Merck & Co Inc Stock (MRK) Moved Up by 4.04% on Jun 25: A Full Analysis

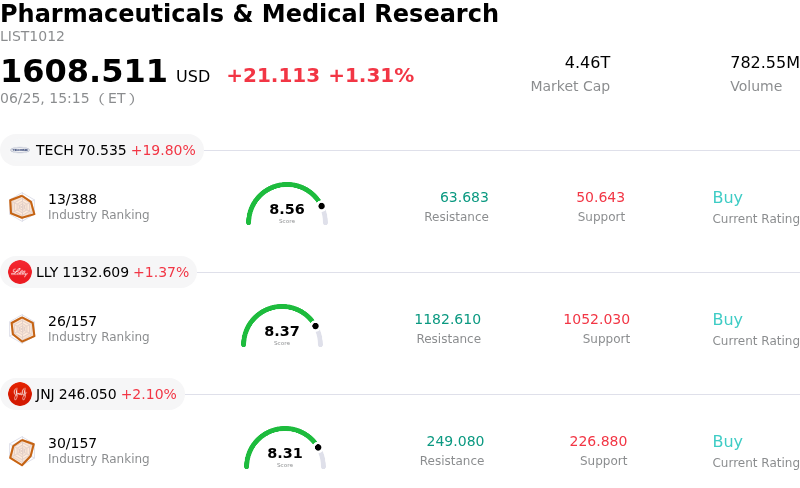

Merck & Co Inc (MRK) moved up by 4.04%. The Pharmaceuticals & Medical Research sector is up by 1.31%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Bio-Techne Corp (TECH) up 19.80%; Eli Lilly and Co (LLY) up 1.37%; Johnson & Johnson (JNJ) up 2.10%.

What is driving Merck & Co Inc (MRK)’s stock price up today?

The primary catalyst for the stock's strong upward movement today is a major regulatory victory. The U.S. Food and Drug Administration (FDA) approved Keytruda and Keytruda Qlex, in combination with Gilead Sciences' antibody-drug conjugate Trodelvy, for the first-line treatment of adult patients with advanced or metastatic triple-negative breast cancer (TNBC) whose tumors express PD-L1. This landmark decision marks the first time a PD-1 inhibitor has been approved in combination with a Trop-2-directed antibody-drug conjugate for this aggressive and hard-to-treat cancer. Given that Keytruda is the cornerstone of the company’s oncology franchise, this expanded indication significantly boosts its long-term revenue pipeline and reinforces its market-leading position in immuno-oncology.

This oncology breakthrough follows hot on the heels of another significant regulatory milestone. Just last week, the FDA granted an expanded indication for the company’s pneumococcal conjugate vaccine, Capvaxive. The approval extends its use to high-risk children and adolescents aged 2 through 17 with chronic medical conditions, making it the first and only vaccine of its kind specifically indicated and studied for this pediatric group in the United States. Together, these consecutive FDA clearances highlight the exceptional execution of the firm's clinical pipeline and validate its diversified growth strategy across both oncology and vaccines.

Further amplifying investor enthusiasm, Wall Street sentiment has grown increasingly bullish. Investment bank CICC recently initiated coverage on the company with an Outperform rating and a favorable price target, citing its strong dividend reliability and updated full-year guidance. During its latest earnings update, management raised both its revenue and earnings-per-share projections for 2026, underlining the company’s operational efficiency and robust commercial execution. This positive forward guidance, paired with the broader resilience and strategic M&A activity within the healthcare sector, has fueled robust institutional accumulation. Collectively, these factors have propelled the pharmaceutical giant to a new 52-week high, establishing strong bullish momentum and driving the notable intraday gains.

Technical Analysis of Merck & Co Inc (MRK)

Technically, Merck & Co Inc (MRK) shows a MACD (12,26,9) value of -0.017, indicating a neutral signal. The RSI at 58.032 suggests neutral condition and the Williams %R at 24.054 suggests buy condition. Please monitor closely.

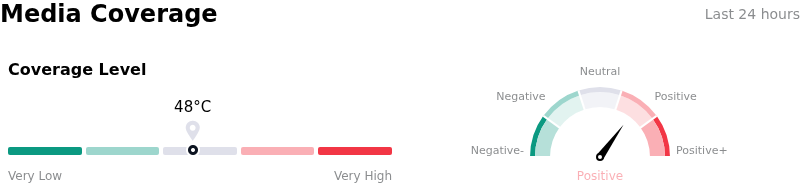

Media Coverage of Merck & Co Inc (MRK)

In terms of media coverage, Merck & Co Inc (MRK) shows a coverage score of 48, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Merck & Co Inc (MRK)

Merck & Co Inc (MRK) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $65.01B, ranking 5 in the industry. The net profit is $18.25B, ranking 3 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $129.82, a high of $150.00, and a low of $100.00.

More details about Merck & Co Inc (MRK)

Company Specific Risks:

- Keytruda Patent Cliff Overhang: Institutional analyst reports from June 25, 2026, emphasize the massive risk associated with Keytruda's upcoming 2028 core patent expiration. Because Keytruda generates nearly half of Merck's total pharmaceutical revenues, there is deep concern over the company's ability to offset an estimated $25 billion in annual revenue erosion once biosimilar competition enters the market.

- Gardasil Demand Softness in China: Analyst updates from the last 48 hours highlight structural risks to Merck's second-biggest franchise, Gardasil. Following an extended freeze on shipments to China and the abandonment of the $11 billion 2030 sales target, the prolonged slump in Chinese consumer spending on vaccines continues to act as a significant drag on near-term growth.

- Recent Pipeline Discontinuations and Phase 3 Setbacks: Merck's strategy to bridge the post-Keytruda revenue gap has been weakened by critical clinical failures. These include the June 8, 2026, discontinuation of the Phase 3 KEYNOTE-D46/EVOKE-03 combination trial in lung cancer, and the Phase 3 Litespark-012 flop for Welireg, which took a $5.8 billion "upside case" peak revenue scenario for kidney cancer treatments off the table.

- Acquisition Charges and Conservative 2026 Outlook: Significant cash outlays and one-time charges from aggressive deal-making—including a $5.8 billion (or $2.35 per share) research and development charge for the Terns acquisition and Cidara-related fees—have weighed heavily on GAAP earnings. This has kept Merck's full-year 2026 guidance conservative (EPS of $5.04 to $5.16), missing higher Street expectations and prompting institutional investors to take a cautious approach.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.