Costco Q3 Revenue and EPS Both Beat Expectations, Why Can’t Strong Performance Drive Up the Stock?

AI Podcast

Costco reported fiscal Q3 2026 results with revenue and EPS exceeding expectations, and comparable store sales growth outpacing peers, driven by strong international performance and e-commerce. Despite record gasoline sales contributing to traffic, the stock declined post-earnings. This is attributed to high market expectations and valuation, with limited incremental information to justify further upside. Concerns remain regarding a slowdown in membership growth and a dip in renewal rates below 90%, impacting Costco's premium valuation supported by membership stability.

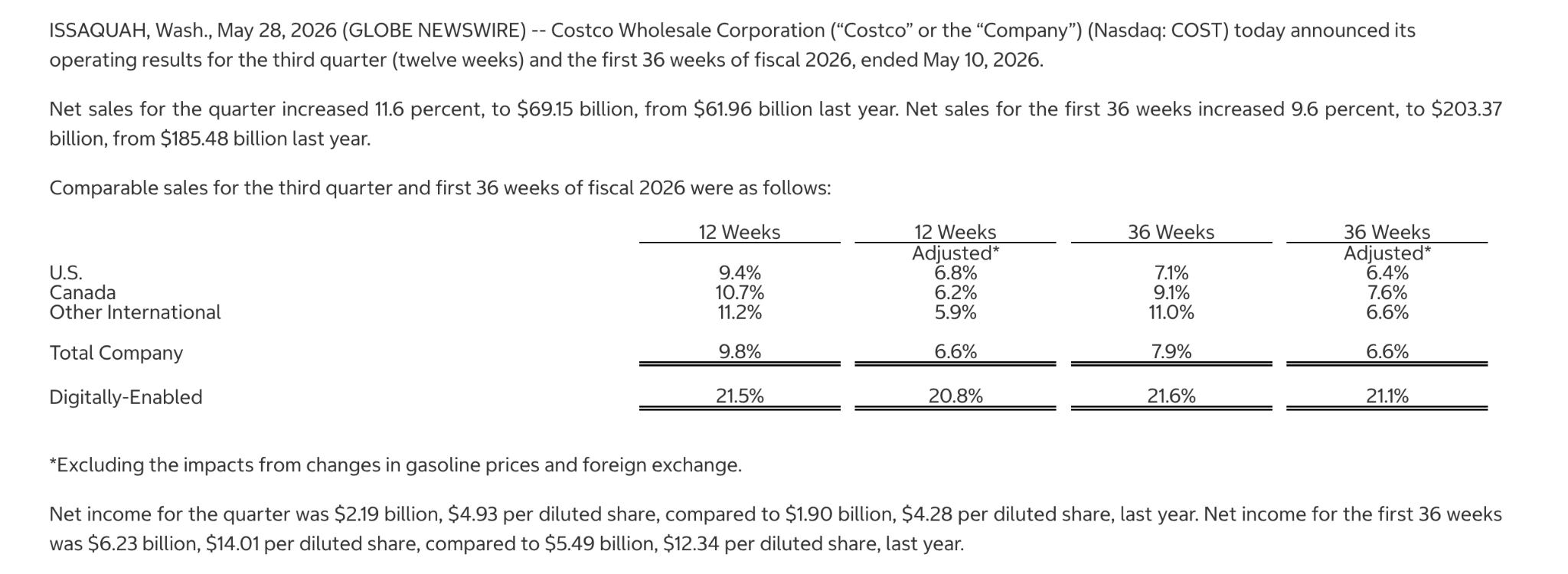

TradingKey - After the market close on May 28 ET, retail giant Costco ( COST.US) reported its fiscal 2026 third-quarter results, with both revenue and earnings per share beating market expectations. Furthermore, its key same-store sales growth and digital channel performance outpaced major retail peers.

However, this solid report failed to lift the share price. Following the earnings release, Costco's stock price swung from a 0.5% gain to a 0.5% decline in after-hours trading, indicating that the market remains cautious toward the results.

Revenue and earnings both beat expectations.

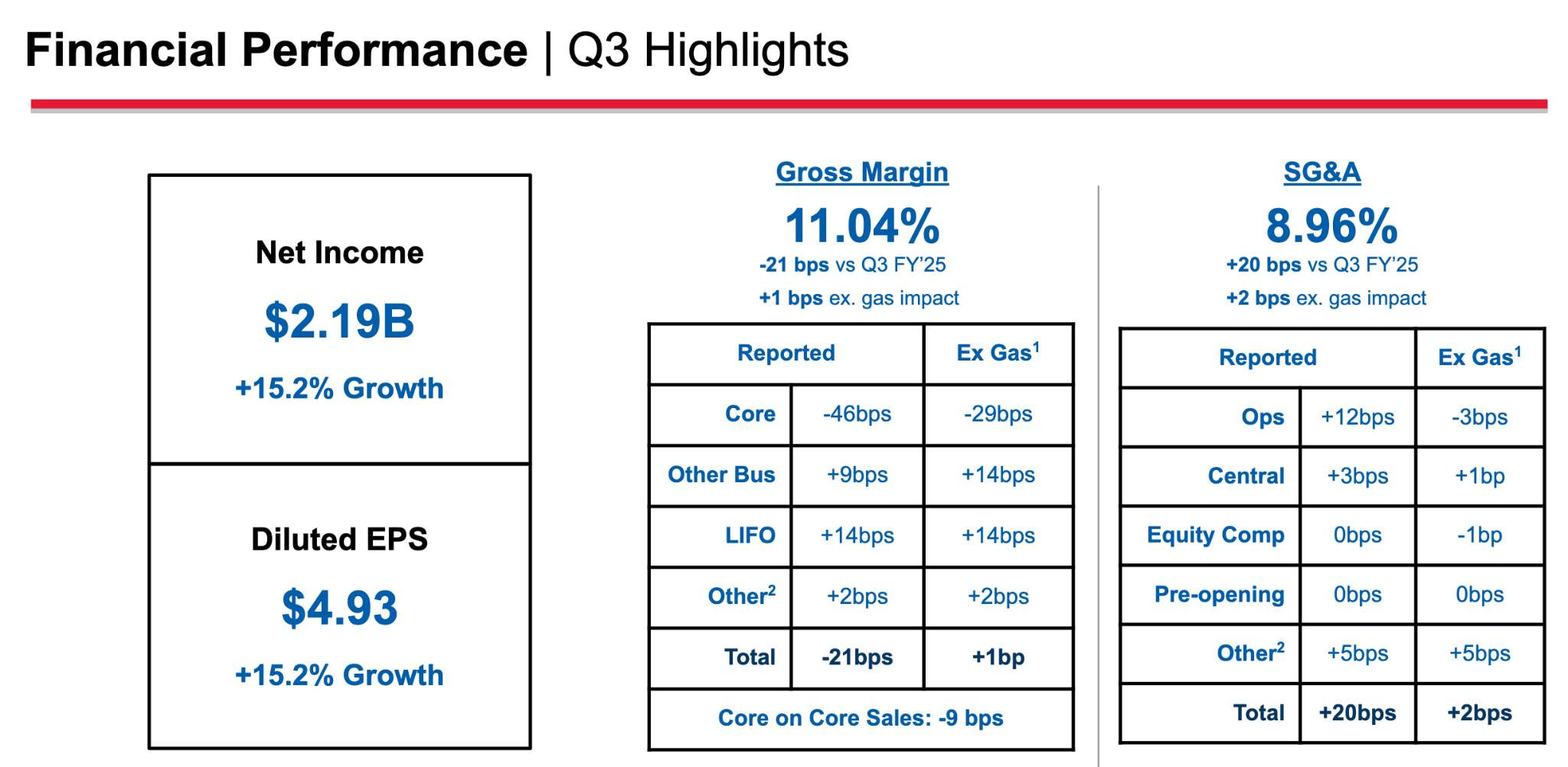

For the third fiscal quarter ended May 10, 2026, Costco reported total revenue of $69.15 billion, up 11.6% year-over-year, exceeding the analyst forecast range of $68 billion to $68.6 billion; net income rose to $2.19 billion, or $4.93 per share, from $1.9 billion, or $4.28 per share, a year earlier, which was in line with market expectations of $4.87 to $4.95 per share.

Net income for the first 36 weeks was $6.23 billion, or $14.01 per diluted share, compared with $5.49 billion, or $12.34 per diluted share, in the prior-year period. Gross margin stood at 11.04%, and free cash flow was approximately $18.946 billion.

Meanwhile, membership fees, Costco's core profit driver, saw revenue grow 10.7% to $1.37 billion during the quarter.

Same-store sales lead retail peers.

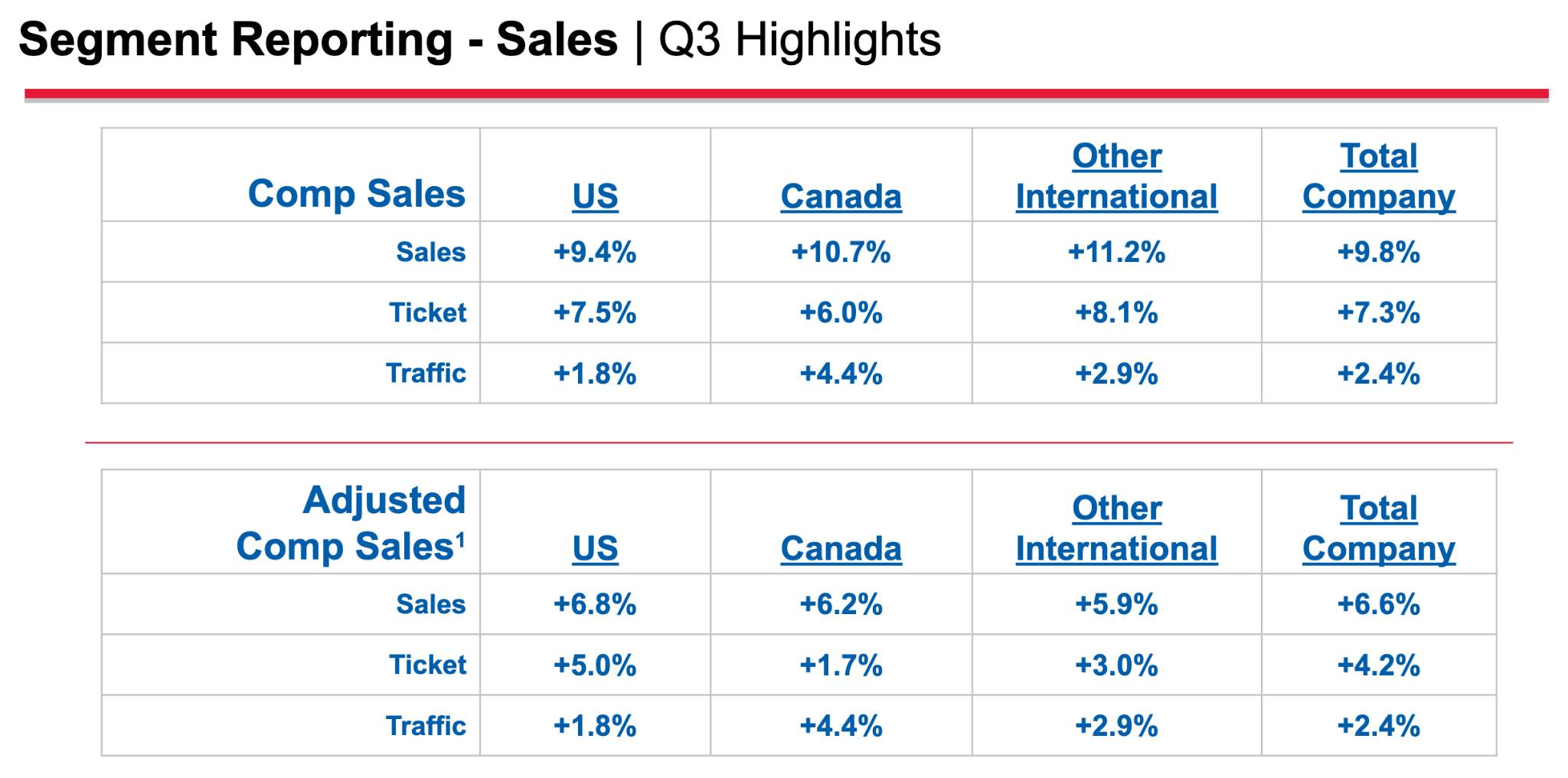

Global comparable store sales grew 9.8% this quarter, or 6.6% excluding the impact of gasoline and foreign exchange, surpassing the market consensus of approximately 6%. Specifically, the U.S. market grew 9.4%, Canada grew 10.7%, and other international markets grew 11.2%, as international operations continued to lead.

Walmart's U.S. comparable sales grew about 5% in the most recent quarter, while Target and Dollar General recorded only low-single-digit growth; Costco remains a top performer among major retailers.

Furthermore, digital channels were also a highlight of the earnings report, with e-commerce comparable sales surging 21.5%.

High oil prices are a double-edged sword for Costco.

While rising costs from high oil prices eroded some retail and transportation margins, the high-price environment underscored the unique value of a Costco membership, as record gasoline sales drove growth in foot traffic.

On May 28 ET, Costco stated that its gasoline business saw record-breaking sales volume in the fiscal third quarter ended May 10, as oil prices rose.

CEO Ron Vachris noted that the final five weeks of the quarter were the highest gasoline volume weeks in Costco's history, as consumers increased purchases in search of cheaper fuel amid rising oil prices during the conflict between the U.S. and Iran.

The savings consumers achieve at discount gas stations can even offset the cost of membership fees; moreover, customers who come for fuel often shop inside the warehouse, generating a cross-selling effect.

Stellar Performance: Why Isn’t the Stock Price Rising?

Although Costco's results slightly exceeded expectations, TradingKey believes that the high valuation driven by high market expectations has compressed its upside potential.

[Costco Historical Valuation Trend, Source: Companiesmarketcap.com]

Prior to the earnings release, Costco's forward P/E ratio was approximately 52x, compared to about 42x for Walmart during the same period. Costco's strong performance this quarter actually only slightly exceeded high expectations, as investors had already priced this robust performance into the stock price.

For mature retailers, short-term growth potential and margin expansion inherently have natural caps; furthermore, the market did not find enough incremental information in the earnings report to drive further valuation expansion.

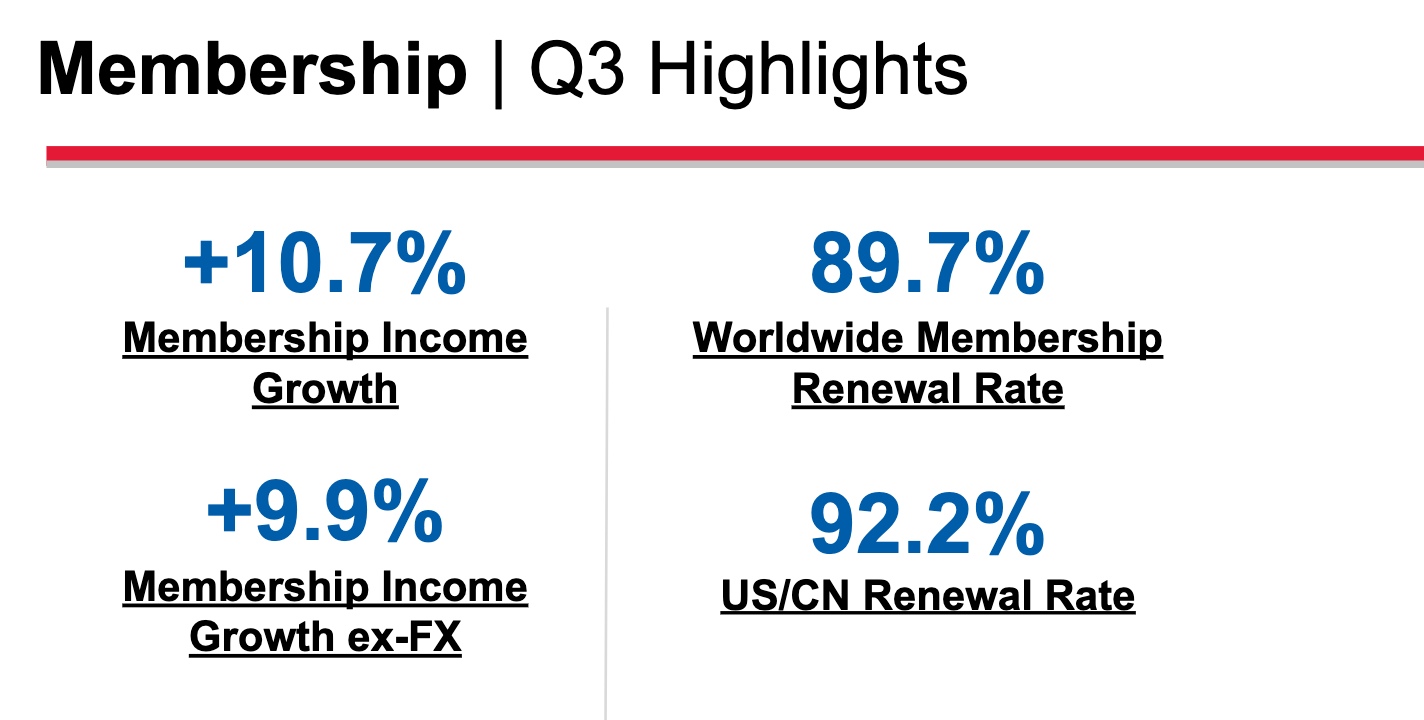

Investors should note that in the previous Q2 fiscal quarter, membership growth—the core growth driver for Costco—showed a marginal slowdown, declining significantly from the 6% to 7% growth rate seen in the same period last year.

Management partly attributed this to a high base effect from the previous year, but a deeper structural factor is that the proportion of young members joining through digital channels has surged from 5% in 2019 to nearly 50%, and these consumers tend to have lower brand loyalty and relatively higher churn rates.

The slowdown in membership growth is directly related to the core support of Costco's valuation, as its nearly 50x P/E premium is largely built on the foundation of sustained stability in membership size and renewal rates.

[Membership Growth Highlights, Source: Costco Q3 Fiscal Quarter]

Regarding renewal rates, the core U.S. and Canadian markets dipped slightly to 92.2%, while the global renewal rate fell slightly below 90%, breaking the psychological threshold of 90%.

From a growth perspective, the momentum of Costco's core "membership" segment is gradually slowing down, and this valuation premium will continue to erode from the stock price; in this context, earnings that only slightly beat expectations struggle to satisfy investors' anticipation for Costco's relatively high growth compared to its peers.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.