Intel Corp Stock (INTC) Moved Down by 3.64% on Jul 10: What Investors Need To Know

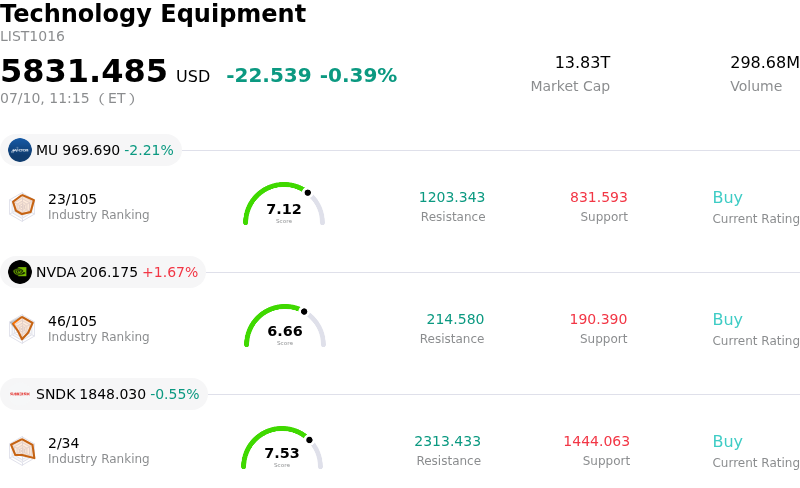

Intel Corp (INTC) moved down by 3.64%. The Technology Equipment sector is down by 0.39%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 2.21%; NVIDIA Corp (NVDA) up 1.67%; SanDisk Corporation (SNDK) down 0.55%.

What is driving Intel Corp (INTC)’s stock price down today?

Intel is experiencing notable downward pressure as market participants react to mounting concerns over the execution of its advanced node manufacturing timeline. Despite the company's aggressive efforts to regain process leadership, recent industry reports suggest that yield improvements for its next-generation foundry processes may be trailing behind internal targets. This perceived delay in reaching volume production for external clients is weighing heavily on investor confidence, particularly as the foundry segment remains the cornerstone of the company's long-term turnaround strategy.

The competitive landscape in the data center and artificial intelligence sectors continues to shift. While the firm has launched new iterations of its AI-focused hardware, the market remains skeptical of its ability to erode the dominant market share held by leading GPU manufacturers. Simultaneously, its primary rival in the x86 processor space continues to secure design wins with major hyperscalers, leading to fears that the company’s market share in the lucrative server segment has not yet found a definitive floor.

Macroeconomic headwinds are exacerbating the stock's sensitivity to negative news. As a capital-intensive business requiring billions in infrastructure investment, the company is particularly vulnerable to shifts in federal monetary policy and the rising cost of debt. Recent signals regarding sustained higher interest rates have cooled institutional appetite for companies with high capital expenditure profiles and longer paths to significant profitability. This has prompted several investment banks to adjust their outlooks, triggering a wave of institutional portfolio rebalancing.

Furthermore, a broader cooling of sentiment across the semiconductor industry is impacting valuations. Following a period of intense enthusiasm for artificial intelligence infrastructure, investors are increasingly demanding tangible evidence of return on investment. The lack of immediate breakthroughs in the contract manufacturing business model leaves the company exposed to volatility whenever industry peers report softening demand in consumer electronics or enterprise hardware. Until a stabilized margin profile can be demonstrated and a landmark multi-year contract for cutting-edge nodes is secured, the stock is likely to face continued technical resistance.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of -6.397, indicating a neutral signal. The RSI at 44.977 suggests neutral condition and the Williams %R at 78.571 suggests sell condition. Please monitor closely.

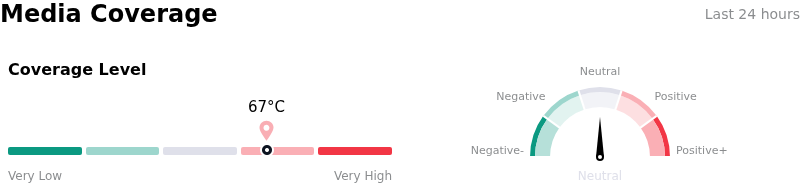

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 67, indicating a high level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $97.33, a high of $200.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Competitive Architecture Shift: The recent launch of Microsoft’s Copilot+ PCs utilizing Qualcomm’s ARM-based Snapdragon X Elite processors has significantly increased the threat to Intel’s x86 dominance, creating immediate concerns regarding market share erosion in the high-margin AI laptop segment.

- Geopolitical Export Constraints: The U.S. Department of Commerce’s recent decision to revoke export licenses for chip shipments to Huawei has introduced a direct revenue headwind and heightened the risk of further retaliatory trade measures from China, which remains a critical market for Intel’s consumer and enterprise divisions.

- Foundry Operational Losses: Institutional focus remains high on the significant operating losses within the Intel Foundry segment, where the massive capital expenditure required for the "5 nodes in 4 years" strategy and the integration of High-NA EUV lithography is severely compressing consolidated gross margins.

- Execution Risk in AI Accelerators: Despite the rollout of Gaudi 3, market analysts have highlighted Intel’s struggle to secure large-scale enterprise commitments compared to NVIDIA’s H200 and AMD’s MI300X, suggesting a fundamental lag in the company’s ability to monetize the generative AI infrastructure boom.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.