Boeing Co Stock (BA) Moved Down by 3.39% on Jun 2: Key Drivers Unveiled

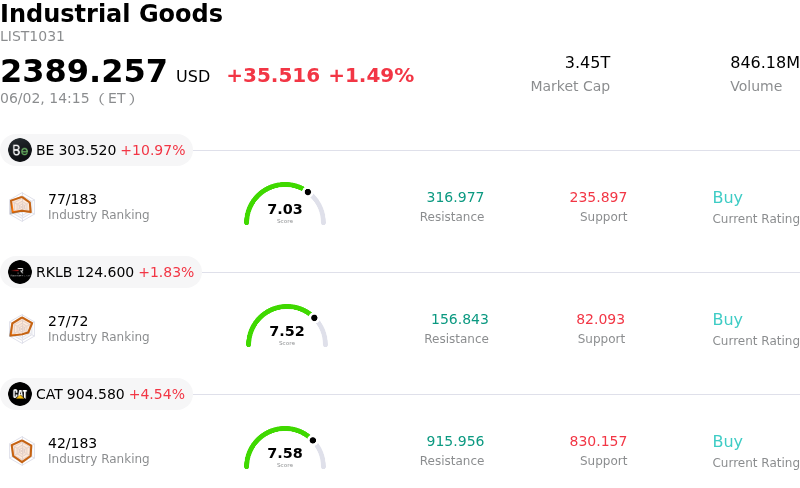

Boeing Co (BA) moved down by 3.39%. The Industrial Goods sector is up by 1.49%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Bloom Energy Corp (BE) up 10.98%; Rocket Lab USA Inc (RKLB) up 1.83%; Caterpillar Inc (CAT) up 4.54%.

What is driving Boeing Co (BA)’s stock price down today?

Boeing shares experienced a notable decline, reflecting investor concerns stemming from a confluence of operational challenges and new program delays. A primary factor contributing to this downward movement appears to be the continued production headwinds impacting the aerospace industry. Commercial aircraft manufacturing levels saw a decrease in May 2026, with both narrowbody and widebody production experiencing a pullback, interrupting an earlier upward trend. While Boeing's 737 MAX output is reportedly higher, single-aisle aircraft faced expanded lead times in May.

Further dampening sentiment is the persistent delay surrounding the certification of the 777X program. Recent indications suggest that the US certification for this key widebody aircraft is now likely to extend into 2027, a further postponement from previous targets. This extended timeline underscores ongoing complexities with new aircraft development and regulatory approvals, potentially affecting future delivery schedules and cash flow projections.

Despite the company's Q1 2026 earnings report showing a rise in consolidated revenue and an improvement in core loss per share, the operating margin declined, and there was a free cash flow outflow. While the free cash flow was better than anticipated and the company reiterated its positive free cash flow guidance for 2026, the market seems to be weighing the persistent operational hurdles, substantial debt, and the need to maintain cash for ongoing investments and the integration of Spirit AeroSystems. The ongoing regulatory scrutiny and production disruptions continue to be highlighted as headwinds for the stock.

While there are positive developments, such as the anticipation of 737 MAX 7 and MAX 10 certifications this summer and by year-end, and a strong order backlog approaching $700 billion, these positive aspects were seemingly overshadowed by the immediate concerns regarding manufacturing slowdowns and program delays. This mixed operational picture, particularly the latest certification setback for a major program and broader industry production dips, likely contributed to the stock's significant intraday volatility.

Technical Analysis of Boeing Co (BA)

Technically, Boeing Co (BA) shows a MACD (12,26,9) value of [0.43], indicating a neutral signal. The RSI at 49.45 suggests neutral condition and the Williams %R at -65.75 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Boeing Co (BA)

Boeing Co (BA) is in the Industrial Goods industry. Its latest annual revenue is $89.46B, ranking 1 in the industry. The net profit is $1.89B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $269.39, a high of $300.00, and a low of $233.00.

More details about Boeing Co (BA)

Company Specific Risks:

- Persistent manufacturing quality control issues continue to pose a risk, as an FAA audit earlier this year (prompted by a January incident) revealed multiple instances of non-compliance in Boeing's manufacturing process control, parts handling, and product control, necessitating an FAA-mandated action plan and continued oversight.

- The achievement of normalized free cash flow (around $6 billion) is not anticipated until 2027, with 2024 guidance significantly lower at $1-$3 billion, indicating a prolonged period before the company reaches stronger financial stability.

- Certification for critical new aircraft variants, such as the 777-9 and 737-7/10, are projected for first deliveries in 2027, meaning any further delays could impact future revenue streams and market confidence.

- Analyst commentary suggests that while operational recovery is underway, the current stock valuation largely reflects this optimism, leading to a "Hold" rating and potentially limited immediate upside, which could contribute to stock price sensitivity if recovery benchmarks are not met.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (1)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.