Intel Corp Stock (INTC) Moved Up by 4.92% on Jul 9: What Signal Does It Send?

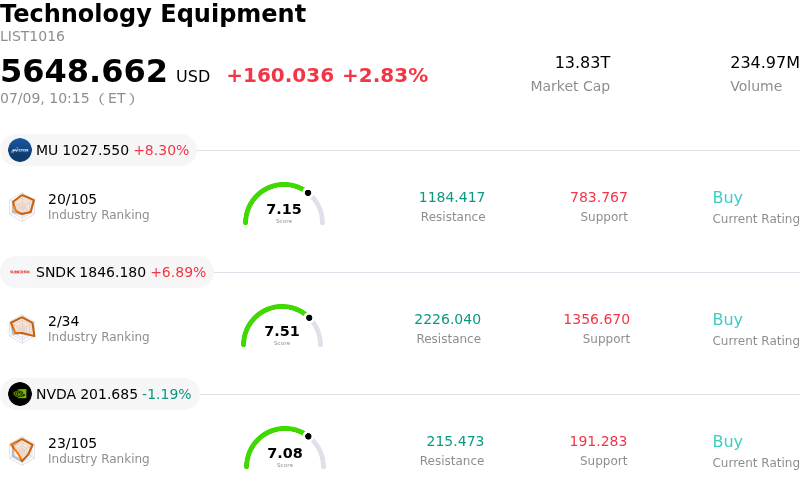

Intel Corp (INTC) moved up by 4.92%. The Technology Equipment sector is up by 2.83%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 8.87%; SanDisk Corporation (SNDK) up 7.12%; NVIDIA Corp (NVDA) down 1.19%.

What is driving Intel Corp (INTC)’s stock price up today?

Intel shares advanced significantly on Thursday, staging a notable intraday reversal. This rally was primarily fueled by a broad-based recovery across the semiconductor sector following a period of intense selling pressure earlier in the week.

The primary catalyst for the positive shift in market sentiment was a highly influential call from prominent Wall Street strategists, who framed the recent semiconductor selloff as an attractive buying opportunity. Analysts argued that the structural bull case for owning chip and memory companies remains entirely intact and that the technical indicators signaled the downward momentum was reaching its exhaustion point. This analytical reassurance provided institutional and retail dip-buyers with the confidence to step back into leading chipmakers, including Intel.

This constructive view was further reinforced by robust quarterly results and strong financial performances reported by global peers in the semiconductor and memory spaces. Phenomenal operating profits from major international memory manufacturers highlighted that global demand for artificial intelligence infrastructure and advanced chips remains exceptionally strong, proving that the previous days’ selloff was driven more by short-term profit-taking rather than any fundamental deterioration in the industry.

For Intel specifically, the rebound follows a sharp retreat earlier in July, which had been triggered by sector-wide valuation concerns and reports that the company’s crucial 18A manufacturing process might not reach profitable production yields until late 2026 or 2027. Despite these lingering medium-term foundry concerns, the market has shifted its focus back to Intel's near-term drivers. Investors are increasingly optimistic ahead of the company's upcoming second-quarter earnings release scheduled for July 23.

Expectations are growing that Intel could deliver a stronger-than-expected quarterly report due to robust demand for server CPUs in AI data centers and a favorable pricing environment. Secular tailwinds, including Intel’s Xeon 6 processors being selected for high-profile AI server architectures and a growing partnership with major hyperscalers, continue to support the long-term investment thesis, prompting buyers to aggressively accumulate shares during this volatile session.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of -6.215, indicating a neutral signal. The RSI at 43.249 suggests neutral condition and the Williams %R at 84.634 suggests oversold condition. Please monitor closely.

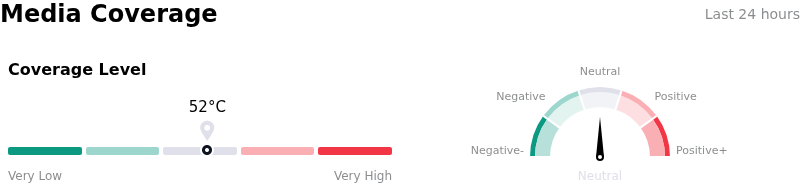

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 52, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $97.33, a high of $200.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Delays in Intel 18A Node Profitability: Reports indicating that Intel's advanced 18A manufacturing process may not achieve profitable yields until late 2026 or 2027 have dampened expectations for a rapid, high-margin turnaround in its foundry business.

- Severe Foundry Segment Losses: The Intel Foundry division continues to generate heavy operating losses, drawing approximately $2.4 billion in losses last quarter against only $174 million in external contract client revenue, which pressures overall margins amid massive ongoing capital investment.

- Market Share Loss to Key Competitors: Advanced Micro Devices (AMD) has surpassed Intel in quarterly data center revenue for the first time in modern history, highlighting Intel's vulnerability to market share erosion in the highly profitable server-CPU landscape.

- Multiple Compression on Stretched Valuation: Following a massive year-to-date rally, the stock is experiencing high volatility as analysts warn that its valuation multiples are extended, leaving the company vulnerable to severe downside if upcoming earnings miss expectations.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.