Partnering With Amazon AWS, SNOW Stock Soars 36%, 2026 Stock Price May Reach $500

AI Podcast

Snowflake's shares surged following an earnings beat and a $6 billion, five-year partnership with Amazon AWS for cloud and AI infrastructure. This deal, utilizing AWS Graviton chips, positions Snowflake as a major AWS CPU customer, aimed at scaling infrastructure for AI agents and enterprise AI applications. The collaboration enhances data governance and AI deployment for customers. Financially, Q1 product revenue grew 34% year-over-year to $1.33 billion, exceeding expectations, and full-year guidance was raised. Technical analysis suggests an inverse head and shoulders pattern, with potential upside targets of $429 and $500.

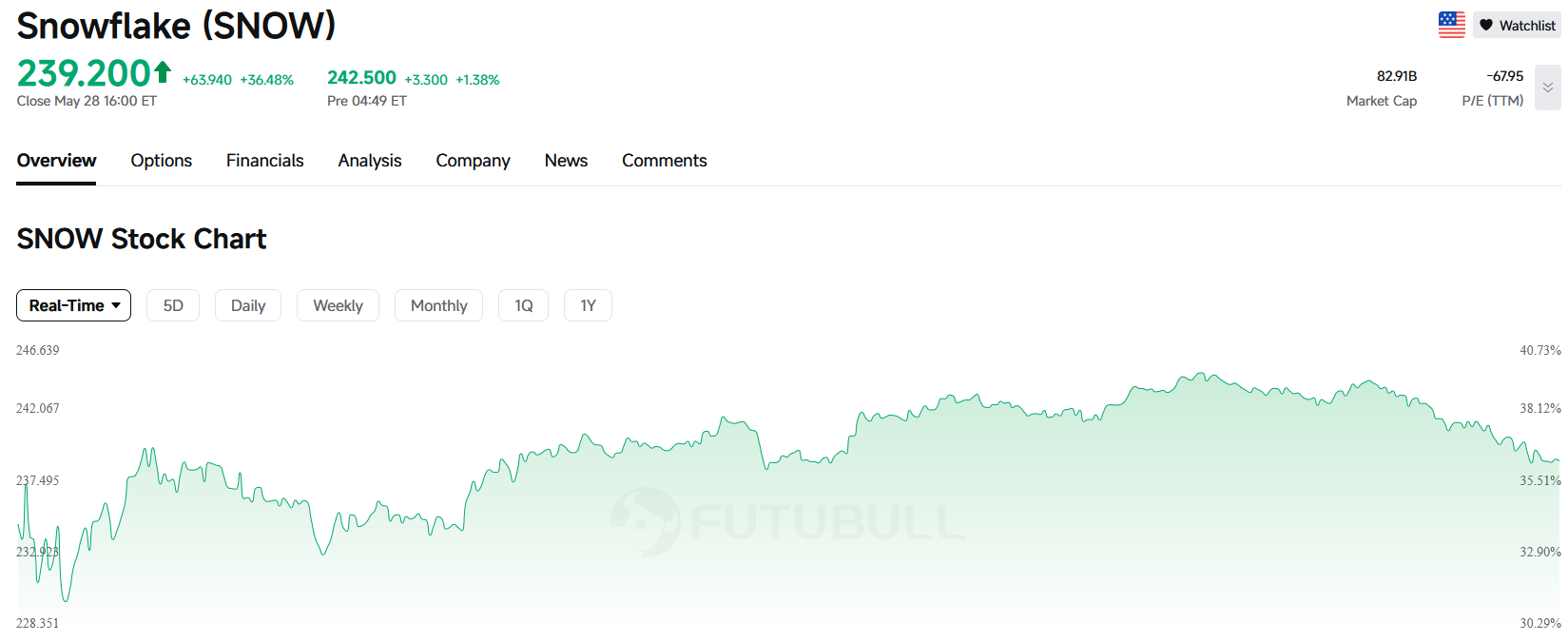

TradingKey - On May 28 ET, Snowflake ( SNOW) shares surged as much as 40% intraday and closed up 36%. The rally was driven by earnings that beat market expectations and the company's announcement of a partnership with Amazon ( AMZN )'s AWS for a five-year cloud and AI infrastructure deal totaling approximately $6 billion.

SNOW intraday price chart, Source: FUTUBULL

$6 Billion Partnership with Amazon AWS: Snowflake Bets on Infrastructure Demand for the Era of AI Agents

According to The Wall Street Journal, Snowflake will pay AWS approximately $6 billion over the next five years to utilize Amazon Graviton chips in AWS data centers, a deal that makes Snowflake one of AWS's largest CPU computing customers.

This collaboration illustrates that Snowflake is preemptively expanding its underlying computing capacity for AI agents and enterprise AI applications. While the market previously defined Snowflake as a cloud data warehouse or data platform company, the AI era demands more than just data storage; enterprises need to integrate governed corporate data into models, agents, and automated business processes. Snowflake's deepening partnership with AWS is intended to prepare infrastructure for the large-scale utilization of enterprise data by AI applications.

From a business logic perspective, the relationship between Snowflake and AWS has become even more deeply integrated. Snowflake originated within the AWS ecosystem, and many of its customers have long operated on the AWS cloud. This five-year, $6 billion partnership further solidifies the synergy between the two parties in AI data infrastructure, with AWS providing the underlying computing, chips, and cloud resources, while Snowflake offers data governance, data sharing, AI application development, and an enterprise-grade data platform. For customers, this combination reduces the complexity of AI deployment; for Snowflake, it helps drive platform consumption and customer retention.

Notably, one of the greatest challenges in implementing enterprise AI is not the models themselves, but rather data quality, permission management, security compliance, and cross-system connectivity. Large enterprises' data is typically fragmented across various clouds, business systems, and permission levels; without a robust data governance layer, it is difficult for AI applications to transition into production environments.

This is where Snowflake's core value is demonstrated. CEO Sridhar Ramaswamy stated that AI capabilities must be seamlessly connected with governed data to generate measurable business impact. A MarketWatch analysis noted that AI acceleration drove record product revenue growth for Snowflake this quarter, and the $6 billion expanded partnership with AWS is specifically designed to help enterprises deploy AI more efficiently.

Earnings beat further bolsters share price upward momentum.

According to the latest earnings report, the company's first fiscal quarter revenue was approximately $1.39 billion, up about 33% year-over-year; product revenue was approximately $1.33 billion, a 34% year-over-year increase that exceeded analyst expectations of $1.32 billion. Adjusted earnings per share were $0.39, also beating the market consensus of $0.32.

The company also raised its full-year product revenue guidance to $5.84 billion, up from the previous $5.66 billion, while its second-quarter product revenue guidance of $1.415 billion to $1.42 billion also came in above market expectations. These figures demonstrate that Snowflake's stock price is not being sustained by a single partnership agreement alone, but rather by simultaneous improvements in core business growth, customer usage, and the full-year outlook.

From an investor's perspective, the earnings beat addresses the question of whether performance is improving in the present, while the AWS partnership answers where future growth will originate. The combination of these two factors is driving a continuous rise in the stock price.

Snowflake Technical Analysis: Inverse Head and Shoulders Pattern Forms, Targeting $500 by 2026

Snowflake Monthly Stock Price Chart, Source: TradingView

Based on Snowflake's monthly stock price chart, the primary overhead resistance level is the November 2025 high of $280.67. If the price breaks through this level, it will open up upside potential toward the all-time high of $429.

The candlestick structure on Snowflake's monthly chart reveals an inverse head and shoulders pattern, signaling a bullish shift in market sentiment. With the breakout above the $237.42 neckline, bullish momentum has further intensified, and the primary upside target is to test the $429.00 resistance level. If the stock breaks decisively and consolidates above that mark, upside toward $500 will be unlocked.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.