Arm Holdings PLC Stock (ARM) Moved Down by 7.04% on Jun 5: A Full Analysis

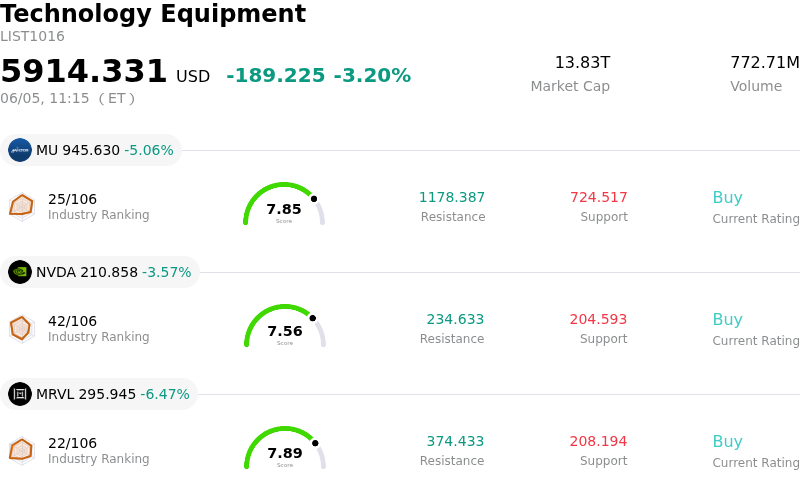

Arm Holdings PLC (ARM) moved down by 7.04%. The Technology Equipment sector is down by 3.20%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 4.82%; NVIDIA Corp (NVDA) down 3.57%; Marvell Technology Inc (MRVL) down 6.47%.

What is driving Arm Holdings PLC (ARM)’s stock price down today?

ARM Holdings PLC experienced significant downward pressure due to a combination of factors, primarily stemming from broader semiconductor industry concerns and specific company-related developments. A key catalyst for the negative movement was the disclosure of Broadcom's latest earnings report, which reportedly fell short of lofty expectations for AI chip revenue. This triggered a wave of selling across the semiconductor sector, leading to a general correction within the AI and chip space that impacted ARM and its peers.

Further contributing to the decline were reports of significant insider selling, with company executives, including the Chief Accounting Officer, reducing their holdings in late May and early June. Such actions can be interpreted by the market as a lack of confidence and prompt other investors to reassess their positions. Persistent concerns regarding ARM's elevated valuation also weighed on investor sentiment. Despite robust business fundamentals and strong growth prospects, the stock is considered significantly overvalued by various metrics, making it particularly vulnerable to negative catalysts and encouraging profit-taking.

Adding to the pressure, ARM's majority stakeholder, SoftBank Group, experienced a substantial drop in its own shares due to unease over its leveraged AI investment strategy. The close ties between the two entities mean that SoftBank's performance can significantly influence investor perception of ARM. Additionally, ongoing regulatory scrutiny from the U.S. Federal Trade Commission into ARM's licensing practices introduces an element of headline risk and uncertainty for the company.

While ARM has recently delivered positive news, including its CEO stating that the company is on track to exceed its $15 billion custom chip revenue target ahead of schedule due to strong AI demand, and analysts maintaining positive ratings and even raising price targets, these positive developments appear to have been overshadowed by the immediate impact of the broader sector pullback, insider activity, and valuation concerns. This confluence of factors led to the intraday volatility and a negative share price movement.

Technical Analysis of Arm Holdings PLC (ARM)

Technically, Arm Holdings PLC (ARM) shows a MACD (12,26,9) value of [41.48], indicating a buy signal. The RSI at 74.72 suggests buy condition and the Williams %R at -15.36 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Arm Holdings PLC (ARM)

Arm Holdings PLC (ARM) is in the Technology Equipment industry. Its latest annual revenue is $4.92B, ranking 23 in the industry. The net profit is $904.00M, ranking 17 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $248.53, a high of $500.00, and a low of $100.00.

More details about Arm Holdings PLC (ARM)

Company Specific Risks:

- The U.S. Federal Trade Commission has initiated an investigation into Arm Holdings' semiconductor licensing practices, examining whether the company uses its market position to impose restrictive terms on customers, which could lead to changes in contract structures and impact long-term royalty streams.

- ARM faces significant valuation concerns, with its stock trading at a forward price-to-sales ratio of 67.03x, substantially above the semiconductor industry average, and is considered overvalued by 134.7% according to its GF Value™, indicating potential for future multiple compression.

- The company's strategic shift into selling its own physical silicon (AGI CPU) introduces increased operational complexity, higher capital requirements, and risks alienating existing semiconductor partners, creating direct competition with its customer base and intensifying rivalry with established players like NVIDIA, AMD, and Intel.

- Arm is exposed to significant customer concentration risk, with over 57% of global revenue dependent on five major clients, and 16% of its FY26 revenue stemming from ARM China, an independently operated entity, posing challenges for financial transparency and intellectual property protection amid geopolitical tensions.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.