Lam Research Corp Stock (LRCX) Moved Up by 8.44% on Jun 8: What Signal Does It Send?

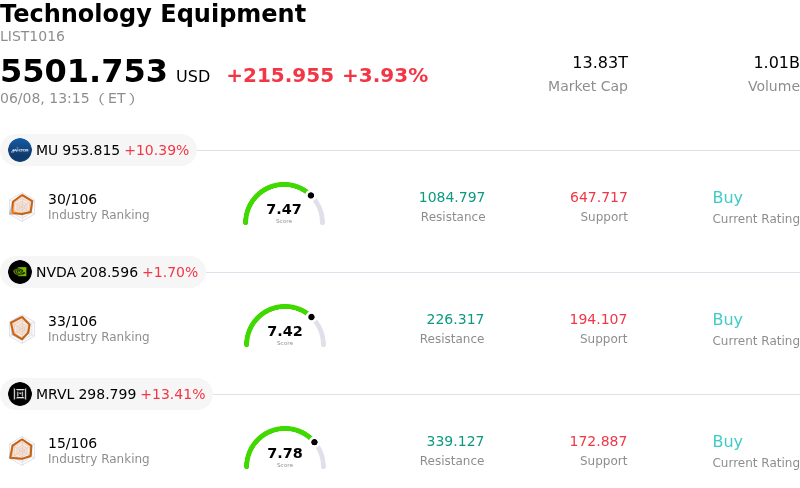

Lam Research Corp (LRCX) moved up by 8.44%. The Technology Equipment sector is up by 3.93%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) up 10.29%; NVIDIA Corp (NVDA) up 1.70%; Marvell Technology Inc (MRVL) up 13.35%.

What is driving Lam Research Corp (LRCX)’s stock price up today?

Lam Research (LRCX) experienced an upward share price movement today, primarily driven by a confluence of positive analyst sentiment, robust financial performance, and its integral role in the burgeoning artificial intelligence (AI) sector.

Recent analyst upgrades and increased price targets have significantly contributed to the positive momentum. Several prominent investment firms have revised their forecasts, with some raising price targets substantially and others upgrading their ratings. These adjustments largely stem from higher expectations for wafer fab equipment spending, specifically citing the expansion of AI logic and memory capacity. This wave of bullish analyst support reinforces investor confidence in the company's future prospects.

The company's strong financial foundation, as evidenced by its Q3 2026 earnings released in April, continues to underpin this positive outlook. Lam Research surpassed consensus estimates for both earnings per share and revenue, and importantly, provided optimistic guidance for Q4 2026 that exceeded analyst models. The company also raised its calendar year 2026 wafer fab equipment outlook, pointing to increased customer spending across various segments and strong demand driven by AI. Further highlighting its commitment to innovation, Lam Research recently announced a new research facility in Salzburg, Austria, dedicated to advanced panel-level packaging, a technology crucial for high-density, cost-effective AI applications.

Furthermore, the broader industry dynamics are highly favorable for semiconductor equipment providers like Lam Research. Recent reports from SEMI indicated a significant year-over-year increase in global semiconductor equipment billings for the first quarter of 2026, reaching record levels. This growth is directly attributed to sustained investments in AI-related infrastructure, including capacity expansion and technology upgrades for leading-edge logic, DRAM, and advanced packaging. Lam Research's position as a key supplier of critical etch and deposition tools for AI memory and advanced packaging was also underscored by recent industry discussions, cementing its role as an essential AI infrastructure provider. These company-specific and industry-wide tailwinds, coupled with a generally constructive market environment for technology stocks, have collectively fueled today's positive movement.

Technical Analysis of Lam Research Corp (LRCX)

Technically, Lam Research Corp (LRCX) shows a MACD (12,26,9) value of [15.45], indicating a buy signal. The RSI at 51.44 suggests neutral condition and the Williams %R at -52.02 suggests oversold condition. Please monitor closely.

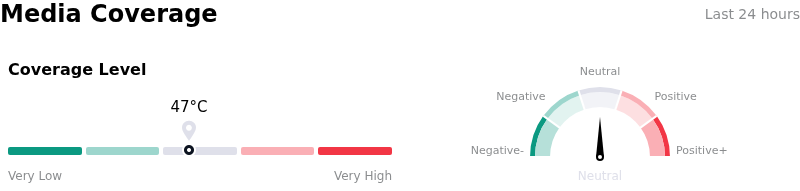

Media Coverage of Lam Research Corp (LRCX)

In terms of media coverage, Lam Research Corp (LRCX) shows a coverage score of 47, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Lam Research Corp (LRCX)

Lam Research Corp (LRCX) is in the Technology Equipment industry. Its latest annual revenue is $18.44B, ranking 12 in the industry. The net profit is $5.36B, ranking 8 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $315.89, a high of $385.00, and a low of $213.00.

More details about Lam Research Corp (LRCX)

Company Specific Risks:

- Ongoing U.S. restrictions on chip shipments to China introduce significant uncertainty regarding market access and future revenue streams for Lam Research in a key market.

- Erste Group downgraded Lam Research's stock to "hold" due to increased risks of declining gross and operating margins, with management forecasting a slight gross margin decline for the current quarter.

- Analyst commentary suggests the stock is currently overvalued, with a forward P/E ratio of 53x embedding overly optimistic assumptions about long-term wafer fab equipment spending, increasing susceptibility to price corrections.

- Broader semiconductor sector weakness, driven by disappointing earnings forecasts from major industry players like Broadcom, has negatively impacted investor confidence and reset expectations for hyperscaler AI chip spending, putting pressure on LRCX.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.