ASML Holding NV Stock (ASML) Moved Down by 3.22% on Jul 13: Key Drivers Unveiled

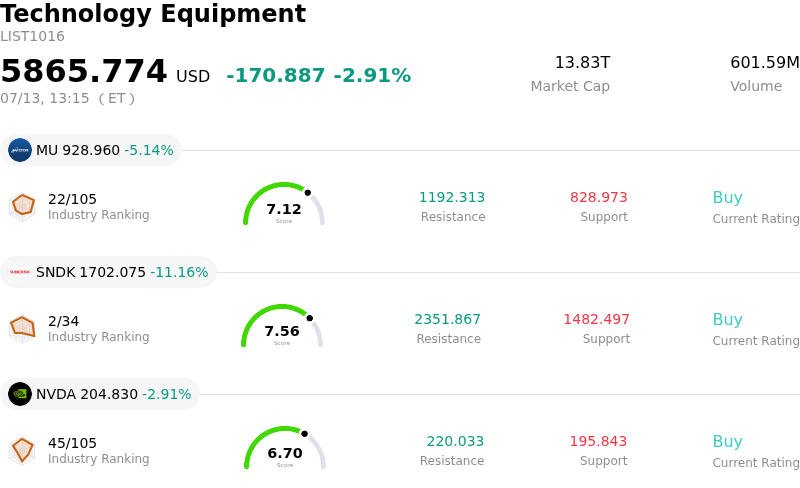

ASML Holding NV (ASML) moved down by 3.22%. The Technology Equipment sector is down by 2.91%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 5.00%; SanDisk Corporation (SNDK) down 11.37%; NVIDIA Corp (NVDA) down 2.91%.

What is driving ASML Holding NV (ASML)’s stock price down today?

ASML’s downward pressure stems from a combination of geopolitical tensions and cautious sentiment within the semiconductor equipment sector. Reports suggesting further tightening of export licenses for high-end lithography systems have reignited concerns regarding the company’s long-term revenue streams from key international markets. This regulatory uncertainty creates a valuation overhang, as investors recalibrate the growth trajectory for both deep ultraviolet and extreme ultraviolet machines in a fragmenting global trade environment.

The decline is further exacerbated by recent updates from major chipmakers indicating a potential moderation in capital expenditure for the upcoming fiscal cycle. As a primary supplier to the world's leading foundries, any signal of a slowdown in fab expansion plans or a delay in tool move-ins directly impacts ASML's order backlog visibility. While the structural demand for high-end logic and memory driven by artificial intelligence remains intact, the broader softening in consumer electronics and automotive segments is leading some clients to exercise caution, contributing to the intraday volatility seen across the equipment peer group.

From a macroeconomic perspective, a shift in sovereign bond yields has placed renewed pressure on high-multiple technology stocks. As institutional investors pivot toward defensive sectors in response to persistent inflationary signals and central bank rhetoric, large-cap growth names like ASML often face tactical de-risking. The absence of immediate positive catalysts ahead of the next quarterly earnings call has left the stock vulnerable to profit-taking, especially following its previous period of outperformance relative to the broader technology index.

Looking ahead, the primary risk remains the potential for more stringent multilateral trade agreements that could further restrict the servicing and maintenance of the existing installed base. While ASML maintains a near-monopoly position in advanced lithography, the push for domestic semiconductor sovereignty in various regions introduces operational complexities and cost pressures. Investors are currently weighing these long-term geopolitical hurdles against the company's technological leadership, leading to the current defensive positioning in the market.

Technical Analysis of ASML Holding NV (ASML)

Technically, ASML Holding NV (ASML) shows a MACD (12,26,9) value of -37.762, indicating a neutral signal. The RSI at 51.231 suggests neutral condition and the Williams %R at 71.693 suggests sell condition. Please monitor closely.

Fundamental Analysis of ASML Holding NV (ASML)

ASML Holding NV (ASML) is in the Technology Equipment industry. Its latest annual revenue is $36.83B, ranking 7 in the industry. The net profit is $10.83B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1846.85, a high of $2500.00, and a low of $994.01.

More details about ASML Holding NV (ASML)

Company Specific Risks:

- Legislative Escalation of Export Controls: The proposed Multilateral Approval of Technology Controls for Hardware (MATCH) Act in the U.S. threatens to prohibit the sale and, more critically, the ongoing maintenance and servicing of Deep Ultraviolet (DUV) immersion lithography systems in China, potentially impacting a high-margin service segment.

- Regulatory Compliance Scrutiny: U.S. Commerce Department officials recently voiced public concern (June 2026) regarding reports that High-End Extreme Ultraviolet (EUV) components may have entered the Chinese market in violation of existing bans, raising the immediate threat of intensified federal audits or expanded unilateral sanctions.

- Structural Revenue Normalization in China: ASML projections indicate a sharp contraction in China-based revenue share, forecasted to drop from approximately 33% in 2025 to 20% in 2026 as local customers face equipment bans and the broader market shifts toward domestic lithography alternatives.

- Valuation Sensitivity Ahead of Earnings: With the Q2 2026 earnings report scheduled for July 15, the stock’s current multiple—trading near 58x trailing earnings—leaves no room for margin compression, making the share price highly vulnerable to any conservative guidance regarding the second half of the fiscal year.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.