1 Magnificent Oil Stock Down Nearly 30% to Buy and Hold Forever

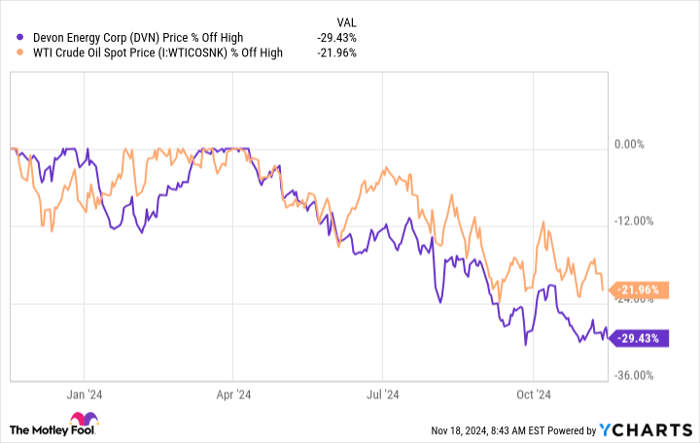

Devon Energy's (NYSE: DVN) stock price has fallen nearly 30% from its 52-week highs. That drop roughly tracks along with the price declines in West Texas Intermediate crude, a key U.S. oil benchmark. But the big story for income investors is that the dividend has now settled at $0.22 per share per quarter. There's a lot to unpack here, but Devon Energy is still a great oil company, even if the dividend is in a state of flux.

What does Devon Energy do?

Devon Energy is a pure play upstream oil and natural gas producer. That means that its top and bottom lines are, effectively, dependent on the price of the commodities it produces. If energy prices are rising, Devon's revenues and earnings will strengthen. If energy prices are falling, Devon's revenues and earnings will weaken. There are no other divisions in the company to soften the blow, as you'd find at an integrated energy company with a business that spans from the upstream (energy production) through the midstream (pipelines) and all the way to the downstream (chemicals and refining).

Image source: Getty Images.

Adding to the upstream focus, Devon's assets are located in the U.S. onshore market. That's not an inherently bad thing, but it limits the company's ability to shift investment and production around to maximize profits. West Texas Intermediate (WTI) crude prices are the key benchmark to watch. Note that in previous years, WTI and Brent crude (a global energy benchmark) have diverged because of operational constraints in the U.S. market.

Devon Energy is a higher-risk way to play the oil sector. If you are a conservative income investor, you'll probably be better off with an integrated energy giant like Chevron. However, there's still a lot to like about Devon Energy.

Devon Energy is growing, leading to some dividend strains

If you can get past the inherent volatility in Devon Energy's business model, it happens to be one of the largest pure play upstream companies in North America. Its production is split roughly evenly between oil and natural gas, providing exposure to both of these key global energy sources. It also has operations in some of the largest and most important U.S. energy drilling basins.

There's plenty of opportunity ahead for Devon. The company estimates that it has at least 10 years of drilling inventory to exploit. It also has a very low breakeven point of around $40 per barrel of oil. The company has an investment grade rated balance sheet.

This is where things get interesting, because Devon Energy just completed a big merger that has increased its leverage. It's targeting debt reduction of $2.5 billion, with $500 million paid down in the third quarter of 2024 alone. The acquisition has boosted the company's growth opportunity, but the plan for debt reduction has come at the expense of the dividend -- sort of.

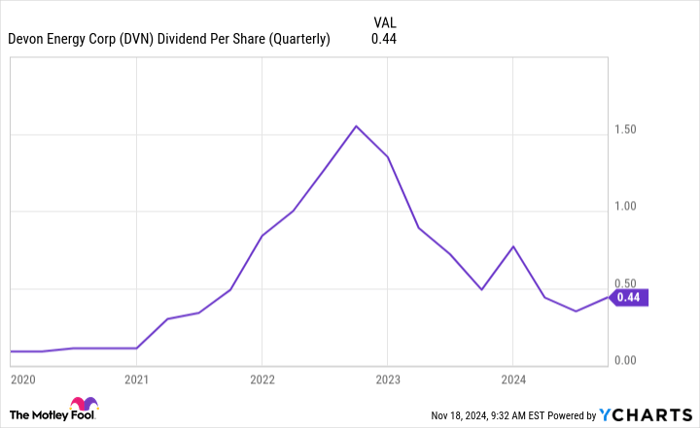

DVN Dividend Per Share (Quarterly) data by YCharts.

Devon Energy has a variable dividend policy, with a base dividend that gets augmented by a variable payment based on financial performance and corporate priorities. The dividend is now sitting at just the base payment of $0.22 per share per quarter. (This isn't shown in the chart above because the dividend hasn't technically been paid yet, even though it has been announced.) That equates to a roughly 2.2% yield, using recent stock prices.

In the prior quarter, the variable portion of the dividend was $0.22, leading to a total dividend payment that was twice the current base level. No wonder the stock is down nearly 30% from its 52-week highs, even though WTI is only down 22% or so!

Right now, Devon Energy isn't exactly an income stock because the financial priority is currently on debt reduction. However, that's not a bad thing after an acquisition and is, in fact, very shareholder-friendly. When the company has finally hit its targeted debt reduction level, it will likely revert back to paying the variable dividend again. After all, it will have to do something with the cash that is no longer being directed toward the balance sheet.

Effectively, for now, the company is a direct play on U.S. energy prices that tosses off a little bit of income. Given that the United States is one of the world's largest energy producers, it's probably a good idea to have some exposure like this in a diversified portfolio. For another year or so, the dividend will play second fiddle to debt reduction. But after that, there's a potential booster for patient income investors, assuming the variable dividend policy resumes.

Hedging your energy exposure

Like it or not, most investors are exposed to energy prices in the real world. That can be related to heating your home or filling your gas tank. If your electricity provider uses natural gas, energy could also be a factor in your electric bill. Owning Devon Energy provides a hedge, to some degree, since it will likely rise in price when energy prices, and your real-world energy costs, are rising.

In a year or so, if the variable dividend comes back, Devon will not only provide an indirect hedge via stock prices appreciation -- it could also give you a very direct hedge via rising dividend payments when energy prices (and your costs) go up. The first hedge is worth putting into your portfolio and leaving there for the long term. If the second, dividend-related, hedge comes to fruition, you could be a winner two times over.

Should you invest $1,000 in Devon Energy right now?

Before you buy stock in Devon Energy, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Devon Energy wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $900,893!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 18, 2024

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chevron. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.