Morningstar Issues Warning, SpaceX Valuation Has Significant Premium, Waiting for Pullback May Be Best Choice

AI Podcast

Morningstar initiated research coverage on SpaceX, estimating its fair value at $780 billion, significantly below the company's target IPO valuation. This discrepancy arises from Morningstar's cautious valuation of SpaceX's AI business, despite acknowledging its leadership in launch and satellite internet. The report highlights the uncertainty surrounding the AI segment's future feasibility and economic viability as the primary driver of the valuation gap. Additionally, governance concerns, particularly Elon Musk's control and the xAI acquisition terms, are noted as significant risks. While short-term speculative enthusiasm might support the IPO price, sustained valuation will depend on fundamental performance, suggesting potential future buying opportunities.

TradingKey - As the countdown to SpaceX's IPO officially begins, the first Wall Street institution to voice clear opposition has emerged. In June 2026, Morningstar, a globally authoritative rating agency, initiated research coverage on SpaceX, providing a fair value estimate of $780 billion—less than half of the company's target IPO valuation of $1.75 trillion to $1.8 trillion.

Morningstar analyst Nicolas Owens stated clearly: We believe the company is significantly overvalued, and investors will have the opportunity to buy in at a more attractive price following the IPO.

Wide valuation gap

Morningstar's core judgment is based on a discounted cash flow (DCF) model: it values SpaceX's launch business and Starlink satellite business at approximately $611 billion, while applying probability weighting to different development scenarios for the AI business, totaling approximately $170 billion, resulting in a total fair value of approximately $780 billion.

Morningstar also acknowledges SpaceX's technological and market leadership in the launch and satellite internet sectors. In 2025, SpaceX accounted for nearly 90% of the payload mass to Earth orbit with 167 successful launches. The launch cost per kilogram for its Falcon 9 rocket has been driven down to under $1,500, a reduction of over 95% compared to the traditional space industry benchmark of over $10,000.

Starlink achieved $11.2 billion in revenue during the same period, representing a 50% year-over-year increase, with operating profit exceeding $4.4 billion. Morningstar assigned SpaceX a "Narrow Moat" rating, recognizing the cost advantages brought by its reusable rockets and Starlink's economies of scale.

The fundamental divergence in valuation gaps stems from the pricing of the AI business.

SpaceX's acquisition of Elon Musk's AI company, xAI, in early 2026 served as a key drag on Morningstar's rating downgrade. Morningstar conducted three scenario simulations for AI businesses such as orbital data centers: in the most optimistic scenario, AI infrastructure could create approximately $1.3 trillion in value, but the probability of occurrence is only 7%; meanwhile, the probability of a shelved scenario is as high as 43%, which would destroy over $81 billion in value.

Owens stated: "We believe xAI is most likely to establish a durable advantage in space infrastructure, but there remains high uncertainty regarding the scientific and economic feasibility of the plan."

From a broader perspective, the difficulty of supporting such high valuations is also prominent. Goldman Sachs pointed out that for SpaceX to sustain a $1.8 trillion valuation by 2030, it would need to achieve annual revenues exceeding $100 billion, with a compound annual growth rate maintained at over 40%, which is extremely difficult.

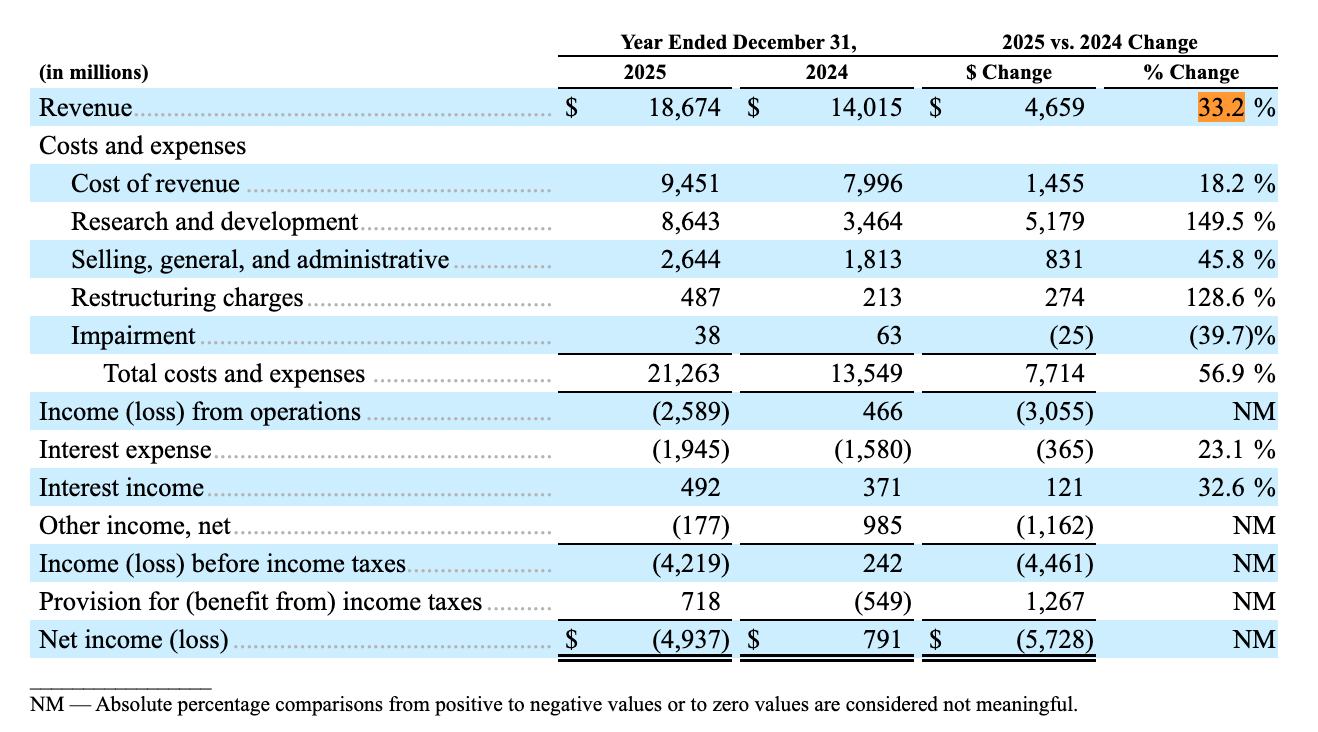

[Combined 2025 revenue for SpaceX and xAI was $18.674 billion, Source: SpaceX Prospectus ]

Previously, financial results released by SpaceX showed that 2025 combined revenue was $18.674 billion, up 33.2% year-over-year, but the net loss reached $4.937 billion, primarily dragged down by the AI business, where the AI segment recorded an operating loss of $6.355 billion.

Governance risk

Morningstar’s warnings regarding governance issues are equally impossible to ignore. Musk is expected to control approximately 80% to 85% of the voting rights through a dual-class share structure while simultaneously serving as CEO, CTO, and Chairman of the Board.

Morningstar’s report pointed out that Musk’s anticipated 85% voting control and the fact that the xAI acquisition was not an arm's-length transaction both represent significant hidden risks.

Previously, Danish pension fund AkademikerPension placed SpaceX on its investment blacklist, refusing to participate in its IPO subscription or any secondary market trading. Its Chief Investment Officer stated that SpaceX’s fair valuation should not exceed $1 trillion and described its governance structure as disastrous.

Short-term Momentum and Long-term Pressure

In the short term, speculative enthusiasm among investors may support the stock price. Morningstar noted that even if the IPO is priced significantly above fair value, SpaceX's stock price is expected to remain stable in the early stages of listing due to the minimal initial public float, robust market demand for AI infrastructure, and the fact that it can be included in the Nasdaq 100 Index just 15 trading days after the IPO.

However, as the lock-up periods for private investors expire and a large volume of shares floods the public market, subsequent selling pressure is expected to accumulate gradually. At that point, the stock price will return to a more reasonable valuation range, potentially providing investors with a larger margin of safety than the IPO.

For investors, Morningstar's core assessment explains that SpaceX's IPO premium is already at a historic high. Even though the company's launch and Starlink businesses possess clear competitive advantages, the AI assets introduced through its acquisition of xAI are still in a highly uncertain early stage. The current valuation framework assigns excessive weight to this long-term narrative.

Short-term speculation may prop up the first-day performance, but this is precisely the most typical emotional peak in a high-premium IPO. As the divergence between valuation and fundamentals is gradually absorbed by the market, an allocation window with a better margin of safety may emerge in the months following the listing. For long-term investors, there is no need to rush into chasing highs on the IPO day. Rather than taking on low premiums at peak levels, it is better to wait patiently for a natural correction after institutional holdings are released, at which point the true value anchor will gradually surface.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.