Is SpaceX’s IPO Valuation Seriously Overvalued? Institution Cuts Its Valuation by 61% to $780 Billion.

AI Podcast

SpaceX's planned Nasdaq IPO on June 12 faces significant valuation concerns. Despite initial expectations nearing $2 trillion, recent reports suggest a target of $1.8 trillion. This revised valuation yields a price-to-sales ratio exceeding 90x, far above industry norms below 30x, indicating a fundamental mismatch. Morningstar values SpaceX at $780 billion, citing a "Narrow Moat" primarily due to its core rocket launch and satellite businesses. The nascent AI division, though valued at $170 billion, presents considerable uncertainty and risk of value destruction due to competitive pressures and immature technologies, impacting the overall moat rating.

TradingKey - SpaceX plans to list on Nasdaq on June 12, with less than two weeks remaining until the largest IPO in history goes public. Media reports suggest SpaceX could be included in the Nasdaq 100 as early as July, with a fundraising cap of $75 billion. Its market capitalization post-listing may exceed Tesla (TSLA). Bolstered by the hot sectors of AI and aerospace, SpaceX originally had high valuation expectations, but targets were lowered following the disclosure of its prospectus.

When SpaceX filed secretly for its IPO in early April, market valuations reached as high as $2 trillion. However, following the prospectus disclosure, latest reports indicate the current target valuation has been lowered to a starting point of $1.8 trillion, a $200 billion reduction compared to the $2 trillion previously reported by Bloomberg.

Although Elon Musk dismissed rumors regarding the valuation adjustment, the downward revision closely follows the prospectus disclosure cycle. The core factor is a severe mismatch between fundamentals and valuation.

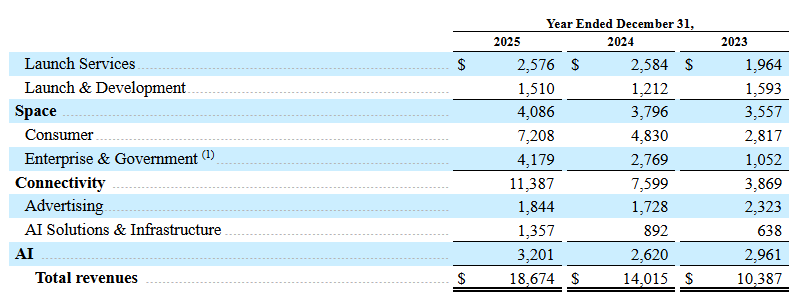

Assessing valuation from a fundamental perspective, financial data shows the company’s total revenue for 2025 is projected at just $18.67 billion. At a $2 trillion market cap, its price-to-sales (P/S) ratio would exceed 100x. Even at the revised $1.8 trillion valuation, the P/S ratio remains over 90x.

Benchmarking against the valuation centers of leading global tech companies, sustainable and reasonable P/S ratios for the industry are generally capped at 30x. Based on historical valuation logic, there is still room for a $1.25 trillion correction to digest the valuation.

A recent Morningstar research report on SpaceX echoes this view, valuing the largest IPO company in history at $780 billion—a 61% decrease from the $2 trillion valuation and a 56% decrease from the $1.8 trillion mark.

The firm stated that by leveraging continuous R&D investment and accelerating scale effects to create a significant cost advantage, the company's two core businesses—rocket launches and satellite communications—have built competitive barriers. It assigned the company a "Narrow Moat" rating.

The firm further noted that the outlook for the company's newly launched AI business is highly uncertain, making it impossible to determine if it can form a moat. Furthermore, the AI business carries significant risk of value destruction, which drags SpaceX’s overall economic moat rating down to "Narrow." Even after applying multiple probability-weighted scenarios for the AI business in its valuation, Morningstar’s discounted cash flow (DCF) model maintains SpaceX's fair value at $780 billion.

The firm stated that the $780 billion valuation is primarily divided into two parts: the core space launch and Starlink satellite connectivity businesses are estimated to be worth approximately $611 billion combined, while the AI division is valued at $170 billion.

Analysts at the firm pointed out significant risks in the AI business, noting that the Grok large language model under xAI lags behind leading AI developers. Additionally, long-term business implementation relies on immature technical solutions such as orbital data centers.

Constrained by intense competition from OpenAI and Anthropic, alongside questionable commercialization prospects, the AI business struggles to build a moat. This remains a key factor in SpaceX's overall moat being limited to a "Narrow" rating.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.