American Express Co Stock (AXP) Moved Up by 3.15% on Jul 1: What Signal Does It Send?

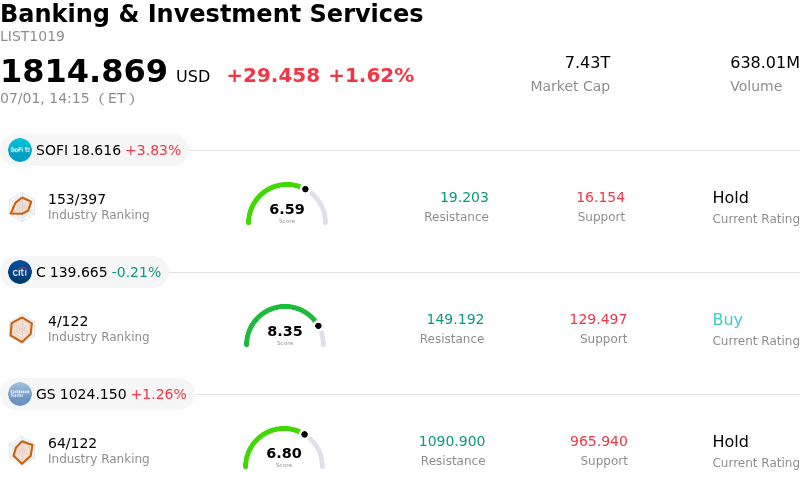

American Express Co (AXP) moved up by 3.15%. The Banking & Investment Services sector is up by 1.62%. The company outperformed the industry. Top 3 stocks by turnover in the sector: SoFi Technologies Inc (SOFI) up 3.83%; Citigroup Inc (C) down 0.21%; Goldman Sachs Group Inc (GS) up 1.26%.

What is driving American Express Co (AXP)’s stock price up today?

American Express (AXP) experienced notable upward momentum accompanied by significant intraday volatility, driven by a combination of positive analyst actions, strong regulatory stress test outcomes, and resilient consumer spending indicators.

A primary catalyst for the stock's upward trajectory is recent favorable analyst coverage. Piper Sandler initiated coverage on the credit card giant with an Overweight rating and an ambitious price target of $396.00. This bullish assessment reflects deep institutional confidence in the financial services company’s ability to outperform its peers. While some research firms like BTIG have maintained a more cautious Sell rating due to concerns over the pace of its commercial product refreshes and intensifying competition from fintech players, the dominant market narrative remains highly supportive. This support is further reinforced by earlier upgrades from DZ Bank and price target increases from major institutions like Bank of America.

Fundamentally, American Express continues to benefit from its affluent consumer base and robust credit metrics. Management recently highlighted that second-quarter billing activity has been tracking ahead of first-quarter growth, signaling that inflation and high interest rates have not severely dented premium consumer spending. Furthermore, credit quality has remained remarkably stable, with low delinquency rates and manageable charge-offs, which have helped mitigate broader macroeconomic anxieties.

Additionally, the company successfully cleared the 2026 Dodd-Frank Act stress tests, confirming it will maintain its stress capital buffer at the regulatory minimum of 2.5% through 2027. This clean bill of health underscores the strength of the company’s balance sheet and reassures investors of its capacity to continue robust capital return programs, including stock buybacks and consistent dividend payments. Despite some intraday volatility stemming from sector-wide adjustments and broader macroeconomic fluctuations, these strong fundamentals and bullish sell-side ratings have ultimately propelled the stock higher.

Technical Analysis of American Express Co (AXP)

Technically, American Express Co (AXP) shows a MACD (12,26,9) value of 1.750, indicating a buy signal. The RSI at 62.046 suggests neutral condition and the Williams %R at 33.279 suggests buy condition. Please monitor closely.

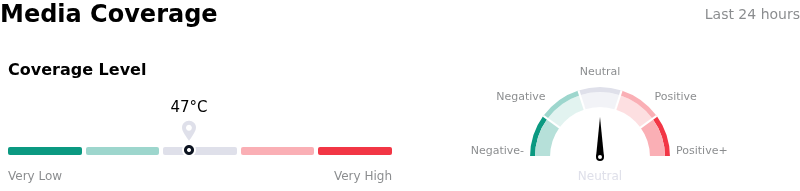

Media Coverage of American Express Co (AXP)

In terms of media coverage, American Express Co (AXP) shows a coverage score of 47, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of American Express Co (AXP)

American Express Co (AXP) is in the Banking & Investment Services industry. Its latest annual revenue is $56.12B, ranking 6 in the industry. The net profit is $10.70B, ranking 10 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $364.94, a high of $450.00, and a low of $272.91.

More details about American Express Co (AXP)

Company Specific Risks:

- Elevated Operating Expenses from Premium Card Reinvestments: Rapidly expanding membership perks—such as the recent integrations with Apple Pay and Fanatics, alongside ongoing product refreshes like the Platinum and Gold cards—continue to push cardmember acquisition and marketing expenses higher, threatening to squeeze near-term margins and overshadow solid top-line performance.

- Valuation Premium Limits Upside Potential: Trading at approximately 19x earnings, the stock commands a clear premium over its sector peers. This rich valuation has already priced in much of the company's growth, leaving the stock highly sensitive to any marginal slowdown in spending and prompting cautious "Sell" or "Hold" ratings from notable institutional research firms.

- Small Business Credit Exposure: While consumer credit metrics remain relatively stable, the small business segment continues to exhibit higher net write-off and delinquency rates compared to the consumer division, posing an ongoing credit quality risk if macroeconomic conditions soften.

- Disruptive Fintech and AI Payment Disintermediation: Long-term competitive risks persist as advancements in agentic artificial intelligence and digital checkout platforms threaten to disintermediate traditional credit card networks, sparking structural concerns regarding the future growth of transaction fee volumes.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.