Marvell Technology Inc Stock (MRVL) Moved Down by 6.62% on Jul 15: What Investors Need To Know

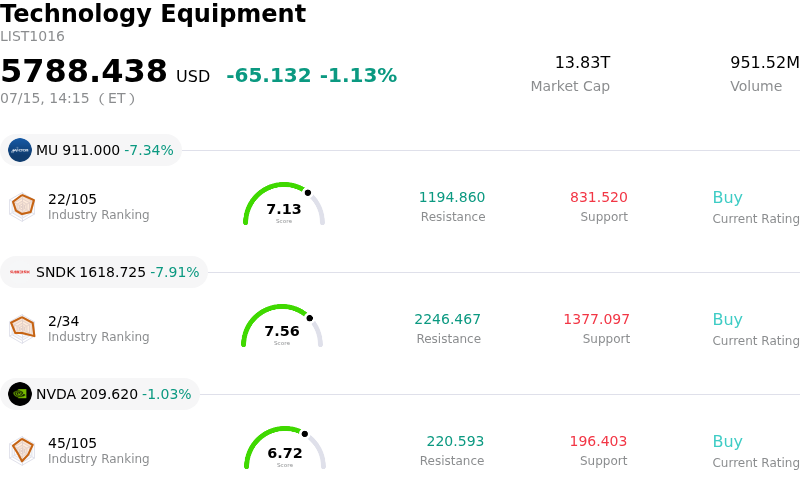

Marvell Technology Inc (MRVL) moved down by 6.62%. The Technology Equipment sector is down by 1.13%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 7.34%; SanDisk Corporation (SNDK) down 7.91%; NVIDIA Corp (NVDA) down 0.98%.

What is driving Marvell Technology Inc (MRVL)’s stock price down today?

The decline in Marvell Technology shares is primarily driven by a broader rotation out of the semiconductor sector following revised capital expenditure forecasts from major hyperscale cloud providers. Investors are increasingly concerned that the initial surge in artificial intelligence infrastructure spending is entering a digestion phase, leading to a temporary slowdown in orders for optical interconnects and custom silicon solutions. This sentiment is exacerbated by reports of intensified competition in the application-specific integrated circuit market, where Marvell faces mounting pressure from both traditional rivals and internal chip development programs at large technology firms.

Additionally, recent industry data suggests that while demand for AI-driven networking remains relatively stable, the recovery in the traditional enterprise networking and carrier infrastructure segments has been slower than anticipated. Marvell’s significant exposure to these lagging end-markets is weighing on its short-term growth outlook. Furthermore, rumors regarding a shift in architectural preferences for next-generation data centers favoring integrated solutions over modular components have sparked fears regarding the company's long-term margin profile and its ability to maintain high average selling prices in an increasingly commoditized hardware environment.

On the macroeconomic front, persistent inflationary signals have dampened hopes for aggressive interest rate cuts, leading to a general de-risking of high-growth technology stocks. As a company with a premium valuation tied to aggressive future earnings growth, Marvell is particularly sensitive to fluctuations in the discount rate. The breach of key technical support levels during today's session has also triggered automated selling programs and retail profit-taking, further accelerating the downward momentum. Institutional rebalancing ahead of the upcoming earnings season suggests a more cautious stance among fund managers who are now seeking more concrete evidence of sustained revenue acceleration beyond the AI hype cycle.

Technical Analysis of Marvell Technology Inc (MRVL)

Technically, Marvell Technology Inc (MRVL) shows a MACD (12,26,9) value of -18.296, indicating a neutral signal. The RSI at 42.626 suggests neutral condition and the Williams %R at 91.549 suggests oversold condition. Please monitor closely.

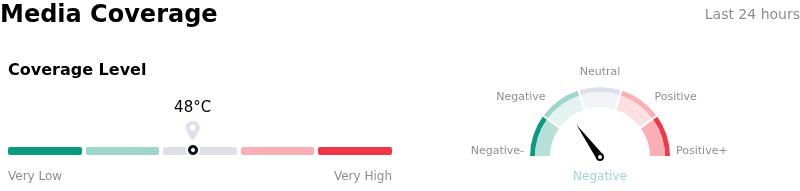

Media Coverage of Marvell Technology Inc (MRVL)

In terms of media coverage, Marvell Technology Inc (MRVL) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Marvell Technology Inc (MRVL)

Marvell Technology Inc (MRVL) is in the Technology Equipment industry. Its latest annual revenue is $8.19B, ranking 18 in the industry. The net profit is $2.67B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $246.16, a high of $400.00, and a low of $90.00.

More details about Marvell Technology Inc (MRVL)

Company Specific Risks:

- Segmented Revenue Divergence: Persistent double-digit revenue contractions in the carrier infrastructure and enterprise networking divisions are currently offsetting high-growth AI contributions, creating a volatile financial profile that relies heavily on a single product category to maintain top-line stability.

- Custom ASIC Margin Compression: Intensifying competition from Broadcom and the strategic shift of major hyperscalers toward internal silicon development threaten Marvell’s long-term market share and may force aggressive pricing strategies that erode gross margins in the custom AI accelerator segment.

- Inventory Digestion Cycles: Institutional analysts have raised red flags regarding the prolonged recovery timeline for the automotive and industrial end-markets, suggesting that excess hardware inventory among tier-one suppliers is dampening near-term guidance expectations.

- Execution Risk on Advanced Nodes: The transition to 3nm and 2nm process technologies introduces significant technical hurdles and higher R&D expenditure, where any manufacturing delays or yield issues at foundry partners could result in missed product launch windows for next-generation optical interconnects.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.