Salesforce Inc Stock (CRM) Moved Up by 9.89% on Jun 1: Key Drivers Unveiled

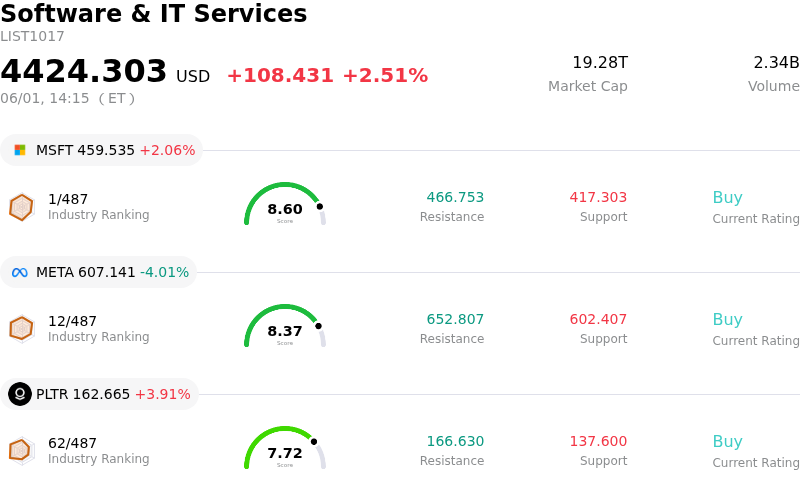

Salesforce Inc (CRM) moved up by 9.89%. The Software & IT Services sector is up by 2.51%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Microsoft Corp (MSFT) up 2.06%; Meta Platforms Inc (META) down 4.01%; Palantir Technologies Inc (PLTR) up 3.91%.

What is driving Salesforce Inc (CRM)’s stock price up today?

Salesforce's stock is experiencing significant positive momentum today, driven by a confluence of strong financial performance, strategic investments, and a favorable shift in market sentiment towards the software sector. The company recently reported robust first-quarter fiscal 2027 earnings, surpassing analyst expectations for both adjusted earnings per share and revenue. This strong financial data, coupled with a 13% year-over-year revenue growth, has provided a solid foundation for investor confidence.

Further bolstering this positive outlook, Salesforce elevated its revenue guidance for fiscal year 2027, signaling management's confidence in the increasing contribution of its artificial intelligence (AI) products to future growth. This optimistic financial guidance suggests a strong trajectory for the company.

A major catalyst for today's stock movement is Salesforce's significant $5 billion investment in Anthropic, a prominent AI chatbot company. This strategic move, announced today, positions Salesforce firmly within the rapidly expanding AI sector, enhancing its capabilities and demonstrating a forward-looking approach to technology. Anthropic's soaring valuation and impending initial public offering are expected to further solidify Salesforce's stake and boost investor sentiment.

Moreover, the company's commitment to returning capital to shareholders through a substantial $25 billion accelerated share repurchase program underscores management's belief that the stock is undervalued. This, along with a broader $27.5 billion return to shareholders, indicates a proactive financial strategy.

Market sentiment for the software industry received a boost from recent comments by Nvidia's CEO, Jensen Huang, who emphasized AI's role in enhancing productivity rather than disrupting traditional software. This perspective helped to alleviate prior investor concerns regarding the impact of AI on Salesforce's growth and contributed to a sector-wide rally in software stocks. Salesforce's own AI-first strategy, highlighted by its Agentforce platform, is also gaining traction and is seen as a key differentiator.

Adding to these positive factors, institutional investors have shown increased accumulation in Salesforce shares, and at least one analyst firm, TD Cowen, reiterated a Buy rating with a $240 price target, specifically noting the strategic advantages of Salesforce's Agentforce platform and Headless 360 architecture. Additionally, Salesforce's plan to invest $2 billion in France, including a new AI Innovation Hub, further demonstrates its commitment to global expansion and AI product adoption.

Technical Analysis of Salesforce Inc (CRM)

Technically, Salesforce Inc (CRM) shows a MACD (12,26,9) value of [-1.26], indicating a neutral signal. The RSI at 60.51 suggests neutral condition and the Williams %R at -10.21 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Salesforce Inc (CRM)

Salesforce Inc (CRM) is in the Software & IT Services industry. Its latest annual revenue is $41.52B, ranking 13 in the industry. The net profit is $7.46B, ranking 15 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $254.40, a high of $475.00, and a low of $160.00.

More details about Salesforce Inc (CRM)

Company Specific Risks:

- Salesforce issued Q2 and full-year FY27 revenue guidance slightly below Wall Street expectations, leading to investor disappointment regarding future growth prospects.

- Several analysts have downgraded Salesforce's stock or significantly reduced their price targets following the earnings report, reflecting increased caution and a less optimistic outlook on the company's near-term performance.

- The company's traditional seat-based subscription model faces potential disruption from advancements in AI, which could reduce the need for human agents or allow new AI-native competitors to offer more cost-effective solutions.

- Organic revenue growth appears muted when excluding contributions from recent acquisitions such as Informatica, raising concerns about the underlying momentum of Salesforce's core business segments.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.