KLA Corp Stock (KLAC) Closed Up by 3.52% on Jun 22: A Full Analysis

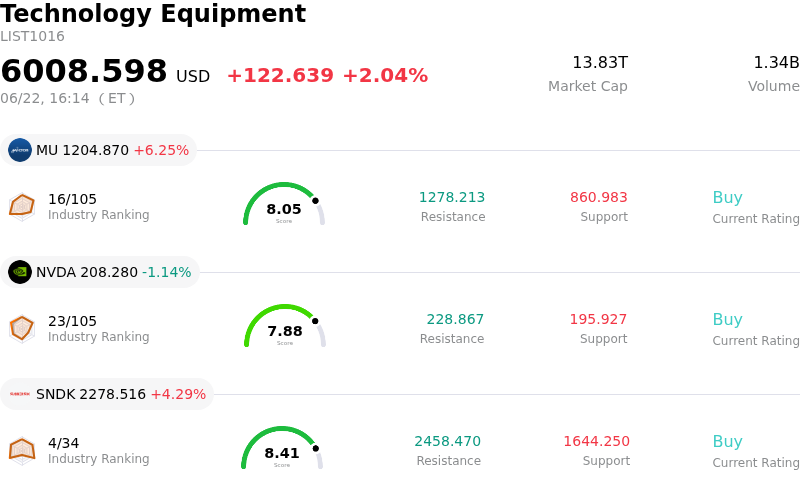

KLA Corp (KLAC) closed up by 3.52%. The Technology Equipment sector is up by 2.04%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 6.25%; NVIDIA Corp (NVDA) down 1.14%; SanDisk Corporation (SNDK) up 4.29%.

What is driving KLA Corp (KLAC)’s stock price up today?

The upward movement and notable intraday volatility in KLA Corporation’s stock are primarily driven by the market digesting its recent ten-for-one forward stock split, which went into effect earlier this month. The split has significantly enhanced share liquidity and accessibility for a broader base of retail and institutional investors. Following a period of profit-taking and defensive options positioning right after the split, the stock has found solid footing, attracting buyers eager to capitalize on the lower nominal entry point and the company’s massive structural growth narrative.

The underlying fundamental driver remains KLA’s undisputed dominance in the semiconductor process control and inspection equipment market. As artificial intelligence applications, high-bandwidth memory, and advanced packaging demand continue to scale, the complexity of chip manufacturing has risen exponentially. This complexity makes defect inspection critical to yield optimization. KLA recently raised its 2026 outlook for advanced packaging process control revenue to approximately one billion dollars, a significant increase from previous years, highlighting how the company is directly capturing value from the ongoing artificial intelligence infrastructure boom.

Positive analyst sentiment and recent target price revisions have further fueled the upward momentum. Major investment firms have aggressively raised their price targets, pointing to KLA’s expanding process control market share, which is several times larger than its nearest competitor. Analysts emphasize that the company’s high-margin services business, supported by longer tool lifecycles and stable recurring revenue, insulates it from some of the broader semiconductor industry’s traditional cyclicality.

While the stock continues to navigate headwinds like stringent government export controls on shipments to China and elevated valuation multiples, today's positive price movement reflects strong buy-the-dip sentiment. Investors are increasingly viewing KLA as an indispensable choke point in the global semiconductor supply chain, transforming short-term technical pullbacks into attractive buying opportunities as the industry enters an accelerating wafer fabrication investment cycle.

Technical Analysis of KLA Corp (KLAC)

Technically, KLA Corp (KLAC) shows a MACD (12,26,9) value of -402.481, indicating a sell signal. The RSI at 19.618 suggests oversold condition and the Williams %R at 98.132 suggests oversold condition. Please monitor closely.

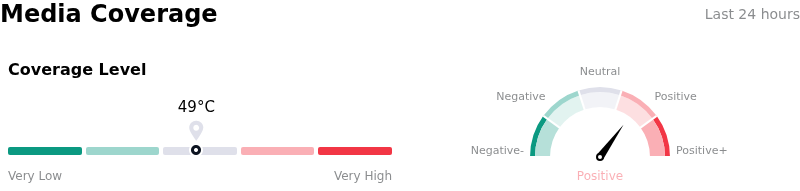

Media Coverage of KLA Corp (KLAC)

In terms of media coverage, KLA Corp (KLAC) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of KLA Corp (KLAC)

KLA Corp (KLAC) is in the Technology Equipment industry. Its latest annual revenue is $12.16B, ranking 15 in the industry. The net profit is $4.06B, ranking 11 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $196.47, a high of $290.00, and a low of $138.80.

More details about KLA Corp (KLAC)

Company Specific Risks:

- Extreme Valuation Multiples Post-Stock Split: Following the 10-for-1 stock split effective June 12, 2026, the company's trailing P/E multiple expanded to over 67x—significantly above its five-year median of 26x. This rich premium leaves no margin of safety, prompting profit-taking and driving a swift 7.44% pullback on June 16.

- Aggressive Insider Divestments: Recent SEC filings reveal notable insider selling, highlighted by CEO Richard Wallace liquidating approximately $10 million in stock (45,120 shares) alongside total quarterly insider sales reaching $19.7 million, signaling a lack of confidence in sustaining current valuation levels.

- Input Cost Pressures and Gross Margin Contraction: Management projects a negative impact of approximately 100 basis points on gross margins. This is driven by soaring memory component costs and tariff-related pressures that the company is currently unable to pass down to its customers.

- Geopolitical and China Export Restraints: Strict government export controls targeting semiconductor technology shipments to China are expected to drag heavily on KLA's top-line growth. This regulatory friction is projected to cost the company an estimated $300 million to $350 million in forfeited revenue for the year.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.