Qualcomm Inc Stock (QCOM) Closed Up by 6.18% on Jun 11: What Signal Does It Send?

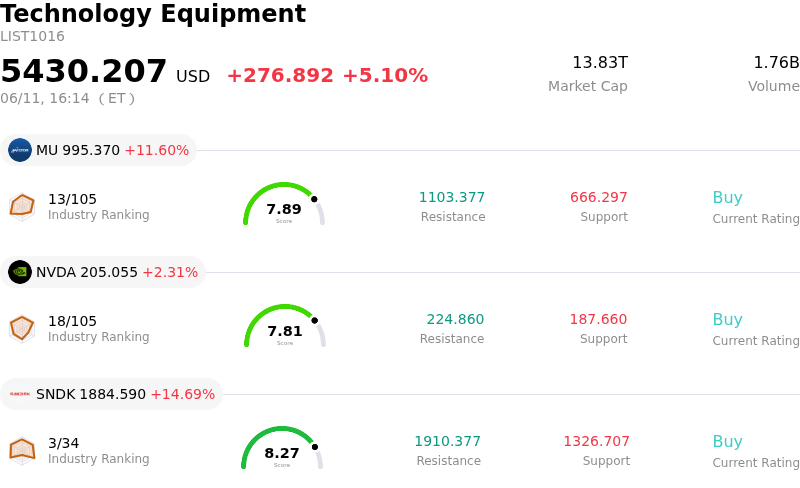

Qualcomm Inc (QCOM) closed up by 6.18%. The Technology Equipment sector is up by 5.10%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 11.60%; NVIDIA Corp (NVDA) up 2.31%; SanDisk Corporation (SNDK) up 14.69%.

What is driving Qualcomm Inc (QCOM)’s stock price up today?

Qualcomm (QCOM) experienced a significant upward movement in its share price, driven by a confluence of positive developments across its diversified business segments and a broader resurgence in the semiconductor sector.

A major catalyst for the positive sentiment was a public endorsement from Nvidia's CEO, Jensen Huang, who reportedly encouraged investors to acquire Qualcomm stock. Huang highlighted Qualcomm's strong positioning and success in mobile and AI-enabled smartphones, acknowledging its competitive advantages in edge devices, which differ from Nvidia's primary focus. This high-profile backing likely bolstered investor confidence in Qualcomm's long-term artificial intelligence strategy.

The company's automotive division also contributed significantly to the positive price action. Qualcomm announced that its Snapdragon Ride Flex SoC (Snapdragon 8775) had entered mass production and secured multiple design wins for vehicle models. Furthermore, the higher-performance Snapdragon 8797 is reportedly on the cusp of large-scale deployment. These advancements in "cockpit-driving integration" signify a strategic move to consolidate intelligent cockpit and advanced driver-assistance system functions onto a single chip, promising reduced hardware costs and improved efficiency. Qualcomm's automotive segment has demonstrated robust year-over-year growth, further supporting its expansion efforts in this high-growth market.

Beyond its traditional mobile and rapidly growing automotive sectors, Qualcomm's expansion into new AI and non-mobile markets, particularly data centers, has been well-received. The company has introduced "Dragonfly" as a brand for its data-center products, with more detailed disclosures anticipated at its upcoming Investor Day. This strategic diversification, including confirmed custom ASIC shipments for hyperscalers scheduled for calendar year 2026, underscores Qualcomm's commitment to capturing growth opportunities beyond its core smartphone business.

The positive trajectory was also supported by a general rebound across semiconductor stocks. After a recent market downturn, investors demonstrated renewed confidence in the sector, particularly in companies poised to benefit from artificial intelligence and data-center advancements. This broader market movement, coupled with Qualcomm's commitment to returning capital to shareholders through a substantial share repurchase plan and a dividend increase, further contributed to the upward price adjustment.

Technical Analysis of Qualcomm Inc (QCOM)

Technically, Qualcomm Inc (QCOM) shows a MACD (12,26,9) value of [15.49], indicating a neutral signal. The RSI at 43.31 suggests neutral condition and the Williams %R at -98.42 suggests oversold condition. Please monitor closely.

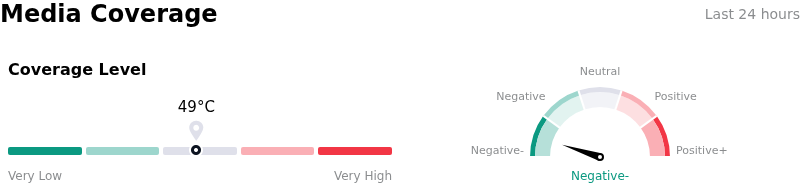

Media Coverage of Qualcomm Inc (QCOM)

In terms of media coverage, Qualcomm Inc (QCOM) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in extremely bearish zone.

Fundamental Analysis of Qualcomm Inc (QCOM)

Qualcomm Inc (QCOM) is in the Technology Equipment industry. Its latest annual revenue is $44.28B, ranking 5 in the industry. The net profit is $5.54B, ranking 7 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $178.09, a high of $300.00, and a low of $100.00.

More details about Qualcomm Inc (QCOM)

Company Specific Risks:

- Intensified competition in the Windows on Arm PC market from NVIDIA's newly unveiled RTX Spark chip, leveraging a more established software ecosystem, poses a significant threat to Qualcomm's Snapdragon X Elite in a crucial growth segment.

- Persistent erosion of core handset market share due to Apple's ongoing development of in-house modems and aggressive pricing from competitors like MediaTek, coupled with the structural risk of losing Apple's modem business by 2027.

- Significant geopolitical and regulatory vulnerabilities stemming from approximately 43% revenue concentration in China, exposing the company to US-China trade tensions and potential antitrust scrutiny by Chinese regulators, as well as investor apprehension following the ByteDance custom AI silicon deal.

- Negative shifts in analyst sentiment, including downgrades from JPMorgan to Neutral and Bernstein to Market Perform, citing increased competitive intensity in the datacenter market, near-term smartphone headwinds, and concerns over current valuation following a recent stock surge.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.