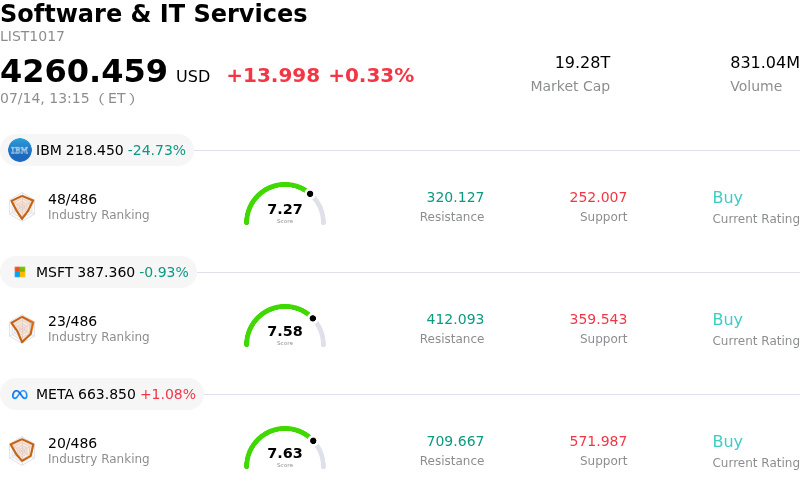

International Business Machines Corp Stock (IBM) Moved Down by 24.63% on Jul 14: A Full Analysis

International Business Machines Corp (IBM) moved down by 24.63%. The Software & IT Services sector is up by 0.33%. The company underperformed the industry. Top 3 stocks by turnover in the sector: International Business Machines Corp (IBM) down 24.63%; Microsoft Corp (MSFT) down 0.93%; Meta Platforms Inc (META) up 1.08%.

What is driving International Business Machines Corp (IBM)’s stock price down today?

IBM's sharp decline reflects a crisis of confidence in its long-term AI and hybrid cloud strategy. The primary catalyst appears to be a dual failure involving a significant security vulnerability discovered within its core enterprise infrastructure and a drastic downward revision of its annual revenue guidance. For a company that has positioned itself as the bedrock of secure enterprise computing, a breach of this magnitude undermines the fundamental value proposition of its software and consulting segments.

The company’s recent financial disclosures revealed that the anticipated growth from generative AI integration has failed to materialize at the scale previously communicated to the market. While competitors have successfully monetized their AI stacks, IBM is reporting a significant contraction in its consulting pipeline as clients pause long-term projects due to security concerns and budget reallocations. This shortfall is exacerbated by the unexpected suspension of its share buyback program and a sharp reduction in dividend payouts, which has historically been a primary reason for institutional and retail support of the stock.

The competitive landscape is becoming increasingly hostile as hyper-scalers continue to erode IBM’s market share in the hybrid cloud space. With the emergence of more agile, specialized AI firms, IBM’s legacy systems are increasingly viewed as a drag on innovation rather than a stable foundation. Institutional investors are reacting to the possibility that IBM’s transition to a high-growth cloud and AI company has stalled, leading to a massive sell-off as funds rebalance away from what is now perceived as a value trap.

General market sentiment is being further weighed down by broader macroeconomic concerns, including tightening credit conditions that make large-scale digital transformations more expensive for IBM's client base. The combination of internal operational failures and external economic pressures has triggered high-volume liquidations, with many institutional desks moving to a neutral or underweight position. Without a clear path to restoring trust in its security protocols and proving the viability of its AI revenue model, the company faces a prolonged period of volatility and downward pressure.

Technical Analysis of International Business Machines Corp (IBM)

Technically, International Business Machines Corp (IBM) shows a MACD (12,26,9) value of 1.800, indicating a buy signal. The RSI at 56.652 suggests neutral condition and the Williams %R at 38.150 suggests buy condition. Please monitor closely.

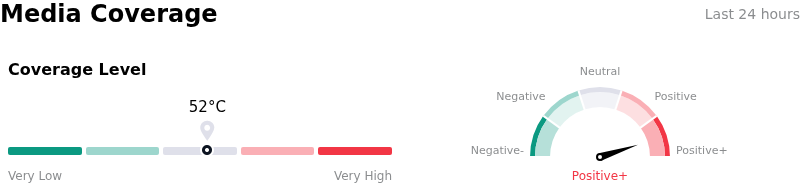

Media Coverage of International Business Machines Corp (IBM)

In terms of media coverage, International Business Machines Corp (IBM) shows a coverage score of 52, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bullish zone.

Fundamental Analysis of International Business Machines Corp (IBM)

International Business Machines Corp (IBM) is in the Software & IT Services industry. Its latest annual revenue is $67.53B, ranking 7 in the industry. The net profit is $10.59B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $288.22, a high of $375.00, and a low of $195.00.

More details about International Business Machines Corp (IBM)

Company Specific Risks:

- Consulting Revenue Deceleration: IBM reported a significant slowdown in its Consulting segment during the third quarter, with growth stalling at 0.5% as enterprise clients pull back on discretionary spending and prioritize cost-saving measures over large-scale digital transformations.

- Infrastructure Segment Cyclicality: The Infrastructure division is facing immediate headwinds as the current z16 mainframe product cycle matures, resulting in a year-over-year revenue decline and a projected lull in hardware sales until the next-generation cycle begins in late 2025.

- Missed Revenue Expectations: The company missed consolidated quarterly revenue estimates due to weaknesses in both Infrastructure and Consulting, leading to institutional concerns that Software growth alone cannot sustain the firm's mid-single-digit growth guidance.

- AI Pipeline Conversion Lag: Despite a generative AI book of business reaching $3 billion, analysts are concerned about the slow conversion rate of these bookings into realized revenue and the potential for these high-margin AI projects to cannibalize traditional, lower-margin service offerings.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.