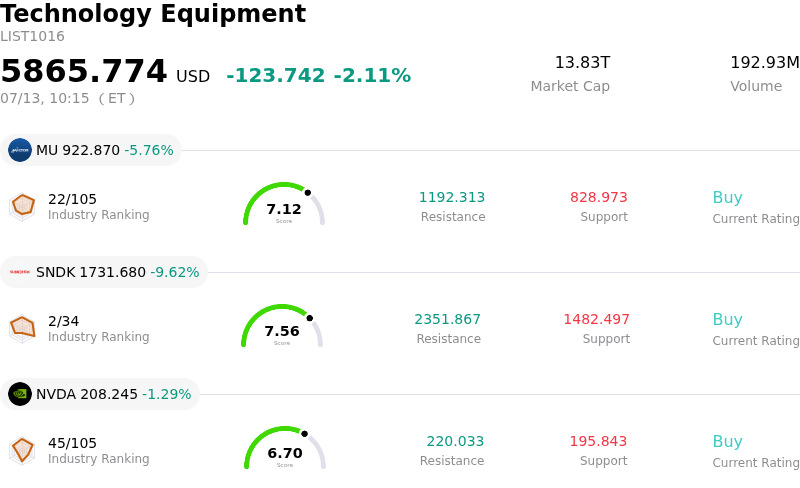

Micron Technology Inc Stock (MU) Moved Down by 5.76% on Jul 13: What Signal Does It Send?

Micron Technology Inc (MU) moved down by 5.76%. The Technology Equipment sector is down by 2.11%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 5.76%; SanDisk Corporation (SNDK) down 9.62%; NVIDIA Corp (NVDA) down 1.29%.

What is driving Micron Technology Inc (MU)’s stock price down today?

Micron Technology is currently experiencing a period of intense selling pressure as broader market concerns regarding the sustainability of the memory chip cycle begin to weigh on investor sentiment. The primary driver appears to be a shift in expectations surrounding the supply-demand balance for high-bandwidth memory, a critical component for artificial intelligence applications. Recent industry data suggests that production yields across the sector are improving faster than anticipated, leading to fears that the supply shortage which previously supported premium pricing may be nearing an end.

This downward movement is further exacerbated by cautious outlooks from major original equipment manufacturers in the personal computer and smartphone segments. While the enterprise server market remains a pillar of strength, the recovery in consumer-facing hardware has been more sluggish than many analysts initially projected. This discrepancy is raising alarms about inventory levels for standard DRAM and NAND products, prompting institutional investors to reduce their exposure to highly cyclical semiconductor names in favor of more defensive positions.

On the macroeconomic front, persistent uncertainty regarding the Federal Reserve's long-term interest rate path is disproportionately affecting high-growth technology companies. As a capital-intensive business, Micron is particularly sensitive to changes in the cost of financing for its multi-billion dollar fabrication facility expansions. Additionally, escalating geopolitical tensions and potential new restrictions on semiconductor equipment exports have introduced a layer of regulatory risk that is currently being priced into the stock, particularly concerning trade dynamics in the Asia-Pacific region.

Market sentiment has also been dampened by a series of analyst notes questioning whether the valuation of AI-linked hardware providers has overextended itself relative to actual earnings growth. Despite Micron's strong competitive position and technological leadership, the recent intraday volatility suggests a lack of conviction among buyers at current levels. As the industry prepares for the next round of quarterly financial disclosures, the focus has shifted from top-line revenue growth to gross margin preservation in an increasingly competitive landscape where rivals are aggressively expanding capacity.

Technical Analysis of Micron Technology Inc (MU)

Technically, Micron Technology Inc (MU) shows a MACD (12,26,9) value of -56.954, indicating a neutral signal. The RSI at 49.123 suggests neutral condition and the Williams %R at 75.879 suggests sell condition. Please monitor closely.

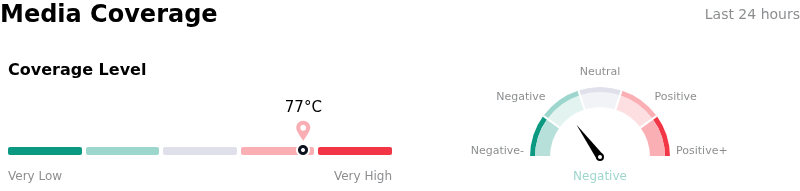

Media Coverage of Micron Technology Inc (MU)

In terms of media coverage, Micron Technology Inc (MU) shows a coverage score of 77, indicating a high level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Micron Technology Inc (MU)

Micron Technology Inc (MU) is in the Technology Equipment industry. Its latest annual revenue is $37.38B, ranking 6 in the industry. The net profit is $8.54B, ranking 5 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1449.24, a high of $2000.00, and a low of $190.00.

More details about Micron Technology Inc (MU)

Company Specific Risks:

- Conservative Revenue Guidance: Despite exceeding Q3 earnings estimates, the company’s Q4 revenue guidance of $7.6 billion only met analyst consensus rather than exceeding it, failing to satisfy elevated market "whisper numbers" and triggering a valuation contraction as AI-driven growth expectations were recalibrated.

- High Bandwidth Memory (HBM) Capacity Constraints: Management confirmed that HBM supply is already fully allocated through the end of calendar year 2025, which effectively caps the company’s immediate-term revenue upside and prevents it from capitalizing further on additional spot-market demand spikes.

- Aggressive Capital Expenditure Requirements: Micron projected a significant increase in CapEx for FY2025 to mid-30s as a percentage of revenue to support HBM3E production and infrastructure, creating concerns regarding near-term free cash flow pressure and the long-term risk of oversupply if AI demand growth begins to plateau.

- Sluggish Recovery in Non-AI Segments: Persistent inventory adjustments and tepid demand in the traditional PC and smartphone end-markets continue to act as a drag on overall margins, highlighting a fundamental dependence on the volatile data center segment to sustain current stock premiums.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.