Lam Research Corp Stock (LRCX) Moved Down by 6.34% on Jul 15: A Full Analysis

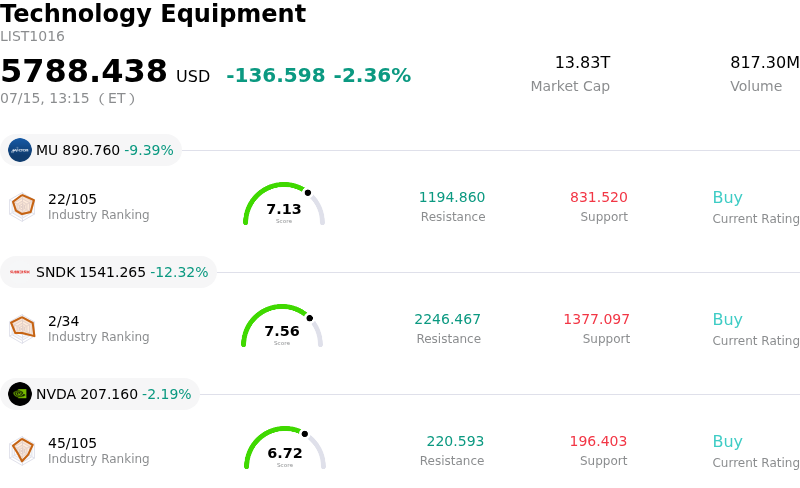

Lam Research Corp (LRCX) moved down by 6.34%. The Technology Equipment sector is down by 2.36%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 9.39%; SanDisk Corporation (SNDK) down 12.32%; NVIDIA Corp (NVDA) down 2.19%.

What is driving Lam Research Corp (LRCX)’s stock price down today?

The sharp decline in Lam Research's market value reflects a broader contraction within the semiconductor capital equipment sector, often triggered by shifting expectations in global wafer fabrication spending. As a primary provider of etch and deposition tools, the company is highly sensitive to the capital expenditure cycles of major foundry and memory manufacturers. When industry leaders or key customers signal a potential reduction in equipment procurement or a delay in capacity expansion, institutional investors frequently rotate out of high-beta semiconductor names to mitigate exposure to cyclical volatility.

Geopolitical tensions continue to serve as a primary headwind for the company, particularly regarding export or trade restrictions involving advanced logic and memory nodes. Because a significant portion of the company’s revenue is derived from international markets, any regulatory movement that threatens the flow of high-end chipmaking machinery creates immediate uncertainty. Investors are likely reacting to perceived risks that could limit the company's long-term total addressable market or disrupt established supply chains in critical manufacturing hubs.

The memory market's inherent cyclicity also plays a crucial role in the current downward pressure. Lam Research holds a dominant position in the production of NAND and DRAM hardware, making its performance closely tied to the health of the memory sector. If market data suggests an oversupply of memory chips or a slowing transition to next-generation high-bandwidth memory architectures, the demand for new fabrication tools naturally softens. This leads to a recalibration of earnings expectations as analysts adjust for a potentially leaner period of equipment orders.

From a macroeconomic standpoint, the prevailing high-interest-rate environment and hawkish central bank sentiment weigh heavily on growth-oriented technology stocks. As a capital-intensive enterprise, the company’s valuation is sensitive to fluctuations in the cost of capital and broader shifts in risk appetite. The observed intraday volatility suggests that market participants are re-evaluating the stock's premium in light of persistent inflationary pressures and the potential for a slowdown in global industrial production, which could curb the long-term growth trajectory of the semiconductor industry.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of -15.924, indicating a neutral signal. The RSI at 48.621 suggests neutral condition and the Williams %R at 73.684 suggests sell condition. Please monitor closely.

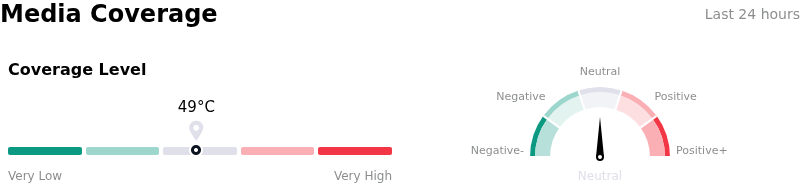

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $359.85, a high of $480.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Geopolitical Revenue Concentration: With approximately 37% of recent quarterly revenue derived from China, the company remains highly susceptible to tightening U.S. export controls on advanced semiconductor manufacturing equipment, particularly regarding Gate-All-Around (GAA) architectures.

- Sluggish NAND Market Recovery: While High Bandwidth Memory (HBM) demand is robust, the broader recovery in traditional NAND flash memory capital expenditure is progressing slower than anticipated, potentially capping the growth of Lam’s etch and deposition segments through the next fiscal year.

- Domestic Competition in Mature Nodes: Institutional analysts are concerned about the "peak China" equipment cycle as domestic Chinese competitors gain market share in non-critical and mature nodes, threatening Lam's long-term dominance in a region that has recently sustained its revenue beats.

- Inventory Digestion Headwinds: Recent analyst commentary suggests a potential "digestion period" for major logic and foundry customers who front-loaded equipment orders in early 2024, creating a risk of sequential deceleration in tool shipments and billings in the coming quarters.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.