Intel Corp Stock (INTC) Moved Down by 5.34% on Jul 15: What Signal Does It Send?

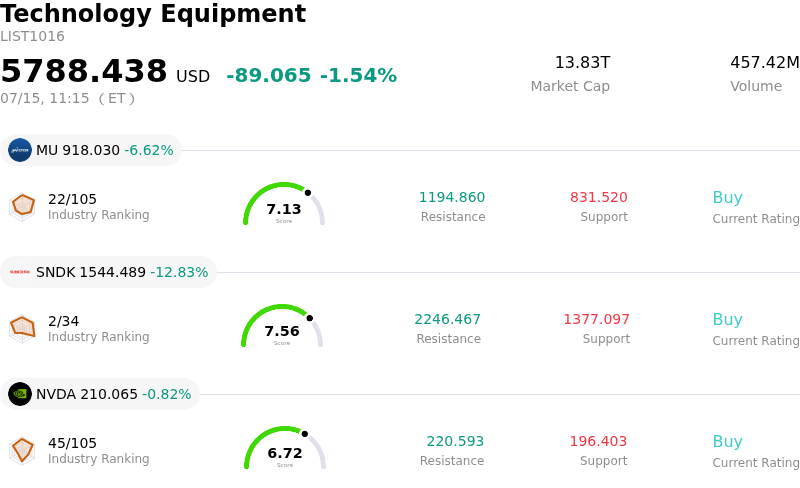

Intel Corp (INTC) moved down by 5.34%. The Technology Equipment sector is down by 1.54%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 6.96%; SanDisk Corporation (SNDK) down 12.83%; NVIDIA Corp (NVDA) down 0.82%.

What is driving Intel Corp (INTC)’s stock price down today?

The recent decline in Intel shares reflects a growing skepticism regarding the timeline and execution of the company's multi-year turnaround strategy. Market participants are reacting to a combination of internal execution risks and a shifting competitive landscape that continues to favor rivals in the high-performance computing and artificial intelligence sectors. This downward movement is compounded by investor anxiety over the massive capital requirements needed to sustain the company's pivot toward a foundry-heavy business model.

A primary driver for the current downward pressure stems from reports suggesting potential delays in the ramp-up of the company's next-generation manufacturing nodes. As the company attempts to regain process leadership, any perceived friction in its roadmap creates concerns about its ability to secure large-scale external customers. This is particularly sensitive given the heavy capital expenditures required to build out domestic fabrication capacity, which places a significant strain on free cash flow and near-term profit margins.

Investors are also weighing the company's position in the lucrative AI accelerator market. While new products have been launched to capture data center demand, dominant competitors continue to hold a significant lead in software ecosystems and hardware performance. The lack of a clear, immediate catalyst to bridge this gap is leading institutional investors to rotate capital into other semiconductor players that offer more visible growth trajectories in the short term. This rotation often exacerbates intraday volatility during periods of high market sensitivity.

On a broader scale, cautious commentary from industry analysts regarding the recovery of the global PC market has dampened sentiment. With inventory levels remaining a concern in certain enterprise segments, the anticipation of a slower-than-expected rebound in consumer hardware spending is impacting revenue projections. Furthermore, recent adjustments in institutional portfolios ahead of the upcoming earnings season suggest a defensive posture, as funds mitigate exposure to companies with high operational complexity and ongoing structural transitions.

The current volatility highlights the delicate balance the firm must maintain between its legacy business and its future as a foundry leader. Risk factors including geopolitical tensions affecting the global supply chain and the potential for further analyst downgrades continue to weigh on the stock. Until there is more concrete evidence of yield improvements and significant foundry contract wins, the market remains inclined toward a cautious valuation.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of -6.786, indicating a neutral signal. The RSI at 43.212 suggests neutral condition and the Williams %R at 85.281 suggests oversold condition. Please monitor closely.

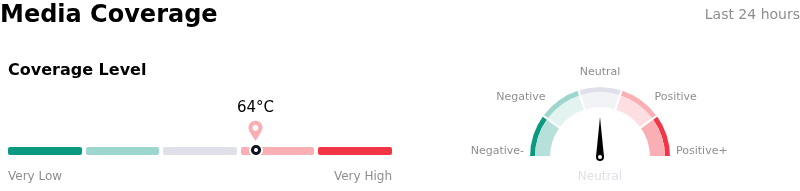

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 64, indicating a high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $101.64, a high of $200.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Foundry Financial Drag: Sustained quarterly losses within the Intel Foundry segment and massive capital expenditure requirements for domestic fab expansion continue to strain the balance sheet, leading to heightened concerns over liquidity and potential credit rating downgrades.

- Competitive Market Share Erosion: Rapid adoption of ARM-based architectures and aggressive market share gains by AMD in the data center and AI PC segments are threatening Intel's traditional revenue strongholds and forcing margin-compressing price adjustments.

- Restructuring and Talent Attrition: The execution of a massive cost-reduction program, including significant workforce reductions, creates internal instability and risks the loss of critical engineering talent necessary to meet the ambitious "Intel 18A" manufacturing roadmap.

- M&A and Divestiture Uncertainty: Ongoing speculation regarding potential takeovers, private equity investments, or the forced divestiture of core business units like Altera has introduced significant structural uncertainty and increased intraday price sensitivity to unconfirmed reports.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.