Everyone Is Watching the Fed. Bessent's Treasury Is Gold's Real Wild Card.

AI Podcast

U.S. Treasury Secretary Scott Bessent is actively reshaping market conditions through "activist debt issuance." By prioritizing short-term Treasury bills over long-term bonds, the Treasury effectively suppresses long-term yields, acting as a substitute for traditional monetary policy. This strategy aims to manage record-high interest payments, which now exceed defense spending, while awaiting a window to "term out" debt. However, this relies on short-term rollover, creating significant refinancing risks. Investors should monitor the Treasury’s Quarterly Refunding Statement, TBAC bill-share guidance, and long-end real rates as core indicators of whether this fiscal-driven stability can be maintained or if fiscal dominance necessitates gold as systemic insurance.

Every time the Federal Reserve holds a meeting, global markets seem to hit pause — waiting for a single sentence: hike, cut, or hold.

For many years, this was how people understood macro. If you could read the Fed, you could read the dollar, read Treasuries, and read gold.

But since this Trump administration took office, something has started to feel different.

Markets still look fixated on the Fed. But the actor who has actually been moving pieces on the board — reshaping market structure, again and again — is Treasury Secretary Scott Bessent and the U.S. Department of the Treasury. The Fed is still central, of course. But if today's American financial system is a chessboard, the player making the most frequent moves is no longer only the central bank.

That's not an exaggeration. In recent years, the U.S. Treasury has sharply increased the share of short-term Treasury bills in its issuance while compressing long-term bond supply — effectively taking on a function that traditionally belonged to the Fed: influencing financial conditions, shaping the yield curve, and guiding the market's expectations about the future path of rates.

Put another way: most people are still watching the Fed's face-up cards. The Treasury has already started playing its hand face-down.

And if you follow gold, this is especially worth understanding. Gold doesn't just react to interest rates — it reacts, at a deeper level, to the entire structure of monetary credibility. What is actually changing in America today is that structure itself.

To understand this, start with one number.

The Interest Bill That Won't Stop Growing

In fiscal year 2025, U.S. federal net interest payments reached $970 billion — a record high. In fiscal year 2026, that figure is projected to exceed $1 trillion for the first time.

This sounds like a statistical milestone, but what makes it genuinely alarming isn't the size alone — it's what it signals about America's fiscal constraints.

Within the federal budget, interest payments now exceed defense spending. Based on public budget data, FY2025 interest outlays of approximately $970 billion surpassed defense spending of roughly $919 billion. The United States now spends more on servicing the cost of past borrowing than on sustaining its global military presence.

This is not a structure any major power would tolerate indefinitely.

Historian Niall Ferguson has an observation that has gained wide currency in recent years: when a great power begins directing more resources toward debt service than toward maintaining hard power, it has typically entered a phase where fiscal pressure comes to dominate both politics and strategy.

This is why understanding America today requires looking beyond inflation, employment, and the federal funds rate. The core question facing the United States is no longer simply whether to cut rates — it's something more fundamental: with debt approaching $40 trillion and interest payments breaching $1 trillion, how does the government continue borrowing at a bearable cost?

This is the defining challenge Bessent inherited when he took office.

And once the question is framed this way, the Treasury's importance becomes immediately obvious.

The Fed decides the "price of money" — the policy rate. The Treasury decides how debt is structured, who buys it, and for how long. In normal times, that was back-office work. In today's high-debt era, it has become a front-line variable that directly shapes market pricing across the entire system.

This is a shift many haven't registered: the Fed hasn't lost its importance — the Treasury has simply become equally important.

How the Treasury Can Substitute for Part of the Fed

To understand Bessent's approach, think of the U.S. Treasury as a borrower.

An ordinary borrower with steady income and manageable leverage can treat the choice between short- and long-term debt as a simple cost optimization. But a borrower already drowning in debt — where interest alone threatens to overwhelm cash flow — finds that the structure of borrowing itself becomes a matter of survival.

The United States today is much closer to the second description.

The Treasury's most important tool is not the printing press. It's the debt issuance calendar. It can issue more T-bills maturing within a year, or it can issue more 10-, 20-, 30-year bonds. On the surface, this is just a maturity choice. In substance, it decides whether to concentrate financing pressure today or defer it to the future — and whether to push market pressure onto the short end or the long end of the curve.

This brings us to the most critical part of this piece: what makes Bessent different isn't what he says — it's how he issues debt.

The First Card: More Short-Term, Less Long-Term

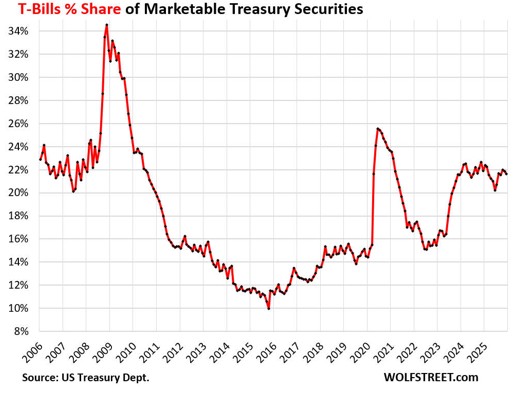

Over the past two years, the most controversial — and arguably most consequential — move by the U.S. Treasury has been a deliberate shift toward short-term Treasury bills (T-bills).

The Treasury Borrowing Advisory Committee (TBAC) — an advisory body composed of representatives from Wall Street's top banks and asset managers that provides quarterly debt management recommendations to the Treasury — is one of the most authoritative windows into Treasury issuance intent. TBAC had recommended maintaining T-bills at 15–20% of total marketable debt. During the Yellen era, the share was pushed to roughly 22%, sparking widespread debate. Treasury officials later clarified that the 15–20% target was never a hard constraint — historically the share had ranged from 10% to 36% — and TBAC subsequently revised its guidance to a "long-run average of approximately 20%." The fact that an official clarification was needed at all speaks to how sensitive the operation had become.

This approach began under Yellen. Bessent not only maintained it after taking over — he escalated it. A bond buyback program launched in May 2024 under Yellen was subsequently doubled in frequency and expanded in quarterly scale under Bessent.

Why? Because T-bills and long bonds, though both labeled "Treasuries," draw from entirely different pools of capital.

T-bills maturing within a year are naturally absorbed by money market funds, corporate cash pools, and bank liquidity accounts — investors who already seek safety, liquidity, and short duration, and who are relatively insensitive to yield fluctuations. As of mid-2026, total U.S. money market fund assets have approached $8 trillion, and fund managers have consistently signaled appetite for new T-bill supply. Short-dated issuance finds buyers quickly.

Long bonds — 10-, 20-, 30-year Treasuries — are another matter. Buyers of long bonds must absorb much longer uncertainty: Will inflation run hotter? Will the deficit spiral further out of control? Will dollar credibility erode? Will term premiums continue rising? In compensation, the market demands higher yields.

This creates a very practical tradeoff.

If the Treasury floods the market with long bonds, long-end supply surges, and buyers will demand higher yields to absorb it. Once 10- and 30-year yields rise, it isn't just government borrowing that gets more expensive — mortgages, corporate credit, equity valuations, and the entire asset pricing architecture come under pressure simultaneously.

If instead the Treasury channels more of its financing into T-bills, long-bond supply pressure stays contained, and long-end yields are not as easily pushed higher.

This is the core of what's become known as "Activist Treasury Issuance." By raising the share of short-dated debt, the Treasury has directly influenced long-term financing costs — without a single Fed meeting. It has, in effect, used its issuance structure to substitute for part of traditional monetary policy.

Source: Wolf Street

More importantly, this isn't theoretical. Economist Stephen Miran — formerly of hedge fund Hudson Bay Capital and subsequently Chair of the White House Council of Economic Advisers under the Trump administration — estimated in a 2024 research paper that this short-dated issuance bias had suppressed 10-year Treasury yields by approximately 25 basis points. Those 25 basis points are equivalent to roughly one full percentage point of Fed rate cuts. Conversely, unwinding the strategy by rolling roughly $1 trillion of short-term debt into long-term issuance would initially push long-end yields up by around 50 basis points — with roughly 30 basis points of permanent upward shift remaining after markets adjust — an economic shock equivalent to two Fed rate hikes.

Twenty-five basis points isn't an astronomical number. But anyone familiar with markets knows that size is sufficient to move mortgage rates, corporate credit spreads, and growth equity valuations. The Treasury simply shifted its issuance mix — and financial conditions across the entire market loosened slightly as a result.

This is why it's fair to say the Treasury has stolen the Fed's spotlight.

In a high-debt era, whoever can influence long-term interest rates is not just a back-office accountant. They are, in effect, a macro player.

Why This Card Works — and Why It's Dangerous

At this point, many readers will think: so what's wrong with this? If issuing more short-term debt can keep long yields contained, why not just keep doing it?

The problem is that what feels comfortable today builds fragility for tomorrow.

T-bills mature quickly — in months, or within a year. The government doesn't actually repay them with cash. It rolls them over: issuing new short-term debt to retire the old. This is standard practice in debt management. The question isn't whether the rollover happens — it's at what price.

If rates fall, the government refinances cheaply, and everything looks fine. But if rates remain elevated, or if market risk appetite contracts, then every maturity means locking in high rates again. As the large volume of T-bills issued in recent years comes due in succession, refinancing risk will accumulate significantly — and the Treasury must keep rolling short-dated debt in an environment of elevated rates.

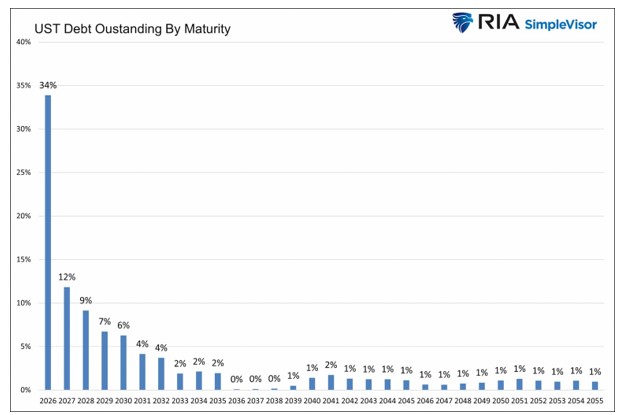

Markets have even coined a term for this: the "refinancing wall." Various estimates put the volume of Treasuries maturing and requiring rollover in 2026 at between $8 and $10 trillion. Adding roughly $2 trillion in new fiscal deficit financing, total annual financing pressure may exceed $10 trillion. The Treasury's own narrower figures show FY2026 Q1 net privately-held marketable borrowing came in at $577 billion (actual); Q2 is projected at $189 billion; and Q3 is projected at $671 billion. Sustaining large-scale debt rollover in a high-rate environment is an inescapable pressure.

Source: RIAAdvisors.com

Think of it this way: a household, wishing to avoid taking out a high-rate 30-year mortgage today, opts instead to finance with short-term credit cards and installment plans. As long as each round renews, monthly payments stay manageable. But the day a bank tightens credit limits, or short-term rates also rise, the household discovers it has never technically defaulted — yet its monthly cash flow has become dangerously fragile, because nearly all its debt reprices in the near term.

The U.S. Treasury is essentially in that position today.

So issuing more short-term debt is not a long-term answer. It's a bridge strategy: hold down the most dangerous long-end rates today, buy time, and wait for conditions to improve.

Which brings us to Bessent's second card.

The Second Card: Waiting for a Window to "Term Out" the Debt

"Terming out the debt" means gradually lengthening the maturity profile — locking in more financing at 10-, 20-, and 30-year rates rather than rolling short-term paper indefinitely.

The logic isn't hard to grasp. If most of what you owe comes due within a year, you return to market to renegotiate your price every year. The market's willingness today doesn't guarantee the same terms next year. Your fate is largely in others' hands.

But if you can lock in decades of financing, your vulnerability drops. Even if markets turn hostile next year, the long-term debt you've already placed has a fixed cost.

Bessent clearly understands this. He has also publicly acknowledged that the U.S. is far from completing this transition.

Why so far? Because now is not the right moment.

If the Treasury were to suddenly ramp up 20- and 30-year bond issuance, markets would ask: Is the U.S. desperate to lock in long-term funding? Is it worried it won't be able to borrow later? Has the fiscal situation gotten worse? When those doubts surface, buyers demand higher term premiums. The Treasury's attempt to stabilize its debt structure would instead push long-end yields higher.

And once 10- and 30-year yields rise, the damage doesn't stay in government borrowing costs. Mortgage rates climb, equity valuations compress, corporate issuance tightens — and the feedback loop ultimately weighs on growth and tax revenues.

So Bessent must wait.

What is he waiting for? At minimum, three things.

First, inflation has to come down. Until it does, markets won't believe long-term rates can hold steady.

Second, the Fed's rate path must clarify. After the Fed stopped cutting rates in late 2025, it has held rates unchanged for four consecutive meetings. The June 2026 dot plot shows nearly half of officials projecting a possible rate hike within the year — meaning the long-term rate path has not clarified, but has instead become more uncertain. Investors find it very difficult to absorb decades of duration in this environment at acceptable yields.

Third, market sentiment must stabilize. Without major crises or sudden credit shocks, investors won't commit real capital to decades of long-dated bonds.

None of these three conditions is currently met. May CPI came in at 4.2% year-over-year, up from 3.8% in April; core PCE held at 3.3% in April, signaling renewed inflationary pressure. The Fed is on hold and may lean toward hiking. Markets remain unsettled. Bessent's wait is far from over.

Bessent's situation resembles a highly indebted borrower who knows the healthiest move is to swap short-term obligations for long-term ones — but also knows that rushing to make that swap now would mean accepting long-term rates the market would price punishingly high. So he keeps rolling short-term debt, waiting for a window.

The question is: in this waiting period, why would markets keep giving him time?

Part of the answer lies in gold.

Why Gold and Treasury Issuance Are Not Two Parallel Lines

Many discussions of gold jump straight to conclusions: rate cuts are bullish for gold, inflation is bullish for gold, geopolitical shocks are bullish for gold.

None of these are wrong. But they're all at the surface level.

What gold is truly sensitive to is a deeper layer: where are the limits of monetary credibility, and will governments under debt pressure change the rules of the game?

What Bessent is doing today with debt management is pressing right against that limit.

Once the Treasury begins using maturity structure to influence long-term interest rates, fiscal power has begun penetrating territory that traditionally belonged to monetary policy. This is why "fiscal dominance" has appeared with increasing frequency in institutional research through 2025–2026.

Fiscal dominance, plainly stated, means: government debt has become so large that the central bank can no longer act solely in pursuit of its inflation mandate — it must simultaneously protect the fiscal system's ability to bear higher rates.

When that happens, monetary policy's degrees of freedom begin to shrink.

This is not without historical precedent. After World War II, America emerged with a heavy debt burden and the Fed cooperated with the Treasury to hold rates at suppressed levels — helping the government manage post-war obligations more smoothly. No press conference announced "we are sacrificing monetary independence." But the outcome was similar to what economists call "financial repression": real rates stayed chronically low, debt was slowly eroded by time and inflation, and savers bore the cost without fully realizing it.

For gold, this environment carries a specific implication: holding paper claims becomes less attractive; holding an asset that depends on no one's promise of performance becomes more attractive.

Gold generates no cash flow and pays no interest — normally its greatest weakness. But once markets begin questioning whether interest itself still represents genuine real return, that weakness becomes a strength. You hold bonds, and nominally you receive a coupon. But if that coupon is consumed by higher inflation, larger fiscal expansion, and eroding real purchasing power, what you have is a nominal return. Gold has no coupon — but it makes no fiscal promises, and depends on no central bank to keep its word.

Bessent's issuance strategy, then, is not relevant to gold through tomorrow's price. It's relevant because it is prompting more investors to revisit a fundamental question: when government debt grows large enough that managing market rates becomes an explicit objective, what is the true risk-free asset?

Why This Matters Especially for Investors

Many investors who engage with macro get stuck at the same point: they understand the concepts, but can't connect them to their own portfolios.

Bessent's story is useful precisely because it makes that chain explicit.

Step 1: To avoid pushing long-end yields higher, the Treasury issues more short-term debt.

Step 2: Long-end yields are therefore partially suppressed; financial conditions are somewhat less tight than they would otherwise be.

Step 3: But the debt structure becomes shorter, and future refinancing pressure accumulates.

Step 4: The Treasury must now wait for inflation to fall and the Fed to resume easing — opening a window to gradually extend maturities.

Step 5: During this wait, markets increasingly recognize that America's fiscal problem is structural, not cyclical — and fiscal dominance becomes a medium-to-long-term theme.

Step 6: As investors grow concerned that monetary policy may no longer be fully independent, or that real rates may be structurally suppressed, gold's appeal as an asset beyond the credit boundary rises.

Notice the chain: this is not "gold is up because of Trump" or "an official said something nice about gold." The actual logic is: the greater the fiscal pressure, the more the government must manage rates; the more it manages rates, the weaker the purity of monetary credibility; the weaker that credibility, the stronger the case for gold allocation.

Once you internalize this chain, you won't find yourself staring at each FOMC meeting, waiting to learn whether the next move is 25 basis points up or down.

Will Bessent Succeed? Two Scenarios

No one can know in advance, but the possibilities can be structured into two scenarios.

Scenario One: He finds the window.

If inflation gradually recedes over the coming quarters, the Fed pivots toward clearer easing, and long-end term premiums compress accordingly, the Treasury would have the opportunity to gradually increase long-bond issuance — slowly terming out today's short-leaning debt structure.

In this scenario, the United States hasn't solved its problems — but it has bought itself a more orderly path to managing them. Markets would read this as declining refinancing risk and a cleaner debt management trajectory.

For gold, this isn't necessarily bad news. Window-opening moments typically coincide with real rates peaking and turning lower — and real rate declines have historically been among the most reliable positive conditions for gold.

In other words, even if Bessent succeeds, gold may not lose its support.

Scenario Two: The window never opens.

If inflation won't fall, or if markets grow increasingly uneasy about America's fiscal trajectory — and long-end yields remain persistently elevated — the Treasury would have no choice but to keep relying on short-term rollover financing.

The problem then isn't imminent default. It's that markets would increasingly question whether the U.S. can only sustain its debt by chronically suppressing real rates, tolerating higher inflation, and expanding fiscal policy indefinitely.

Once that doubt deepens, gold's case becomes stronger — because gold is precisely designed for that environment: the nominal system continues to function, but the anchor of real value begins to drift.

Based on where macro stands today — with inflation re-accelerating, the Fed pausing, and the terming-out window nowhere in sight — the United States looks closer to Scenario Two. But Scenario One hasn't permanently closed; the timeline has simply become far more uncertain.

This is what makes Bessent's position unusual from an allocation perspective: success may not be bearish for gold; failure is likely bullish for gold.

This is not to say gold only goes up. It's to say that, within the current macro structure, gold occupies a rare position where there are arguments on both sides for holding it.

Three Things to Watch — Not a Conclusion to Remember

If this article ends simply with "therefore, be bullish on gold," it isn't very useful. What has real value is knowing what to watch.

The first indicator: the Treasury's Quarterly Refunding Statement.

Almost no one reads this document. But it tells markets exactly how the Treasury plans to issue debt going forward — whether long-bond auction sizes are changing, whether T-bills are still serving as the buffer. If you ever see the Treasury explicitly increasing long-bond supply, that typically signals it believes the window is opening.

The second indicator: TBAC's stance on the T-bill share.

TBAC's guidance is that T-bills should remain between 15% and 20% of total debt — enough to provide short-end liquidity without making the debt structure excessively fragile. If that share continues to hover at the high end or drift higher, it means the Treasury is still relying on the logic of buying time with short-dated paper.

The third indicator: long-end yields and real rates.

If you observe 10-year yields beginning a meaningful decline, real rates moving lower in parallel, and the Treasury simultaneously increasing long-bond issuance — that is a signal that the window Bessent has been waiting for may genuinely be opening. When that happens, it won't just be the bond market that shifts. Gold will typically be entering a new phase as well.

These three indicators are far more useful than monitoring financial headlines daily — because they help you see structure, not noise.

Most people assume gold primarily reacts to the Federal Reserve.

But if you follow Bessent's thread to its end, you find that what truly determines gold's long-term position is not whether a particular meeting moves rates 25 basis points in either direction — it's how far the United States, in order to keep its debt sustainable, is willing to push the boundary between fiscal and monetary authority.

When the Treasury begins using issuance structure to influence long-term rates; when interest payments begin consuming budgetary space; when "fiscal dominance" appears with growing frequency in institutional research — these changes, taken together, are telling you the same thing: today's gold has long since ceased to be merely a trade that catches a bid when risk sentiment turns.

It has reverted to something more foundational: insurance on the edges of the credit system.

Bessent is worth writing about not because he is mysterious or because he has some secret plan. It is because the Treasury he runs is making this dynamic progressively more visible.

Most people are still watching the Fed, because that's where the stage lights are focused.

But in this chapter of American financial history, the real scene-stealer is the Treasury.

If you've understood that shift, your framework for gold will have moved one step forward.

Disclaimer: This article is for investor education purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.