Why Is Dell Technologies (NYSE: DELL) Stock Falling? AI Server Growth Fails to Stop $70 Billion Selloff

AI Podcast

Dell Technologies faces a sectoral correction, with shares retreating 22% from record highs amid investor skepticism regarding AI infrastructure valuations and potential margin compression from rising memory costs. Despite robust fundamentals—including a 757% year-over-year surge in AI server revenue and a $51.3 billion backlog—heavy insider selling and a technical breach of trendline support have intensified bearish sentiment. While Wall Street analysts remain largely bullish on long-term prospects, the stock faces heightened sensitivity to future earnings guidance. Short-term price action remains vulnerable, with key support levels at $357 and $328 testing the market’s conviction in the AI hardware trade.

TradingKey -Dell Technologies (NYSE: DELL) shares are trading around $391 as they pull back over five per cent today and almost 22 per cent off their record highs reached earlier this month. In the last three trading sessions, the company has seen the market value decline by over $70 billion as investors pulled out of AI hardware stocks. The pressure has also fallen on Hewlett Packard Enterprise and Super Micro Computer.

What's fascinating is that the problem with slower demand is not driving the selloff. Dell's AI server business continues to see triple digit growth. Instead, investors are questioning whether AI infrastructure stocks ran too far, too fast.

Investors Worry About Margins, Not Demand

Dell's stock fell about 13% on Wednesday, extending losses over the next two sessions. The primary fear is that the profit margins on AI servers may be squeezed due to rising memory prices and growing competition for enterprise AI contracts.

Investors are increasingly skeptical, as memory prices appear to be peaking and dampening the supply shortage story driving up valuations for AI hardware so far this year, an Evercore ISI analyst said.

Particularly, the overall market didn't suffer from Dell's fall. The S&P 500, Nasdaq and Dow Jones Industrial Average were all up slightly, and Dell was down, indicating it's a sectoral pullback rather than a marketwide drop.

Insider Selling Added More Pressure

Investor sentiment was also affected by heavy insider selling. The regulatory filings indicated that there were approximately $1.56 billion in insider sales in the three months and no insider purchases during the same period. This week, two more Form 4 filings came out.

Among the sellers were Silver Lake affiliates and director Egon Durban, who together sold more than $320 million worth of shares.

While insider selling after a stock has gained more than 200% in the past year isn't unusual, the timing reinforced concerns already building around margins and encouraged traders to lock in profits.

Dell's AI Business Is Still Growing Rapidly

Despite the sharp pullback, Dell's core business remains strong.

The company reported:

- Revenue of $43.84 billion

- Earnings per share (excluding certain non-GAAP expenses) of $4.86

- AI server revenue surged 757% year over year to $16.1 billion

- The backlog for AI servers stood at $51.3 billion.

Management's guidance is that AI server revenue will be about $60 billion this fiscal year, close to double the previous guidance. Wells Fargo believes that figure could ultimately land between $60 billion and $65 billion.

Dell also secured a $9.7 billion, five-year Pentagon contract to manage Microsoft software and cloud licensing across U.S. military and intelligence agencies. The deal, which the DoD says will save approximately $422 million per year, marks Dell's latest involvement with major government and enterprise purchases outside of AI hardware.

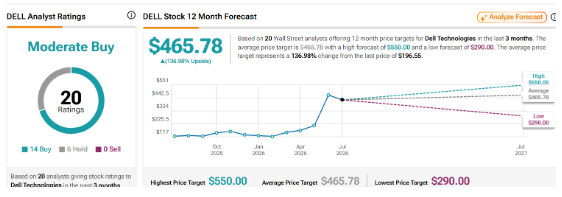

Wall Street Remains Largely Bullish

Even after this week's selloff, most analysts have maintained positive ratings on Dell.

Evercore ISI reiterated its Outperform rating and price target, stating that despite current concerns over the declining pricing of memory, the long-term opportunity for AI servers is intact.

Meanwhile, Goldman Sachs and Morgan Stanley have both increased their price targets for this year, from $467 and $474, respectively, earlier in the year.

However, not all are convinced of the lasting impact of the rally. Dell stock is currently priced at a level that doesn't provide much room for error, suggesting that even if the company's AI orders slow or its guidance is short of expectations at the next earnings call, it could spark another bout of selling, according to some analysts.

Image Source: TipRanks

Dell Stock Price Forecast: DELL Breaks Trendline Support as Bears Eye $357

Dell Technologies (NYSE: DELL) is trading bearish now that it has lost the bullish trend on the multi-week ascending trendline and the 50-period EMA near $419. The price has retreated to $379 and sellers continue to dominate after the rejection from the longer-term descending resistance trendline around $460.

Dollars $357, the 200-period EMA, is expected to provide support in the short term. Should the price fall below this support level, the next downside target would likely lie at $328. Resistance levels on the upside are expected to form at around $391, the trendline and $416, which is now resistance level as well.

Dell Stock Forecast Price Chart - Source: Tradingview

The momentum indicators, meanwhile, indicate bearish price action. The RSI has dropped to approximately 32 indicating strong selling momentum and oversold conditions and indicating that short-term relief rallies are possible. If the stock is unable to reclaim the $391 price level and the broken trendline, the long-term price action continues to point lower. The immediate focus will continue to be a series of lower support levels with rallies in the immediate future attracting sellers while trading below the 50 EMA.

What’s Next for Dell?

Dell’s next earnings, for fiscal Q2 2027, will be a major focus, and investors will be monitoring whether AI server backlog conversion rates improve and whether the demand trends remain robust as well as what revisions the company makes to its guidance for the fiscal year. Much of the reason behind Dell’s appreciation over the past year has been the optimism surrounding AI. As such, earnings could have a big impact on the stock going forward.

Dell is in an unusual place at the moment. While its business fundamentals are strong, the market sentiment has taken a very negative turn. In the coming weeks, we will see whether the selloff is a much-needed pullback after the impressive gains or the early signs of a more general rethink on the AI infrastructure trade.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.