Credo Technology Group Holding Ltd Stock (CRDO) Closed Up by 9.02% on Jun 21: What Investors Need To Know

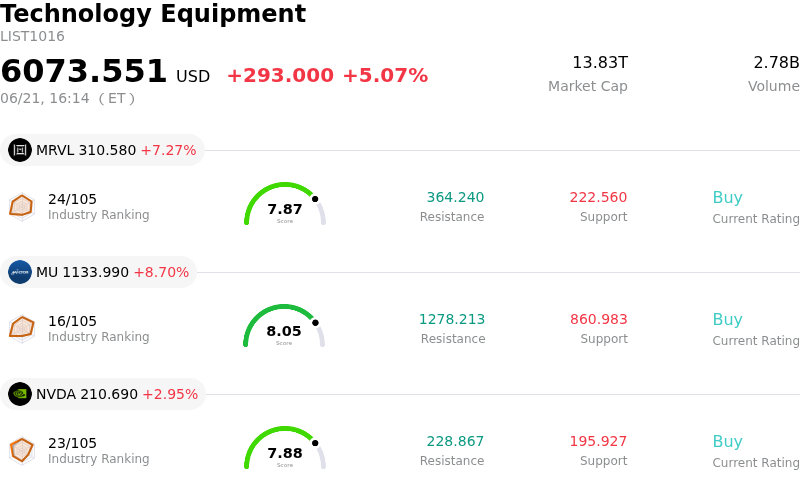

Credo Technology Group Holding Ltd (CRDO) closed up by 9.02%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Credo Technology Group Holding Ltd (CRDO)’s stock price up today?

The stock experienced significant upward momentum and notable intraday volatility, continuing a powerful rally driven by strong fundamental drivers and favorable sector-wide dynamics. This bullish price action is primarily underpinned by lingering positive sentiment from the company's exceptional fiscal fourth-quarter and full-year financial results, which confirmed a massive growth trajectory fueled by robust demand for high-speed artificial intelligence data center connectivity.

From a financial standpoint, the company's recent earnings release delivered an impressive revenue beat and a substantial earnings-per-share surprise compared to Wall Street consensus. More importantly, gross margins remained strong and comfortably above expectations, assuaging previous investor concerns regarding margin compression. Management's confident forward guidance for the upcoming fiscal quarter signaled continued sequential growth, highlighting that the company is successfully scaling its operations alongside the expanding artificial intelligence hardware cycle.

Strategically, the recent completion of the DustPhotonics acquisition has further bolstered investor enthusiasm. By integrating advanced silicon photonics, the company has established a vertically integrated optical stack capable of supporting next-generation bandwidth demands in hyperscale data centers. This strategic expansion, combined with the proven market adoption of its ZeroFlap Active Electrical Cables, solidifies its position as an indispensable hardware supplier for large-scale GPU cluster deployments where network reliability is paramount.

The upward movement was also accelerated by a wave of bullish analyst revisions, with major financial institutions raising their price targets to reflect the company's accelerated growth outlook. Although some analysts have pointed out potential risks, such as customer concentration and premium valuations, the overall market remains highly optimistic. Furthermore, a broad-based rally across the semiconductor and technology equipment sectors provided additional tailwinds, allowing the stock to outperform the broader market as institutional capital continues to flow into key artificial intelligence infrastructure enablers.

Technical Analysis of Credo Technology Group Holding Ltd (CRDO)

Technically, Credo Technology Group Holding Ltd (CRDO) shows a MACD (12,26,9) value of 3.590, indicating a buy signal. The RSI at 65.570 suggests neutral condition and the Williams %R at 4.099 suggests overbought condition. Please monitor closely.

Fundamental Analysis of Credo Technology Group Holding Ltd (CRDO)

Credo Technology Group Holding Ltd (CRDO) is in the Technology Equipment industry. Its latest annual revenue is $1.34B, ranking 39 in the industry. The net profit is $472.28M, ranking 24 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $262.09, a high of $300.00, and a low of $196.23.

More details about Credo Technology Group Holding Ltd (CRDO)

Company Specific Risks:

- **Severe Customer Concentration and Absence of Long-Term Contracts**: According to the company's newly filed FY2026 Form 10-K, Credo's top ten customers account for approximately 90% of total revenue, with the top two customers representing 61% of sales. Because the business operates without long-term purchase commitments, any order reduction, pause, or delay by a single key hyperscaler presents an immediate threat to revenue and margins.

- **Stretched Valuation and Plateauing Near-Term Growth**: Despite strong year-over-year numbers, near-term sequential revenue growth has slowed to just 7.4% in Q4 FY2026 and is guided to flatten in the first half of fiscal 2027. Because the highly anticipated $600 million optical product ramp is heavily back-half weighted to the latter half of FY2027, the stock's highly stretched valuation (trading around 18x forward EV-to-revenue and a high double-digit P/E multiple) is extremely vulnerable to severe multiple contraction.

- **High-Stakes Optical Pivot and Integration Risks**: Institutional analysts have flagged rising execution risks as Credo shifts its primary growth driver from established copper products—like its Active Electrical Cables (AECs)—toward more complex, unproven optical technologies. The integration of the newly acquired DustPhotonics and the commercialization of its vertically integrated silicon photonics stack represent major execution hurdles that could suffer from design-win delays or yield issues.

- **Geographic Supply Chain and Fluid Tariff Exposures**: Credo relies exclusively on TSMC for its wafer fabrication, alongside a concentrated group of Asian-based outsourced semiconductor assembly and test (OSAT) providers and cable manufacturers. This concentration exposes the company's operating margins to geopolitical tensions, supply chain disruptions, and a highly fluid global tariff regime.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.