SK Hynix US Listing Timeline Surfaces, Said to Debut as Early as August

AI Podcast

SK Hynix plans a U.S. ADR listing, potentially by mid-August, following confidential SEC filing in March. Sources suggest investor feedback has been "extremely positive" due to AI demand and the company's chip market position, aiming to broaden its shareholder base. The company's stock has experienced significant volatility, influenced by profit-taking and geopolitical risk. Driven by AI memory chip demand, SK Hynix reported strong Q1 2026 earnings, with revenue up 198% and operating profit up 405%. Analysts at Nomura and J.P. Morgan find its current valuation attractive, citing low P/E ratios relative to industry benchmarks.

TradingKey - On June 10, ET, Reuters cited sources familiar with the matter as saying that SK Hynix plans to list in the U.S. as early as August this year. The U.S. Securities and Exchange Commission (SEC) may approve its American Depositary Receipt (ADR) listing application during the week of June 22. South Korea's Meritz Securities reported on the same day that if the approval process is successful, SK Hynix will officially list as early as mid-August.

SK Hynix responded in a statement that it plans to issue ADRs by 2026, but the specific scale and timing have not yet been finalized. The company had already filed for a U.S. listing confidentially in March, with sources at the time indicating that the fundraising could be as high as $14 billion.

According to media reports, recent roadshows have received "extremely positive" investor feedback, attributed to robust AI demand and the company's competitive position in the memory chip market. Some U.S. institutional investors are only permitted to invest in U.S.-listed stocks, and SK Hynix aims to broaden its shareholder base through this listing.

Sharp volatility in stock prices

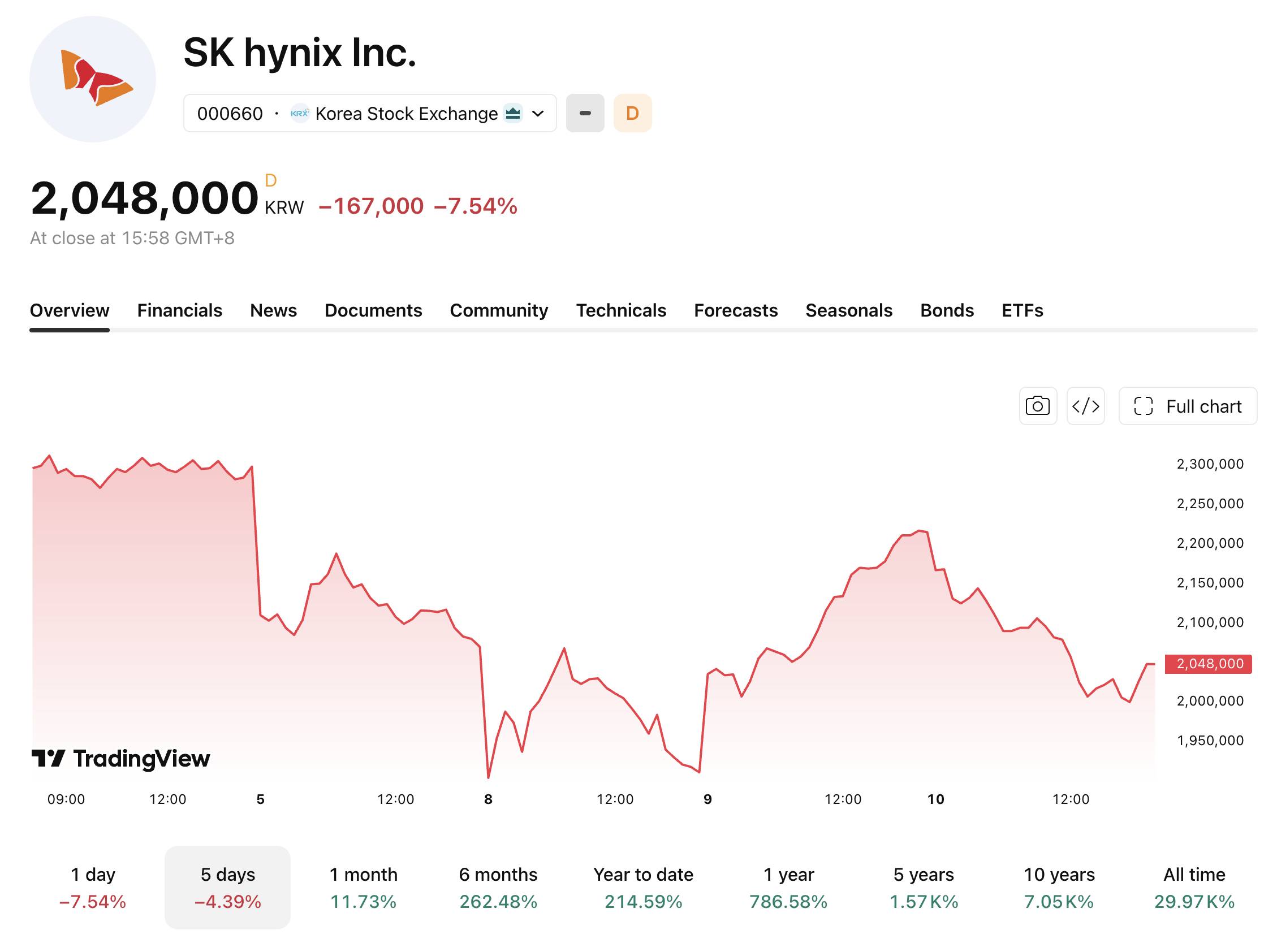

SK Hynix shares have seen intense volatility recently. On June 8, South Korea's KOSPI index closed down 8.29%, triggering a Level 1 circuit breaker and a 20-minute trading suspension, while SK Hynix fell 7.68%. The next day, chip stocks staged a powerful rebound, with SK Hynix surging nearly 16% and the KOSPI closing 8.18% higher. Today, SK Hynix closed at 2.048 million won, down 7.54%. The sharp price swings reflect growing market divergence regarding the AI storage sector and intense capital positioning.

This rollercoaster performance was primarily driven by two factors: profit-taking following excessive gains in AI chip stocks, and heightened risk aversion fueled by the military conflict between the U.S. and Iran. The magnification effect of leveraged ETFs further exacerbated the volatility.

[Source: TradingView]

Earnings and valuation support

Over the past year, SK Hynix's stock price has surged by more than 780%, with the core driver being the robust demand for advanced memory chips from AI data centers.

In the first quarter of fiscal 2026, the company reported revenue of approximately 52.58 trillion won, up 198% year-on-year; operating profit reached 37.61 trillion won, up 405%; and net profit was 40.35 trillion won. The operating margin hit a record high of 72%. Since May, the company's market capitalization has surpassed $1 trillion, making it, after TSMC ( TSM) and Samsung Electronics, the third company in Asia to reach this milestone.

Regarding valuation, several institutions believe current levels remain attractive. Nomura Securities noted that SK Hynix's 12-month forward P/E ratio is approximately 6x, which severely undervalues the sustainability and stability of its earnings. J.P. Morgan, meanwhile, set SK Hynix's 2026 forward P/E at about 6.9x, representing a significant valuation discount compared to the Philadelphia Semiconductor Index's forward P/E of about 27x.

In an in-depth global semiconductor memory industry report released on June 1, Goldman Sachs pointed out that the valuation framework is undergoing a historic shift, with the industry benchmark officially moving from price-to-book (P/B) to price-to-earnings (P/E). It raised its target price for SK Hynix to the 3.3 million to 3.5 million won range, implying an upside of approximately 53% from the price on that day.

The report argues that even if memory prices were to fall by 30% annually over the next two years, SK Hynix would still be able to maintain an operating margin of around 40%. The consensus among multiple institutions indicates that the market is re-evaluating the structural shift in the memory industry.

As a core supplier to Nvidia ( NVDA ), SK Hynix has benefited profoundly from the surge in demand for AI computing power. Market participants expect that the upcoming U.S. listing will serve as a key window to gauge the level of global capital's recognition of its valuation.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.