Lam Research Corp Stock Opened Up by 3.27% on Mar 4: A Full Analysis

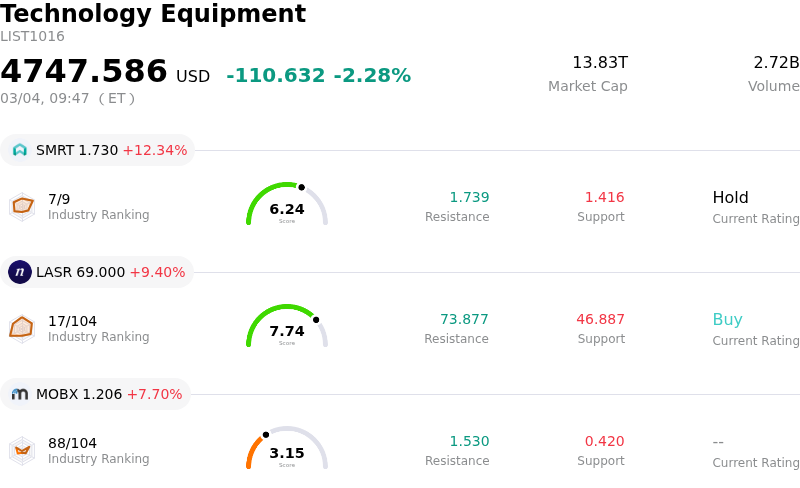

Lam Research Corp (LRCX) opened up by 3.27%. The Technology Equipment industry is down by 2.28%. The company outperformed the industry. Top 3 gainers of the industry: SmartRent Inc (SMRT) up 12.34%; nLIGHT Inc (LASR) up 9.40%; MOBIX LABS, INC. (MOBX) up 7.70%.

Lam Research Corporation's stock experienced an upward movement on March 4, 2026, driven by a confluence of positive analyst sentiment, robust industry forecasts, and strategic company-specific developments.

A significant catalyst for the positive performance was the strong endorsement from investment analysts. Zacks added Lam Research to its highly regarded Rank #1 (Strong Buy) list on this date, indicating strong potential for positive momentum. This was further amplified by multiple research firms, including TD Cowen, Barclays, Mizuho, Sanford C. Bernstein, and Needham & Company LLC, which recently raised their price targets and maintained "Buy" or "Outperform" ratings for the company. The consensus analyst rating for Lam Research remains a "Moderate Buy," signaling continued confidence in its future prospects. The Zacks Consensus Estimate for the company's current year earnings has also seen an increase over the past two months.

Another contributing factor was Lam Research's dividend announcement. The company declared a quarterly dividend of $0.26 per share, with March 4, 2026, serving as both the record date and the ex-dividend date. Such a declaration often signals financial health and can enhance investor confidence by demonstrating a commitment to returning capital to shareholders.

From an industry and company-specific perspective, the outlook remains highly favorable. Lam Research presented at the Morgan Stanley Technology, Media & Telecom Conference 2026 on March 3rd, where it highlighted its strategic growth initiatives and a positive financial trajectory. The company emphasized its successful diversification into foundry and logic markets and its strong position within the evolving semiconductor architecture landscape. Management forecasts a substantial 40% growth in advanced packaging for 2026, a segment that is outperforming the broader Wafer Fab Equipment (WFE) market due to surging demand for High Bandwidth Memory (HBM) and complex packaging, largely fueled by advancements in Artificial Intelligence (AI). The overall WFE market is projected to experience significant growth in 2026, with estimates pointing to an increase of approximately 23% year-over-year to $135 billion. Lam Research is well-positioned to capitalize on this expansion through its increasing market share in key areas. The broader semiconductor industry is anticipated to reach a historic peak in annual sales in 2026, driven primarily by the AI infrastructure boom. Additionally, the company's strong Q2 FY26 financial results, which surpassed analyst estimates for both earnings per share and revenue, underscore its robust operational performance.

While some insider selling activity by company executives was noted in early March, the overwhelming positive sentiment from analyst upgrades, the dividend announcement, and optimistic industry and company forecasts appear to have outweighed these individual transactions, propelling the stock upward during today's trading. Macroeconomic factors such as CPI data and Federal Reserve policy meetings are not immediate drivers, as the next CPI release is scheduled for March 11th and the next FOMC meeting for mid-March.

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [7.33], indicating a neutral signal. The RSI at 42.53 suggests neutral condition and the Williams %R at -96.38 suggests oversold condition. Please monitor closely.

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is 18.44B, ranking 12 in the industry. The net profit is 5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 270.22, a high of 325.00, and a low of 116.32.

Company Specific Risks:

- Significant insider selling activity by a CFO and another executive on March 2nd contributed to a 5.9% stock decline, indicating potential lack of confidence from company leadership.

- Analyst valuation models suggest potential overvaluation, with GuruFocus estimating a downside of over 34% from current price levels, and a recent downgrade to 'Hold' due to a stretched P/E ratio.

- The company faces increased financial and operational risks from its significant revenue exposure to China, with export controls already causing a decline from 43% to 35% of revenue and further projected diminishment.

- Lam Research remains susceptible to the inherent cyclicality of the semiconductor capital equipment industry, with analyst concerns regarding potential deceleration in wafer fabrication equipment spending and volatility in memory pricing post-2025.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.