidance fell short of overly optimistic market expectations. Broadcom expects AI semiconductor revenue for the third fiscal quarter to accelerate to $16 billion, a year-over-year increase of over 200%, yet this remains approximately 7% below the consensus analyst estimate of $17.2 billion; it maintained its full-year AI semiconductor revenue guidance for fiscal 2026 at $56 billion, lower than some market forecasts of $57.6 billion.

During the second-quarter earnings call, CEO Hock Tan officially confirmed to the market that Broadcom will only provide chips in the future, rather than the complete AI integrated systems previously promised.

This strategic pivot directly impacted previous high market expectations for Anthropic-related chip projects, and the guidance provided by Broadcom failed to fully bridge this expectation gap.

Market analysis suggests that the sharp decline did not stem from weakness in the earnings report itself, but rather from the fact that market expectations for Broadcom were already extremely high; any guidance falling short of a significant beat could trigger profit-taking.

Fundamentals have not stalled.

Beyond the sell-off sentiment, the message conveyed by management during the earnings call was far from pessimistic. Hock Tan explicitly stated that "demand for XPUs and networking equipment is simply insatiable," revealing that new AI semiconductor orders for the quarter exceeded $30 billion, far outstripping the $10.8 billion in actual deliveries for the period.

Broadcom detailed for the first time its blueprint for deep integration with six core customers: Google signed long-term agreements for multiple generations of TPUs and AI networking equipment; Anthropic will secure over 1 GW of computing capacity, with an additional 5 GW starting in 2027; OpenAI has received its first batch of production chips and committed to deploying 1.3 GW by 2027; and Meta will collaborate on delivering multiple generations of MTIA XPUs, with a planned deployment of 3 GW by the end of 2028.

Hock Tan reiterated that AI semiconductor revenue will "very easily" exceed $100 billion in fiscal year 2027. Visibility for these orders already extends to 2028, and long-term fundamental certainty remains unshaken despite quarterly guidance that slightly missed expectations.

Golden Opportunity or Waterfall Decline?

Citi believes Broadcom will outperform the market in the second half of the year, with demand visibility extending to 2027, and maintains its "Buy" rating. HSBC raised its FY2026 ASIC revenue estimate to $46 billion and its FY2027 estimate to $100.2 billion, citing the core logic that ASIC revenue momentum will significantly strengthen in the second half of FY2026.

44 out of 45 institutions still maintain "Buy" or "Overweight" ratings, and Wall Street's medium-to-long-term pricing has not seen a major correction despite the marginal softening of single-quarter guidance.

It should be noted that AI guidance is the core factor weighing on the stock price; despite overall results exceeding expectations, investors harbor doubts about the AI revenue growth trajectory. Susquehanna had already lowered its FY2026 AI revenue forecast from $62.5 billion to approximately $55 billion before the earnings report, preemptively anticipating the direction of this weaker-than-expected guidance.

In the long run, Broadcom's sharp decline is not due to deteriorating fundamentals but is a violent correction in the market's pricing of long-term certainty. The massive gains over the past few months pushed market expectations for AI growth to unsustainable levels, where any marginal guidance weakness triggers profit-taking. However, fundamental supports—such as an order backlog extending to 2028 and the unchanged $100 billion AI revenue guidance for 2027—remain intact.

After-hours closing price: $413.21

Support level: $410

For investors focused on the AI infrastructure sector, Broadcom's pullback offers a window to buy into long-term growth certainty at a more reasonable valuation; for short-term traders, the expectation-gap trade triggered by the AI guidance is not yet fully priced in, and the position rebalancing process in the days following the earnings report still warrants patient observation.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.