Arm Holdings PLC Stock (ARM) Moved Up by 11.16% on Jul 9: A Full Analysis

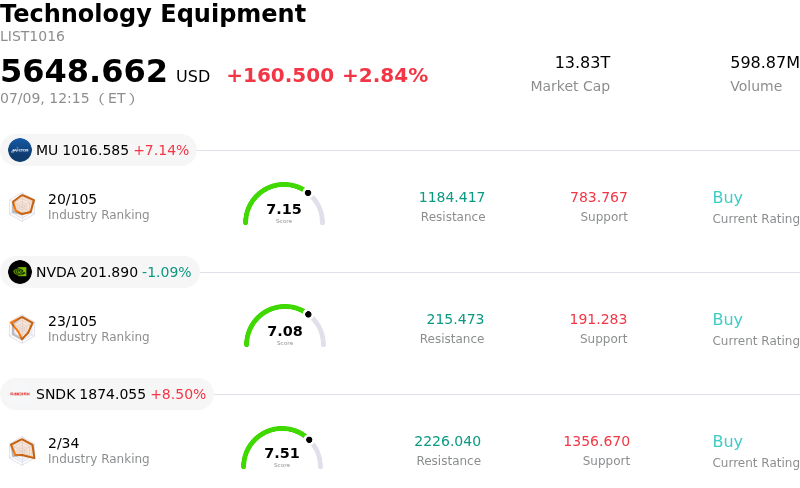

Arm Holdings PLC (ARM) moved up by 11.16%. The Technology Equipment sector is up by 2.84%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 7.22%; NVIDIA Corp (NVDA) down 1.09%; SanDisk Corporation (SNDK) up 8.50%.

What is driving Arm Holdings PLC (ARM)’s stock price up today?

Arm Holdings experienced notable upward price movement and significant intraday volatility, driven by a convergence of strong industry dynamics, positive fundamental indicators, and shifting market sentiment in the artificial intelligence and semiconductor sectors. This momentum highlights the company's central role in the expanding physical AI and data center ecosystem.

A primary catalyst for the positive movement is the growing market realization of Arm's structural positioning within AI infrastructure and custom silicon. Recent financial reports have highlighted exceptional growth, including a twenty-nine percent year-over-year surge in licensing revenues. This growth is largely fueled by escalating demand for advanced chip designs and custom processors. Additionally, royalty revenues rose eleven percent, driven by accelerated adoption of the Armv9 architecture and wider penetration of its Compute Subsystems in next-generation data centers. This steady transition from mobile-centric IP to high-performance AI data center architecture has bolstered institutional confidence.

Sustained institutional interest has provided further support for the stock. Recent regulatory filings revealed new position initiations and increased holdings by several institutional investors, demonstrating long-term confidence from professional money managers even amid broader sector volatility. This influx of institutional capital has acted as a stabilizer, helping the stock rebound from its recent corrective phase.

Broader market and industry dynamics also contributed to the upward pressure. Following a mid-year correction in tech and semiconductor equities, investors have aggressively rotated capital back into premium AI-related names. Arm's strategic partnerships with major hyperscalers and cloud giants have solidified its position as a default architecture for emerging agentic AI workloads. This thematic strength, paired with anticipatory buying ahead of the company's upcoming quarterly earnings release later in the month, created a highly favorable environment for the daily surge.

Despite the positive move, the stock continues to experience intraday volatility due to mixed technical indicators and valuation concerns. While the underlying fundamentals remain exceptionally strong, high forward valuation multiples and recent insider selling have introduced a level of caution. This tension between near-term technical resistance and robust long-term growth prospects explains the sharp price swings observed during the trading session.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of -26.705, indicating a neutral signal. The RSI at 42.426 suggests neutral condition and the Williams %R at 93.966 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $284.35, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- Severe Capacity and Supply Bottlenecks: Despite securing over $20 billion in customer demand within six weeks for its newly launched Arm AGI CPU, management has disclosed that the company has only successfully locked in manufacturing capacity to fulfill $1 billion of that total demand.

- Valuation Multiples Severely Decoupled from Fundamentals: Trading at an exceptionally elevated trailing P/E ratio exceeding 380x and a forward Price-to-Sales ratio of 49.1x (compared to the semiconductor industry average of 9.1x), the stock is highly vulnerable to aggressive mean reversion and downside volatility on even slight macro or sector sentiment shifts.

- Overhang from Impending Legal and Regulatory Battles: Mid-term execution is heavily clouded by high-stakes legal risks, specifically the critical Qualcomm/Nuvia trial scheduled for late 2026, alongside an ongoing FTC antitrust investigation.

- Operating Margin Compression and Rising R&D Drag: The aggressive transition into designing custom silicon has forced non-GAAP operating margins down from 52.8% to 49.1%, driven by a 43% year-over-year surge in necessary R&D expenses ($1.91 billion) that reduces near-term profitability.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.