Shopify Inc Stock (SHOP) Moved Up by 3.12% on Jul 13: What Investors Need To Know

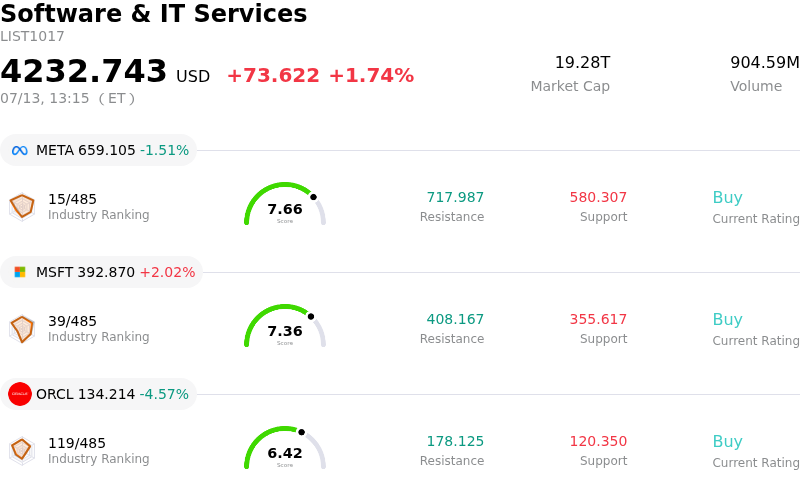

Shopify Inc (SHOP) moved up by 3.12%. The Software & IT Services sector is up by 1.74%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Meta Platforms Inc (META) down 1.51%; Microsoft Corp (MSFT) up 2.02%; Oracle Corp (ORCL) down 4.57%.

What is driving Shopify Inc (SHOP)’s stock price up today?

Shopify is experiencing notable upward momentum as the broader e-commerce sector benefits from a stabilizing macroeconomic environment and resilient consumer spending patterns. Institutional investors appear to be increasing their exposure to high-growth software platforms as market sentiment shifts toward a more favorable outlook for the technology sector. The company’s focus on high-margin software services and its successful transition away from capital-intensive logistics operations continue to resonate with the investment community, providing a solid foundation for valuation expansion.

A primary driver for the current price movement is the positive feedback surrounding the company’s latest advancements in artificial intelligence. By integrating sophisticated generative AI tools into its merchant dashboard, the platform has managed to significantly lower the barrier to entry for new entrepreneurs while enhancing the operational efficiency of established brands. Recent industry data suggests that these technological enhancements are leading to higher merchant retention and improved conversion rates, which are critical metrics for the company’s long-term revenue growth.

The market is also reacting to a series of bullish adjustments from equity analysts who have raised their price targets in anticipation of the upcoming earnings cycle. There is a growing consensus that the company is effectively capturing market share from traditional retail competitors by expanding its enterprise-level offerings. The success of its commerce components strategy has allowed it to attract larger, more complex global brands, thereby diversifying its merchant base and reducing sensitivity to the cyclicality of small-business spending.

Intraday volatility remains elevated as the stock attracts significant attention from both retail and institutional participants. While the immediate trend is positive, investors are closely monitoring potential risks, including currency fluctuations and the impact of geopolitical tensions on global supply chains. However, the company’s strong balance sheet and its ability to generate consistent free cash flow have positioned it as a preferred pick for those looking to capitalize on the ongoing digital transformation of the global retail landscape.

The current activity suggests a repositioning of portfolios toward leaders in the digital economy that demonstrate a clear path to sustained profitability. As the company continues to refine its ecosystem and expand its suite of financial services, including its payments and lending arms, it remains well-positioned to maintain its leadership status. The combination of product innovation and disciplined expense management continues to be the primary catalyst for the stock’s performance in the current market environment.

Technical Analysis of Shopify Inc (SHOP)

Technically, Shopify Inc (SHOP) shows a MACD (12,26,9) value of 2.017, indicating a buy signal. The RSI at 59.533 suggests neutral condition and the Williams %R at 33.172 suggests buy condition. Please monitor closely.

Fundamental Analysis of Shopify Inc (SHOP)

Shopify Inc (SHOP) is in the Software & IT Services industry. Its latest annual revenue is $11.56B, ranking 32 in the industry. The net profit is $1.23B, ranking 39 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $150.29, a high of $200.00, and a low of $110.00.

More details about Shopify Inc (SHOP)

Company Specific Risks:

- Decelerating Revenue Guidance: Management's outlook for the upcoming quarter projects revenue growth in the "mid-to-high teens" percentage range, a significant slowdown from the 23% growth achieved in the prior quarter, missing consensus analyst expectations.

- Operating Expense Expansion: Forecasts for a sequential increase in operating expenses—driven by aggressive marketing spend and research development—are raising concerns that rising costs will offset recent efficiency gains and suppress operating margins.

- Gross Margin Headwinds: The structural impact of divesting the logistics business, combined with a higher mix of lower-margin payments revenue, continues to create downward pressure on gross margins, complicating the path to sustainable profitability.

- Free Cash Flow Margin Sensitivity: Recent volatility is linked to investor disappointment over single-digit free cash flow margin projections, suggesting that the company’s transition from a growth-at-all-costs model to a profit-focused one is facing execution hurdles.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.