Netflix Slumps Over 10% Pre-Market: Weak Q3 Guidance, Streaming Giant Faces Subscriber Growth Test

AI Podcast

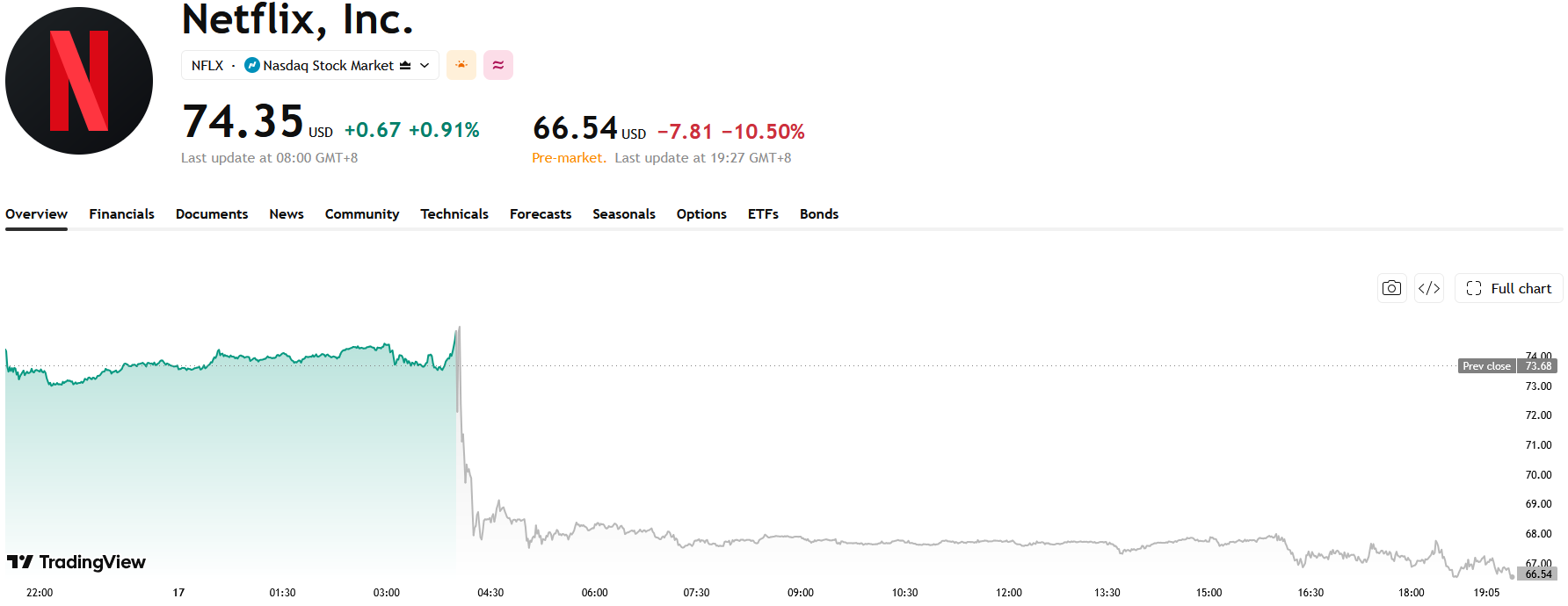

Netflix shares fell 10.5% in premarket trading after third-quarter revenue and earnings guidance missed market expectations. While Q2 revenue and net income rose 13% and 9% respectively, the projected revenue growth of 11.7% for Q3 marks its slowest pace since late 2023. Investors are concerned that high-speed expansion is ending as traditional growth drivers mature. Netflix is now prioritizing user engagement and monetization through advertising and live content to sustain long-term growth. Despite short-term sentiment pressure, the company retains industry-leading churn rates and profitability, with future valuation dependent on scaling new revenue streams and AI-driven efficiencies.

TradingKey - Netflix ( NFLX) shares tumbled as much as 10.5% in premarket trading as the company's third-quarter revenue and earnings guidance both missed market expectations, reigniting investor concerns about its growth prospects.

Source: TradingView

Third-Quarter Guidance Below Expectations, Growth Slowdown Concerns Heat Up Again

Judging from its second-quarter results, Netflix delivered a solid scorecard. The company generated revenue of $12.56 billion, up over 13% year-over-year; net income reached $3.4 billion, up approximately 9% year-over-year, with the overall performance largely in line with Wall Street expectations.

What truly disappointed the market was management's outlook for the next quarter.

Netflix expects third-quarter revenue of approximately $12.9 billion, a year-over-year increase of 11.7%, which would mark its slowest quarterly year-over-year growth rate since the end of 2023; earnings per share is projected at $0.82, which is also below consensus analyst expectations. Although the company still maintains double-digit growth, the continuous slowdown in growth has led to market concerns that its phase of high-speed expansion has come to an end.

Over the past few years, Netflix has relied on price hikes, password-sharing crackdowns, and its advertising business to drive a new wave of growth. However, as these dividends are gradually realized, investors are beginning to focus more closely on what new growth engines the company can rely on to sustain its growth in the future.

User Growth Enters Mature Phase, Netflix Accelerates Cultivation of New Growth Engines

As the global streaming market gradually matures, Netflix's business focus is also shifting, moving from pursuing subscriber growth to enhancing user engagement and monetization capabilities.

The company disclosed that cumulative viewing time on the platform exceeded 97 billion hours in the first half of this year, continuing to grow year-over-year, indicating that user stickiness remains at a high level.

Notably, since last year, Netflix has stopped disclosing quarterly net subscriber additions. Investors now need to gauge the company's operational performance through metrics such as revenue growth, advertising revenue, and user engagement, rather than solely relying on membership growth data.

To further expand its user base, Netflix has recently been re-testing free trial services in several overseas markets, hoping to attract new users who have not previously subscribed to the platform.

Management stated that the platform's overall user engagement remains healthy. For streaming platforms, the longer users watch, the lower the probability of them canceling their subscription.

According to data from market research firm Antenna, Netflix still maintains the lowest user churn rate in the industry, with a churn rate of only about 2.1% in June, continuing to hold a clear advantage in the highly competitive streaming market.

Streaming Competition Enters New Phase, Netflix Still Needs to Prove Long-Term Growth Capability

Overall, Netflix's latest earnings report did not expose any obvious fundamental issues, and its profitability, cash flow, and user engagement remain at industry-leading levels. However, the capital market's focus has already shifted from "how many new users can still be added" to "how many new sources of growth can still be created".

The advertising business, live content, AI technology, and more content formats are becoming crucial pillars for Netflix's next phase of growth. If these businesses can continue to scale up monetization, it will help alleviate the pressure stemming from the slowing growth of its traditional subscription business.

In the short term, the lower-than-expected third-quarter guidance will inevitably dampen market sentiment and has led to a noticeable pullback in the stock price. In the long run, however, whether Netflix can continuously enhance its advertising monetization capabilities, enrich its live content ecosystem, and leverage AI to further optimize content production efficiency will be crucial in determining whether its next growth cycle can be unlocked.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.