Intel Corp Stock (INTC) Moved Up by 10.64% on Jun 20: What Investors Need To Know

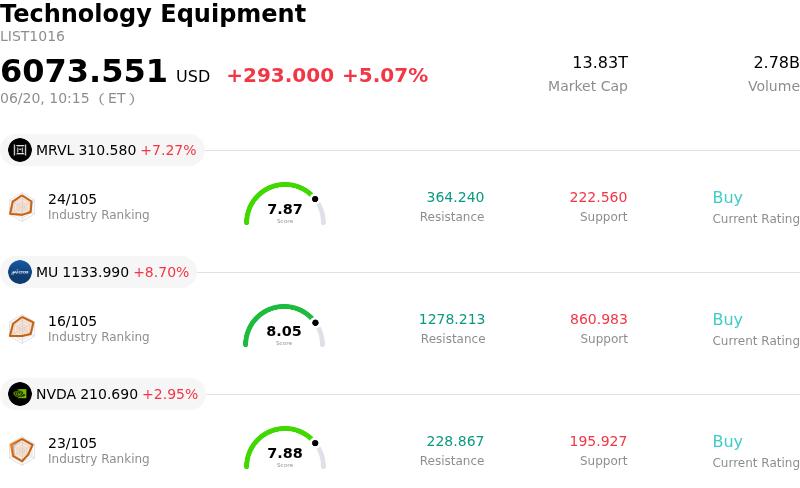

Intel Corp (INTC) moved up by 10.64%. The Technology Equipment sector is up by 5.07%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Marvell Technology Inc (MRVL) up 7.27%; Micron Technology Inc (MU) up 8.70%; NVIDIA Corp (NVDA) up 2.95%.

What is driving Intel Corp (INTC)’s stock price up today?

Intel has experienced significant upward momentum and heightened intraday volatility, driven primarily by a high-profile announcement regarding its contract manufacturing business. U.S. President Donald Trump shared on social media that Apple has agreed to partner with Intel to design and manufacture its chips domestically within the United States. Although neither Intel nor Apple has officially confirmed the agreement, the prospect of securing Apple as a foundry customer represents a watershed moment. Apple’s potential validation of Intel’s manufacturing capabilities signals to the broader tech industry that Intel’s fabrication facilities are becoming competitive with global leaders, marking a pivotal step in Intel's transition from a pure chip designer to a commercial foundry.

This speculative momentum is heavily supported by strong technical progress and government backing. Just days prior, Intel announced at the VLSI Symposium that its next-generation 18A-P process node had entered the risk production phase, delivering improved power efficiency and thermal characteristics. This milestone is complemented by tangible customer wins, notably a major contract from Google to manufacture over three million of its custom Tensor Processing Units (TPUs) starting in 2028. Furthermore, the U.S. government’s strategic roughly ten percent equity stake in Intel underscores Washington's commitment to reshoring advanced semiconductor manufacturing. This implicit state backing reduces execution risk and positions Intel as the primary beneficiary of national security-driven supply chain localization.

While the market has reacted with immense optimism, driving the broader semiconductor sector to record highs, institutional investors remain mindful of underlying risks. The foundry division remains deeply unprofitable, with a breakeven timeline not projected for another year, placing a heavy drain on capital reserves. Additionally, the rapid stock appreciation has stretched Intel's valuation relative to its current earnings, making the equity highly sensitive to changes in sentiment or any potential delays in the official confirmation of the Apple partnership. For now, the stock continues to trade on the immense promise of its dual-track strategy in AI infrastructure and advanced contract manufacturing.

Technical Analysis of Intel Corp (INTC)

Technically, Intel Corp (INTC) shows a MACD (12,26,9) value of 1.364, indicating a buy signal. The RSI at 64.208 suggests neutral condition and the Williams %R at 4.011 suggests overbought condition. Please monitor closely.

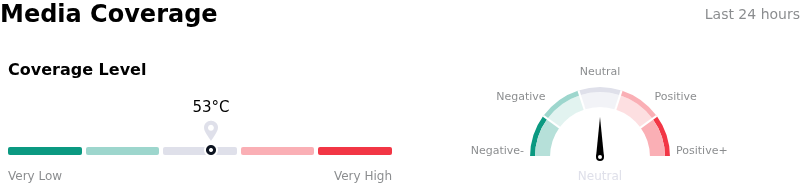

Media Coverage of Intel Corp (INTC)

In terms of media coverage, Intel Corp (INTC) shows a coverage score of 53, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Intel Corp (INTC)

Intel Corp (INTC) is in the Technology Equipment industry. Its latest annual revenue is $52.85B, ranking 4 in the industry. The net profit is $-267.00M, ranking 110 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $91.92, a high of $150.00, and a low of $25.00.

More details about Intel Corp (INTC)

Company Specific Risks:

- Speculative Volatility and Valuation Stretch from Unconfirmed Apple Rumors: Intel's recent run-up over $133, triggered by a June 18, 2026, social media post by President Donald Trump claiming a manufacturing partnership with Apple, remains highly speculative as neither company has officially confirmed the deal. Analysts warn this has stretched Intel's valuation to a precarious level with a minimal margin of safety, leaving the stock highly vulnerable to a sharp pullback and options-market hedging.

- Unprofitable Foundry Segment and Capital Drain: Intel's contract manufacturing (foundry) business remains deeply unprofitable, with a projected breakeven timeline delayed until 2027. Compounded by nearly $4 billion in negative free cash flow, the segment's heavy capital requirements severely strain Intel's reserves, while the company still faces steep execution hurdles in scaling ARM-based manufacturing for external clients since its 18A-P node has only just entered early risk production.

- Disruptive Competitive Threats to x86 Core Business: The launch of Nvidia’s RTX Spark processor in partnership with Microsoft represents a direct assault on Intel's core x86 PC and AI data center CPU businesses. By pushing to replace the legacy x86 architecture with alternative designs, this competitor directly threatens Intel’s long-term market share and primary cash-generating segments.

- Management Transition Risks in Critical Foundry Division: Following the June 18, 2026, announcement of Executive Vice President Navid Shahriari's retirement after 37 years, Intel is restructuring its advanced packaging leadership under Seok-Hee Lee. Executive turnover during a high-stakes, capital-intensive manufacturing turnaround introduces operational friction and execution risk to its commercial timelines.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.