ServiceNow: Investors’ Panic Sell-off Might Not Be Justified

AI Podcast

ServiceNow (NOW) stock has experienced an over 86% decline due to AI disruption fears, despite consistent revenue growth above 20% and strong customer retention. The company's strategy focuses on integrating AI as an enabler rather than a replacement, evidenced by partnerships with AI firms like Anthropic. Financials show robust FY2025 revenue at $13.278 billion (20.89% YoY growth) and net income at $1.748 billion, with an improving EPS. While its P/S multiple suggests undervaluation compared to peers, potential margin compression from AI investments presents a risk.

Setting The Stage

ServiceNow (NASDAQ: NOW) stock price has lost by over 86.30% in the last year, due to investors’ panic over possible AI-related disruption. For your information, this company’s fundamentals and financial performance have remained steady, maintaining a top-line YoY growth rate above 20% amidst these market headwinds. Honestly, isn’t this interesting? I think it is because, despite these AI-boom fears, customer stickiness has remained intact, which is a testament that they are deriving value from NOW services. In fact, the company has sustainably beaten analysts’ revenue estimates in FY2025 amidst this AI-related panic sell-off, which confirms that the company is offering value, evidenced by customer stickiness.

TradingKey

I will delve into financial details later and how it is related to customer stickiness. But to mention something, the renewal rate of customers has remained at 98% expect for Q3’2025 when it went down to 97% but recovered to 98% in Q4’2025. From where I sit, the driving force behind this solid customer stickiness is that NOW is becoming a cheaper and more efficient alternative as opposed to a replacement for AI. This can be seen in the partnership between ServiceNow and Anthropic, where NOW is seeking to deploy agentic workflows across its SaaS platform to execute tasks autonomously.

Let’s now dive deeper into the details of why I think customer stickiness is a major indicator that warrants a Buy rating on NOW.

The Big Picture

Before I get to the big picture, let me introduce you to the basis of my perspective. NOW generates most of its revenues from SaaS, and this is one of the most feared areas that investors have been skeptical about due to the loss of customers who might access exact services from other AI models, such as ChatGPT. These fears are valid, but they have been disproven by the customer stickiness the company continues to show. One-way customers are seeing value, yet there are optional AI models that are looking at the ServiceNow commitment to align with the AI models across its subscriptions. For example, ServiceNow and Anthropic have partnered to help their customers with curated or enterprise-specific AI models for agentic workflows. For those who don not know, agentic workflows means that instead of having one AI model doing all tasks or a human being doing repetitive tasks, varied and specified agents can be used to perform those tasks efficiently.

Moving on to the pig picture, recall that I said that investors’ fears are valid because there are meaningful changes AI is bringing to organizations. A good example is the 10 million hours on-hold crisis Australia is currently reporting in the customer service. About 46% of Aussies cite poor customer service and are ready to switch to other competitors. NOW looks at this problem opportunistically, given that over 58% of Aussies so far have seen the benefit of using AI in various tasks, such as personal interactions and the reduction of errors.

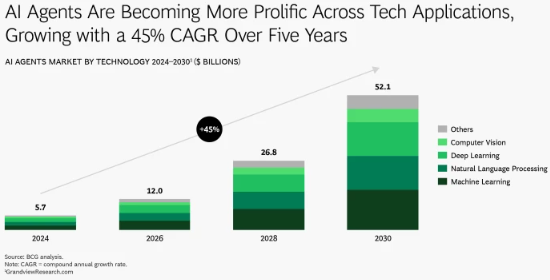

This reveals that there is a real need for agentic AI that SaaS companies can integrate with to automate tasks that do not require physical interactions. About 57% of work can currently be automated, as opposed to 43% of work that cannot be automated. As such, it becomes easier to draw from this on why AI agents are gaining traction more rapidly, especially around technology-related companies. This is why AI agents are currently estimated to grow at a CAGR of 45% towards 2030. In this year (2026), AI agents are estimated to reach a market volume of $12.0 billion, and this is expected to reach $52.1 billion by 2030.

BCG

It is coming out clearly that agentic AI is at its tipping point because in 2025, AI assistants began being embedded into most companies’ applications, and now in 2026, enterprise apps have begun integrating task-specific AI models for every application. This is exactly where I am seeing NOW to have a solid position in this AI ecosystem. NOW is incorporating AI models in its SaaS companies, such as OpenAI and Anthropic.

Financial Highlights

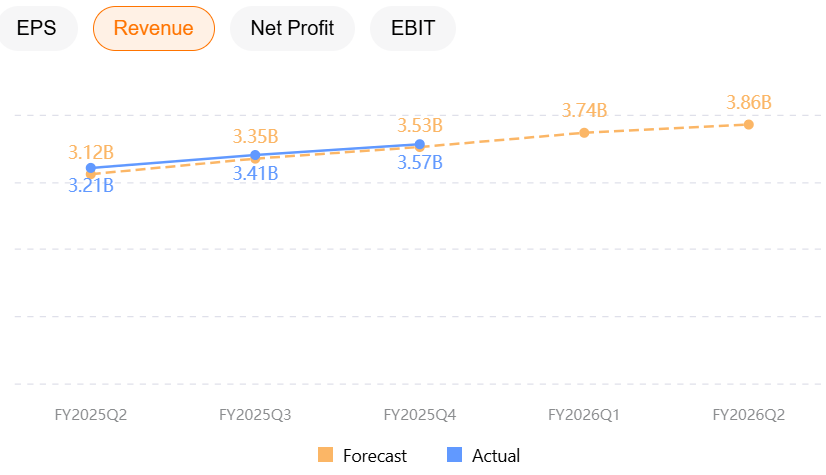

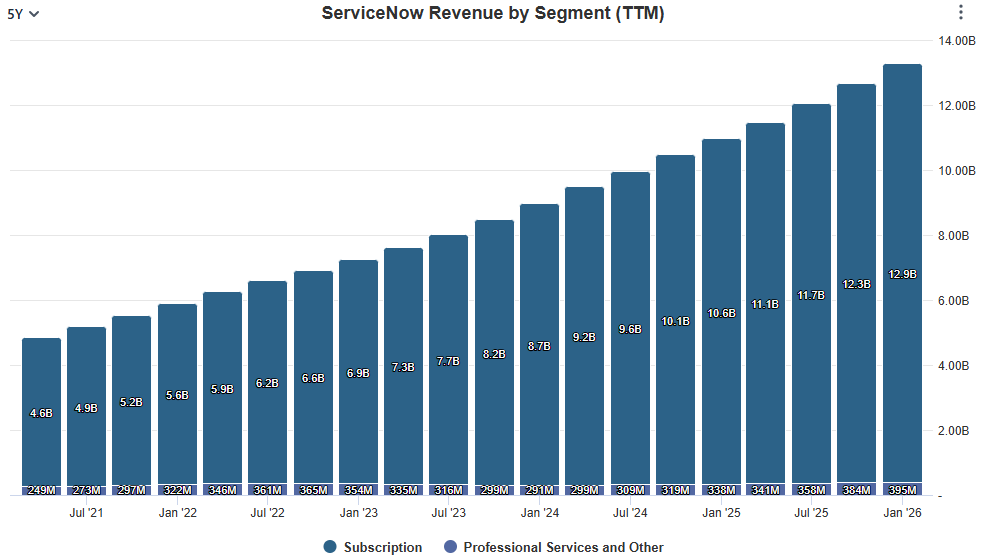

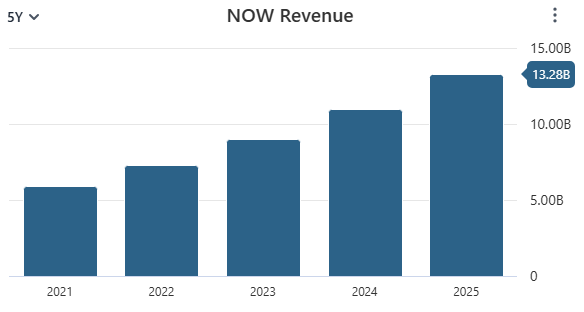

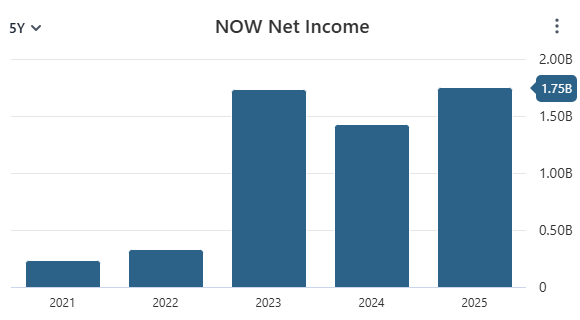

It is here where the top-line’s impressive impact of customer stickiness is evident, despite a stock price down by over 80% in the last year. The company in FY2025 maintained a robust revenue growth to $13.278 billionm, representing 20.89% YoY growth, which is up from $10.984 billion. This is not the first time NOW has recorded such an impressive top-line; it has maintained this upward trend since 2021. Basically, the fears investors had about AI replacing NOW’s SaaS subscription business have not been affected despite the stock plummeting to an unprecedented percentage above 80% in one year. This reveals my stickiness perspective because customers are still deriving more value from AI-integrated SaaS systems and applications. Now that AI agents will be included in various subscriptions, the company might beat analysts’ revenue estimates towards the first quarter at $3.74 billion and second quarter at $3.86 billion in the FY2026. In previous quarters when the investor sell-off had heightened, the company continued beating analyst estimates, demonstrating that there is a strong customer stickiness in ServiceNow.

Even from the earnings perspective, this company shows potential with a net income of $1.748 billion, up from $1.425 net income in FY2024. This represents a net income YoY growth of 22.67%, which is beyond a double-digit figure. You also note that this is the same reason NOW is recording an improving EPS, which also reached $1.67, up from $1.37, representing 21.90% YoY growth. This is a testament that NOW has a solid execution capability, which is why I believe this company has the capability to maintain and improve its clientele base as an alternative to AI agents, as opposed to a replacement.

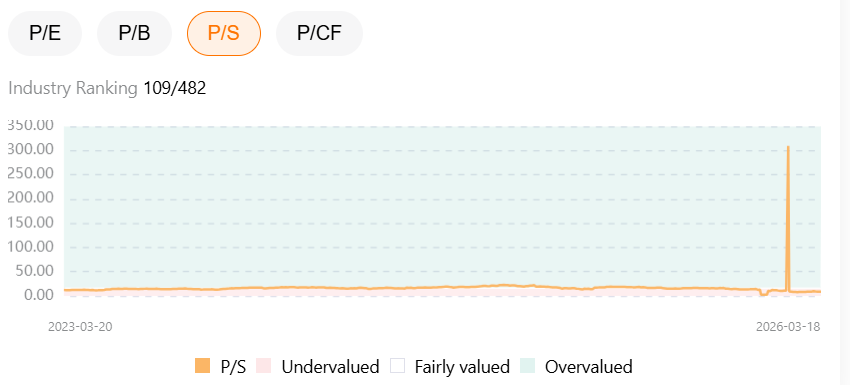

Even looking at valuation, ServiceNow’s P/S multiple to its peers, Palo Alto Networks Inc (NASDAQ: PANW) and Oracle Corp (NASDAQ: ORCL), shows that it is currently undervalued at 9.02x. Compared to its peers, PANW at 7.01x and ORCL at 12.01x, which are fairly valued, you would note that there is a higher chance of upside momentum for NOW.

TradingKey

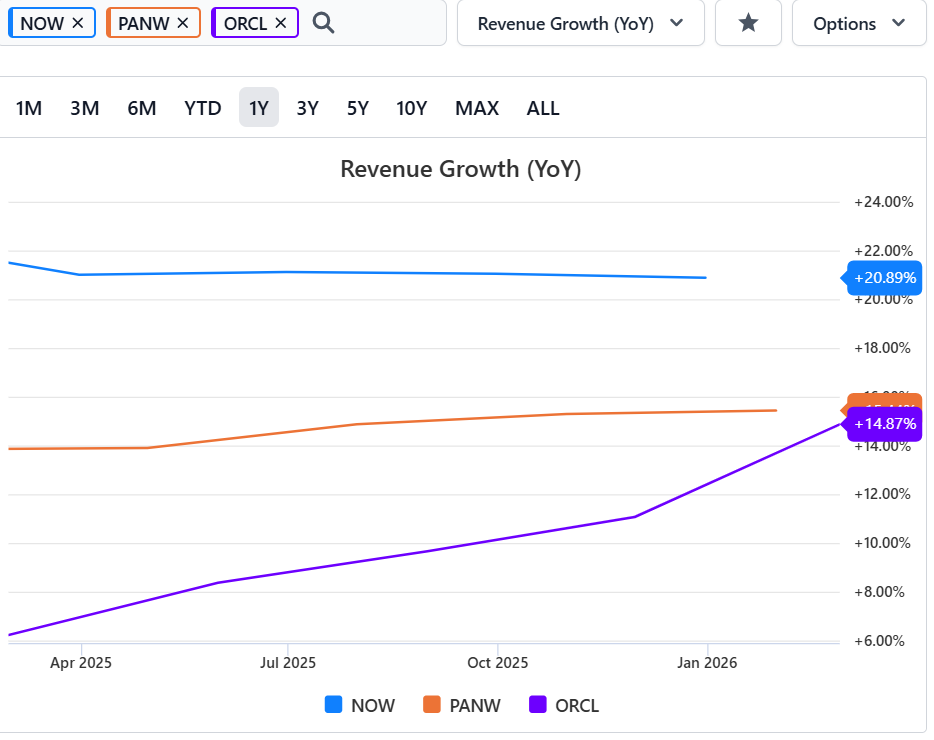

Relating P/S with revenue growth, it brings out the undervaluation perspective even more clearly. For example, among its peers, NOW reigns in terms of revenue growth rate YoY, which is above 20% compared to PANW, ranging around 15%, and ORCL at 14.87%. This means that the NOW financials are strong enough to warrant a bullish momentum as the investor panic sell-off settles.

What Could Go Wrong: Margin Compression Risk From AI Investments

At 98% renewal rate, NOW has customer stickiness, but when you look at the non-GAAP subscription gross margin, it has been declining from 84.5% in Q4’2024 to 82.5% in Q4’2025. This hints that the NOW is maintaining its AI platform at a higher cost currently. Therefore, if AI integration expenses continue to compress its margins, investors may continue to sell off, disapproving of the upside momentum.

The Bottom Line

I believe NOW is well-positioned to execute the AI alternative aspect over a replacement given its resilience during these headwinds in FY2026. Looking at the FY2026 guidance, the non-GAAP increase might reach 20% YoY growth rate from 19.5% in FY2025, which signals the company’s readiness to recover from this headwind, which is why I reiterate my bullish stance.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.