1 Magnificent Growth Stock That Could Crush the Market Over the Next 10 Years

Not all investors want to take a chance on young growth stocks. These stocks are often unprofitable and unpredictable, and they could fall apart and take your money with them.

Some are better bets than others. If you have an appetite for risk, your best course of action is to diversify. That way, even if some companies go bust, you still have a strong chance of coming out on top -- you can only lose the money you put in, but you can gain many times that amount if a stock succeeds.

Global-e Online (NASDAQ: GLBE) is a young e-commerce company that's growing fast, but it's still building its business and moving closer to profitability. It's not a stock for the risk-averse, but there are many reasons to believe it will crush the market over the next decade or more.

Developing a niche e-commerce business

If you've never heard of Global-e, it's because it's a business-to-business company that offers cross-border e-commerce solutions for retailers. It takes care of back-end services and doesn't deal directly with end customers.

The services it offers include things like instant customs calculations and delivery options. It makes it easy for retailers all over the world to reach global shoppers and convert more international sales. As it gathers more information and upgrades its platform, it continues to roll out effective solutions that take it up more notches. For example, it recently added more features for easy returns and more inclusive services for omnichannel shopping, like in-store pickup and use of physical locations for distribution.

It has a long list of top clients you know and likely shop from, such as Disney and Adidas. It has a long pipeline of new clients that it constantly onboards, and it added brands like Doc Martens and Billabong in Q3, in addition to many others. It also expanded its existing partnerships, such as new markets for Disney and new brands from its collaboration with LVMH.

Its most prominent relationship is with e-commerce powerhouse Shopify. Shopify was an early investor in the company, and it offers Global-e's services to all its merchants through a program called Shopify Managed Markets. It was launched last year, and CEO Amir Schlachet said that it "continues to grow as planned and generate great value to the thousands of merchants using it."

Growing and getting closer to profits

Global-e has faced some serious pressure from inflation and from its own customers experiencing slower growth. But with an improved retail landscape and its new Shopify program, sales growth is accelerating as expected. Revenue increased 32% year over year in Q3, driven by a 35% increase in gross merchandise volume (GMV).

It's now in scale mode, leading to improved profitability. Adjusted gross margin expanded from 44.4% to 46.8% in the third quarter, and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) increased from $22.1 million last year to $31.1 million this year. Net loss improved from $33.1 million last year to $22.6 million this year.

Much of the net loss still stems from the amortization of warrants connected to its partnership with Shopify. They will be fully amortized by December next year, and management expects to turn to positive net income on a generally accepted accounting principles (GAAP) basis by the middle of 2025. Global-e already typically generates positive cash from operations and free cash flow.

Management raised its full-year outlook based on the Q3 results, and the market received it warmly.

Is it too late to buy?

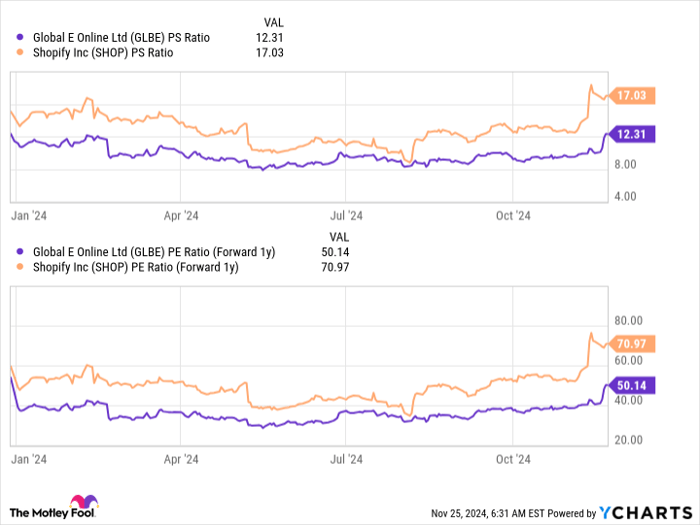

Global-e stock is up 26% this year, and it's not cheap. It trades at a price-to-sales ratio of 12 and a forward, 1-year P/E ratio of 50. That's still a lot cheaper than partner company Shopify, and the ratio is growing faster.

GLBE PS Ratio data by YCharts.

Global-e has a massive opportunity ahead as it brings in new clients, expands its platform, and benefits from an overall lift in global e-commerce. If you have some appetite for risk, it looks like an excellent candidate for a growth stock that could crush the market in the coming years.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $368,053!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $43,533!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $484,170!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of November 25, 2024

Jennifer Saibil has positions in Global-E Online and Walt Disney. The Motley Fool has positions in and recommends Global-E Online, Shopify, and Walt Disney. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.