SpaceX Soared 50% After Listing, Why Did This Space ETF Holding It Fall Instead of Rise?

AI Podcast

As of June 16, Eastern Time, the Tema Space Innovators ETF (NASA) faces significant headwinds following the SpaceX IPO. While NASA previously surged on its unique status as an indirect vehicle for SpaceX equity, the IPO’s materialization has eroded its scarcity premium. Shares fell over 9% post-launch as liquidity shifted toward direct SpaceX investment and broader space-sector holdings suffered a "sell-the-news" correction. Investors now face risks regarding valuation lags, 180-day lock-up restrictions, and high concentration. With SpaceX’s imminent inclusion in the Nasdaq 100, direct stock exposure may prove more efficient than maintaining NASA’s 0.75% fee-based structure.

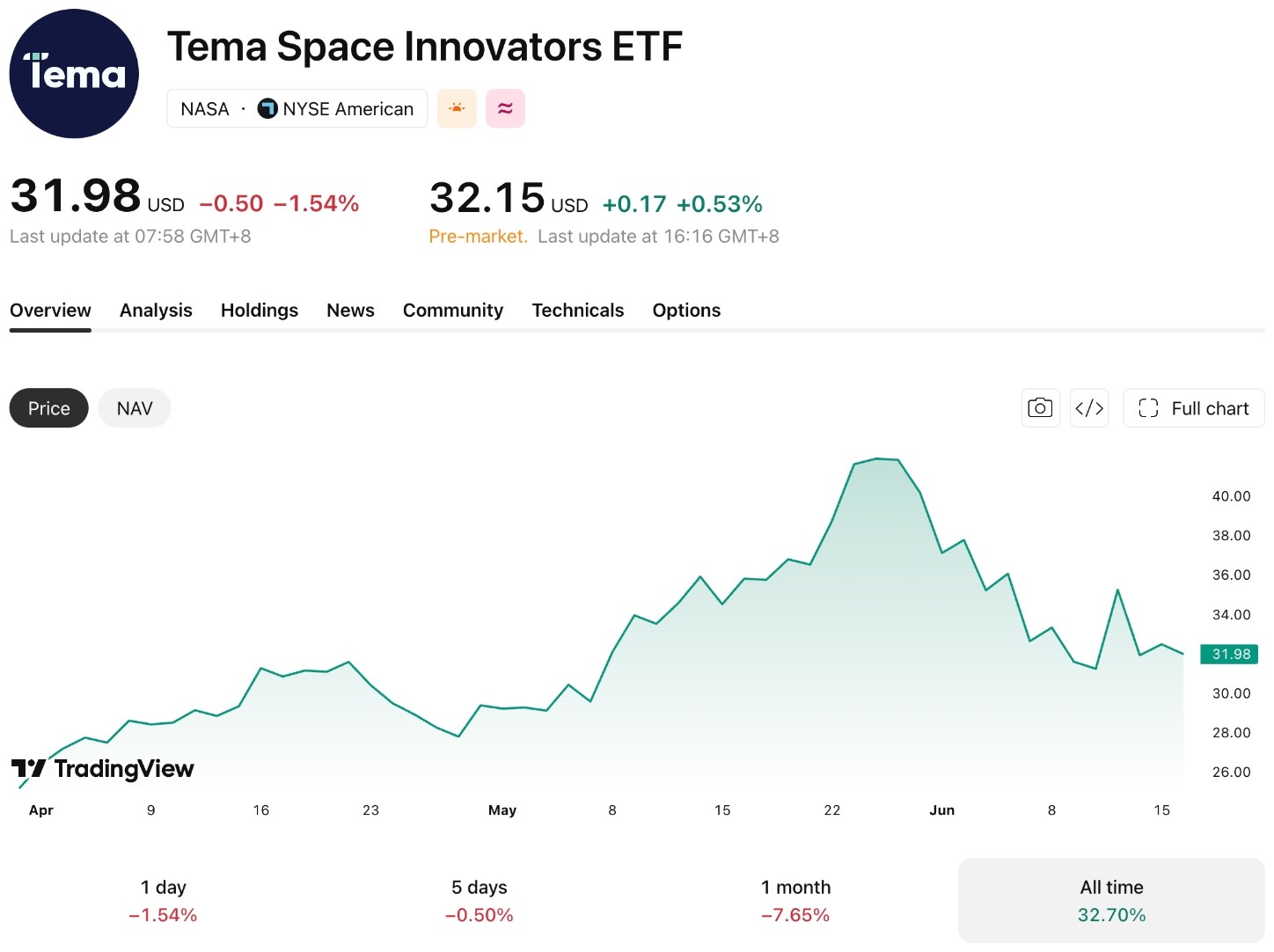

TradingKey - As of June 16, Eastern Time, the Tema Space Innovators ETF ( NASA) has delivered a cumulative return of approximately 32.7% since its listing on March 31. Leveraging its unique positioning as the 'first pure-play space-themed ETF to indirectly hold pre-IPO equity in SpaceX,' the fund attracted over $3 billion in inflows in just over two months, surpassing established peers to become the world's largest space-themed ETF.

However, as SpaceX ( SPCX) completed its IPO on June 12 and surged approximately 50% in the three trading days following its debut, NASA's scarcity premium has been rapidly eroding. Its share price has pulled back to $31.98 from an all-time high of $42.68 in late May, and fell more than 9% on the first day after the IPO, making its future direction a central focus for the market.

[Source: TradingView]

AUM and Holdings of the NASA ETF

As of mid-June, NASA 's assets under management were approximately $3.27 billion. The fund holds a total of 42 stocks, with the concentration of its top ten holdings at around 58% to 60%.

The key reason NASA has been able to attract significant capital is that it indirectly holds shares in SpaceX through a special purpose vehicle (SPV), with the structure provided by Charles Schwab's Forge. Prior to SpaceX going public, retail investors had virtually no legitimate channels to access investment opportunities in the world's most valuable private company.

Top 10 Holdings (as of June 16, according to Tema's official website) :

Rank | Company Name | Ticker | Business Profile | Weight |

1 | SpaceX | SPCX | Rocket Launch and Satellite Internet | 12.47% |

2 | EchoStar | Satellite Communication Services | 10.90% | |

3 | Rocket Lab | Small Satellite Launch Services | 9.61% | |

4 | MDA Space | Space Robotics and Ground Systems | 6.94% | |

5 | AST SpaceMobile | Space-based Mobile Communications Network | 5.37% | |

6 | Intuitive Machines | Lunar Exploration and Logistics Services | 4.53% | |

7 | York Space Systems | Satellite Manufacturing | 4.15% | |

8 | Firefly Aerospace | Rocket and Spacecraft Manufacturing | 4.11% | |

9 | 5N Plus | VNP | Semiconductors and Specialty Materials | 4.10% |

10 | ViaSat | Satellite Broadband Communications | 3.94% |

In terms of sector distribution, industrial companies dominate, followed by technology and communication services companies, with the overall portfolio focusing on core segments of commercial aerospace such as launch, satellite operations, and ground equipment.

Why is NASA struggling to keep pace after SpaceX's IPO?

SpaceX listed on the Nasdaq on June 12 at an offering price of $135 per share, raising $75 billion and setting a record for the largest IPO in global capital market history. Post-listing, the stock price continued to climb, closing at $201.8 on June 16, representing a cumulative gain of approximately 49.5% from its IPO price, with its market capitalization reaching around $2.64 trillion.

However, NASA did not rise in tandem, instead falling over 9% on the IPO's first day. Many retail investors might be confused: since NASA holds SpaceX, why did SpaceX surge while NASA did not?

This is because retail investors had previously flocked to NASA; unable to increase positions in the unlisted SpaceX, new capital was forced to buy other stocks (such as Rocket Lab), diluting SpaceX's weighting. Once SpaceX officially listed, it aggressively drained liquidity from across the market, causing other space stocks—which make up nearly 88% of the ETF—to suffer a 'sell-the-news' sell-off and plunge collectively, severely dragging down the overall net asset value (NAV). Furthermore, restricted by a 180-day lock-up period, the fund could not sell SpaceX at its highs to cash out, leaving its NAV still constrained by the overall sluggish performance of the sector.

What risks should be monitored in the market going forward?

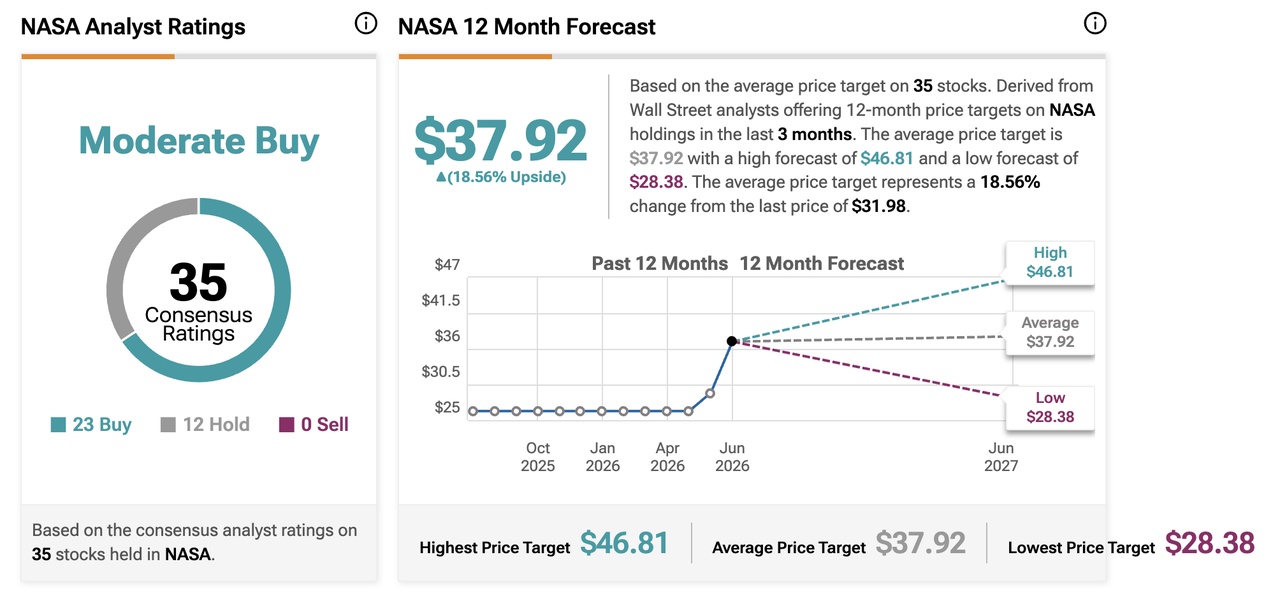

[Source: TipRanks]

According to data from TipRanks, the overall analyst consensus for the constituent stocks held by NASA is a "Moderate Buy," with an average 12-month target price of approximately $37.92, representing a potential upside of about 18.56% from recent prices. However, investors need to be aware of the following risks:

Valuation Lag Risk. The SpaceX shares held by NASA through SPVs are not marked to market daily, but are updated during fund transactions or periodic valuations. Although SpaceX's stock price has risen about 50% since its listing, this portion of the holdings has not yet been revalued. The fund's net asset value (NAV) cannot fully reflect changes in SpaceX's market value before the revaluation, making it difficult for investors to accurately assess the fund's true value.

Lock-up Period Restrictions. Following the IPO, SPVs are subject to lock-up periods, meaning private holdings are not expected to be convertible into publicly traded shares for at least six months. During this period, even if SpaceX's stock price fluctuates significantly, the fund cannot flexibly adjust this portion of its holdings.

Concentration Risk. The top ten holdings account for approximately 60% of the fund's assets, meaning the performance of a few companies has a significant impact on the overall net asset value. The U.S. Securities and Exchange Commission (SEC) classifies NASA as a "non-diversified fund," reflecting its high concentration of holdings.

Fee Levels. NASA's annual management fee rate is 0.75%, which is higher than that of similar defense-themed ETFs (such as Invesco PPA's 0.58%).

Capital Diversion Pressure. According to market expectations, the Nasdaq 100 Index will include SpaceX as a constituent stock 15 trading days after its listing. At that time, passive funds tracking the index will directly allocate to SPCX, which could potentially divert inflows away from NASA.

SpaceX's IPO expectations have been realized: Is NASA still worth investing in?

The sharp rally of NASA over the past two months since its listing was essentially the market pricing in expectations of SpaceX's listing in advance. With the IPO now materialized, the fund's scarcity value as "the only channel to indirectly hold SpaceX through the public market" has ceased to exist.

For investors optimistic about the long-term development of the commercial aerospace value chain, NASA still provides an actively managed tool covering launch, satellite operations, and ground equipment segments. If the sole purpose is to gain SpaceX exposure, directly holding SPCX might be a more straightforward choice.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.