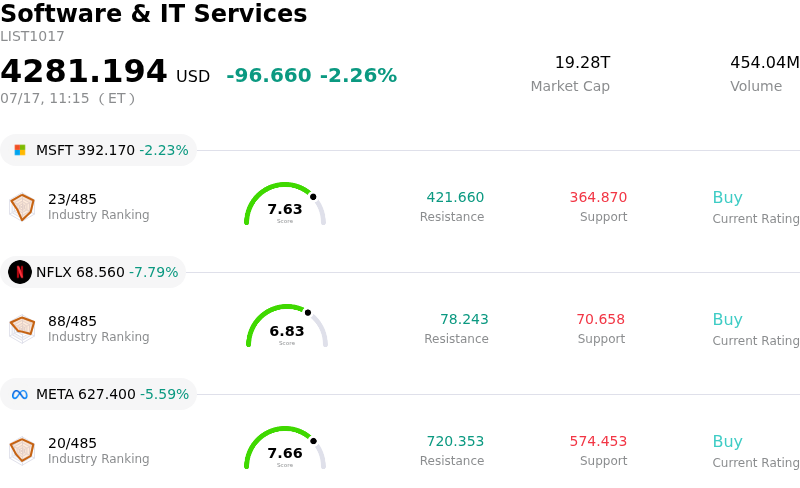

Netflix Inc Stock (NFLX) Moved Down by 8.02% on Jul 17: Key Drivers Unveiled

Netflix Inc (NFLX) moved down by 8.02%. The Software & IT Services sector is down by 2.26%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) down 2.22%; Netflix Inc (NFLX) down 8.02%; Meta Platforms Inc (META) down 5.59%.

What is driving Netflix Inc (NFLX)’s stock price down today?

Netflix shares are experiencing a sharp decline following the release of the company's latest quarterly earnings report, which appears to have disappointed investors on several key fronts. The primary catalyst for the downward movement is the company's forward-looking guidance, specifically regarding subscriber growth targets for the remainder of the year. Market participants are reacting to an outlook that suggests a cooling of the momentum previously gained from initiatives such as the password-sharing crackdown and the initial rollout of the ad-supported tier.

The stagnation in average revenue per membership is another significant concern weighing on the stock. While the ad-supported model was designed to capture a broader audience, the resulting mix shift is putting pressure on overall revenue growth in key geographic regions. Institutional analysts are reassessing their valuation models as the trade-off between volume growth and pricing power becomes less favorable. The expectation that advertising revenue would rapidly become a primary growth engine is being met with a more cautious reality, leading to a de-risking of positions across the board.

Operational costs are also under scrutiny, particularly as the company doubles down on live content and high-budget international productions. The capital requirements for securing exclusive rights to live events represent a shift in the business model that carries higher execution risks. Investors are questioning whether these investments will yield a sufficient return on invested capital in an increasingly fragmented streaming market where consumer loyalty is highly price-sensitive and churn rates remain a persistent challenge for the industry.

Macroeconomic headwinds are further amplifying the negative sentiment. Softening consumer discretionary spending data has raised fears that subscription services may be among the first areas where households look to cut costs. This macro backdrop, combined with a broader sector rotation away from high-multiple growth stocks, has triggered significant selling pressure. The lack of a strong catalyst to counter the downward guidance has left the stock vulnerable to heightened volatility as retail and institutional investors alike adjust their portfolios to reflect a more conservative growth trajectory for the streaming leader.

Technical Analysis of Netflix Inc (NFLX)

Technically, Netflix Inc (NFLX) shows a MACD (12,26,9) value of 0.845, indicating a neutral signal. The RSI at 42.012 suggests neutral condition and the Williams %R at 54.973 suggests neutral condition. Please monitor closely.

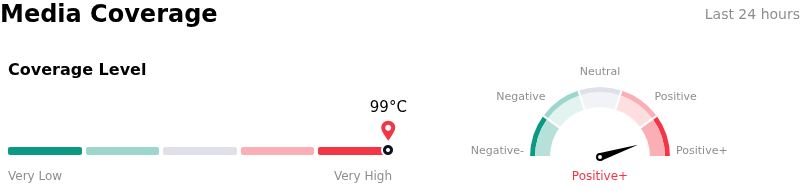

Media Coverage of Netflix Inc (NFLX)

In terms of media coverage, Netflix Inc (NFLX) shows a coverage score of 99, indicating a very high level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of Netflix Inc (NFLX)

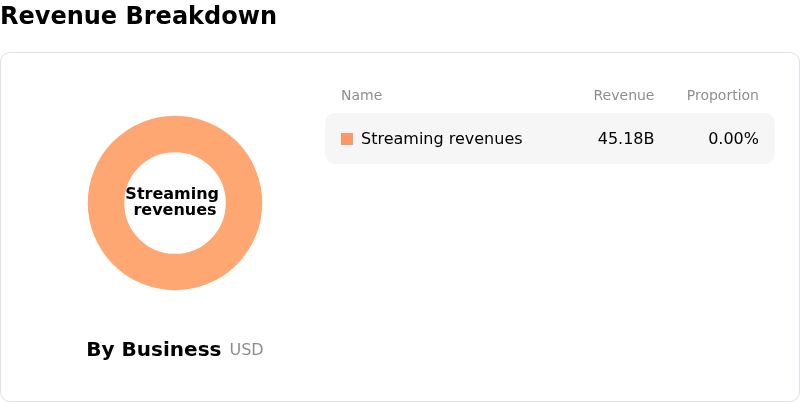

Netflix Inc (NFLX) is in the Software & IT Services industry. Its latest annual revenue is $45.18B, ranking 12 in the industry. The net profit is $10.98B, ranking 10 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $112.32, a high of $151.40, and a low of $80.02.

More details about Netflix Inc (NFLX)

Company Specific Risks:

- Transparency and Reporting Shifts: The decision to cease reporting quarterly subscriber additions and Average Revenue per Member (ARM) starting in 2025 has triggered institutional concerns regarding long-term visibility into market saturation and the sustainability of organic growth following the password-sharing crackdown.

- Ad-Tier Scaling Friction: Despite rapid subscriber intake on the ad-supported plan, analysts highlight a significant lag in monetization as the platform struggles to scale its internal ad-tech infrastructure and reach the "critical mass" required to compete for premium brand budgets against established legacy broadcasters.

- Content Expenditure Escalation: Aggressive pivots into live sports and high-cost recurring entertainment rights, such as the WWE and NFL Christmas Day deals, represent a transition toward a more capital-intensive business model that threatens to compress operating margins if advertising revenue fails to offset these fixed costs.

- Diminishing Paid Sharing Tailwinds: Current intraday volatility reflects market fears that the revenue growth attributed to the "paid sharing" initiative is nearing exhaustion in mature markets (UCAN), leaving the company without a clear immediate catalyst to sustain double-digit revenue expansion in a high-inflation environment.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.