Kioxia Japan Shares Surge Over 660% Year-to-Date. Topping World’s Best-Performing Semiconductor Maker, Can Investors Still Buy Now?

Kioxia Holdings has achieved significant market capitalization growth since its December 2024 IPO, driven by a 660% year-to-date stock gain. Strong first-quarter 2026 revenue and record operating profit surges are attributed to explosive NAND demand from AI data centers and limited new supply. Goldman Sachs significantly raised its price target, citing future earnings projections and a favorable P/E ratio. However, market sentiment is divided, with analysts differing on the sustainability of Kioxia's performance. While the supply-demand gap and potential U.S. ADS listing offer upside, risks include NAND's cyclical nature and potential AI spending slowdowns.

TradingKey - Since its Tokyo listing in December 2024, Kioxia Holdings has completed the leap from IPO to one of Japan's top three companies by market capitalization in just a year and a half. As of the Asian trading session on June 3, Kioxia's Japan-listed shares saw a year-to-date increase of up to 660%, topping the leaderboard for annual gains among global semiconductor manufacturers.

Earlier, during the Asian session on June 1, Kioxia's shares jumped as much as 11% after Goldman Sachs sharply raised its target price from 48,000 yen to 93,000 yen and upgraded its rating from 'Neutral' to 'Buy.' Its market cap quickly surged to approximately 39.7 trillion yen, bringing Toyota Motor within its sights.

The Logic Behind Surging Performance

From January to March 2026, Kioxia reported revenue of 1,002.9 billion yen, a 189% year-on-year surge, while operating profit skyrocketed 15-fold to 596.8 billion yen, marking a record quarterly high. The U.S. dollar-denominated average selling price of NAND flash doubled within a single quarter, while shipments fell by approximately 10% quarter-on-quarter.

Explosive demand for NAND from AI data centers is colliding with a supply side where new capacity will not come online until late 2027 at the earliest. This supply-demand gap is shifting pricing power entirely back to memory manufacturers.

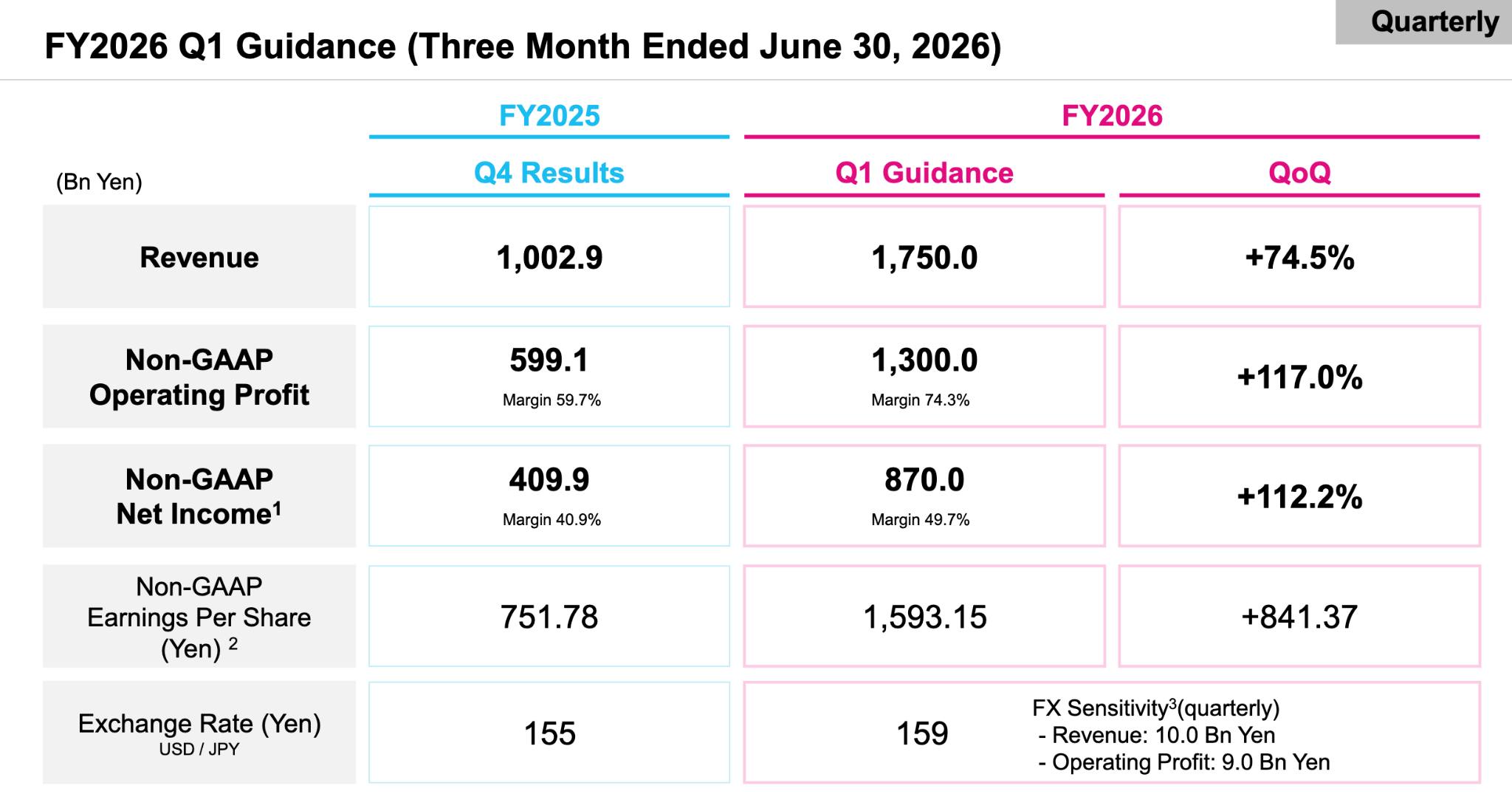

[Q1 FY2026 Guidance, Source: Kioxia FY2025 Financial Results Overview ]

Looking ahead to the April-June quarter, Kioxia's guidance is even more staggering: revenue is projected at 1.75 trillion yen, up 74.5% sequentially, and operating profit at 1.3 trillion yen, up 117% sequentially, yielding a 74% profit margin. This level of profitability is beginning to surpass that of software firms renowned for high gross margins.

The Core of Valuation Divergence

Based on 2027 earnings forecasts, its forward P/E ratio is only 7.9x, representing a roughly 20% discount to SK Hynix, making it appear quite cheap within the AI sector.

This is the core logic behind Goldman Sachs raising its price target to 93,000 yen; analysts forecast that Kioxia's consolidated operating profit will soar to the 10 trillion yen level in fiscal 2028, with gross margins consistently maintained around 80%. Based on these calculations, the PEG ratio is only 0.10x, suggesting that growth has seemingly not been priced in at all.

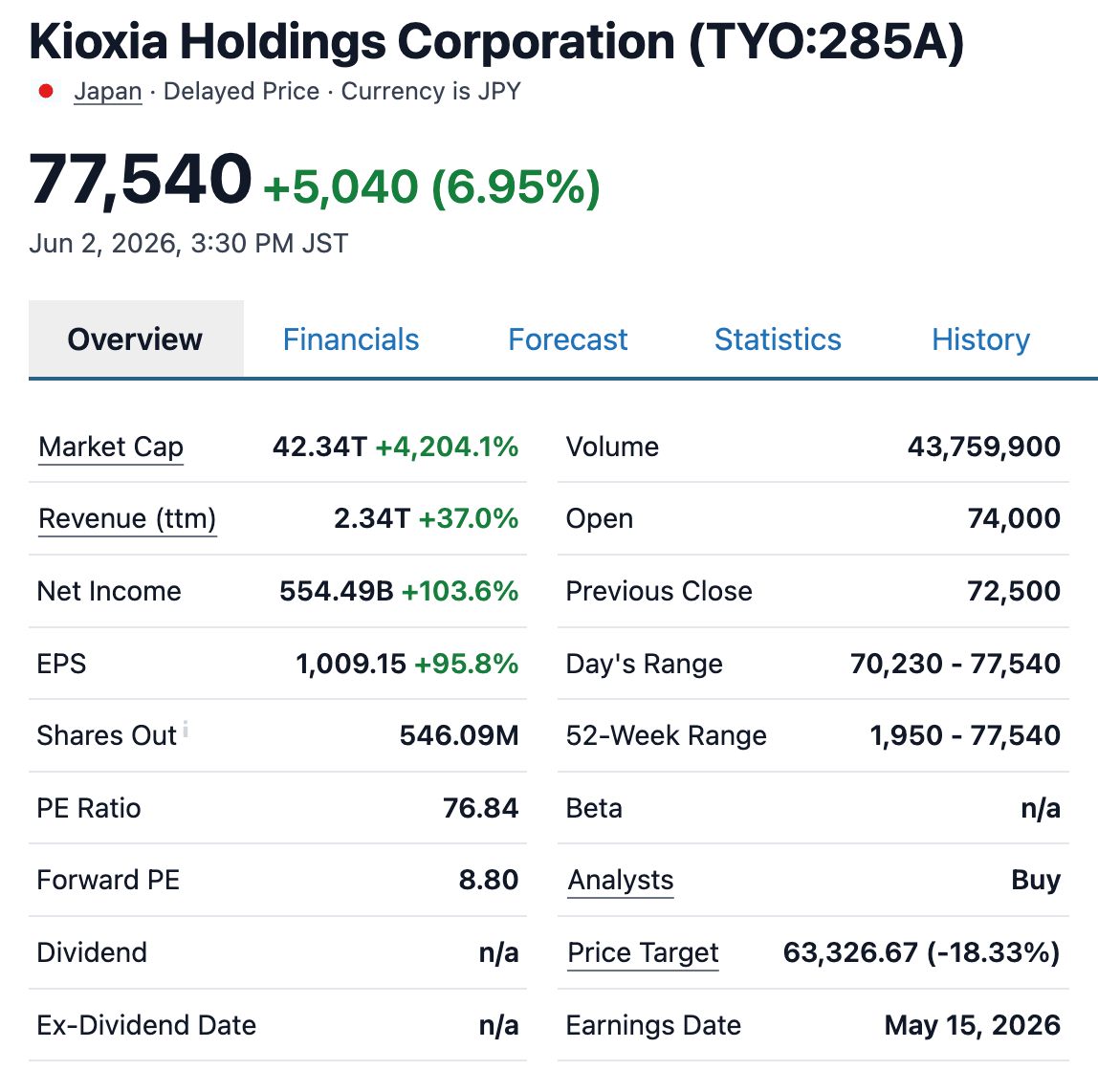

[Kioxia's 2026 forward P/E ratio is 8.8x, exceeding Samsung Electronics and SK Hynix; Source: Stockanalysis]

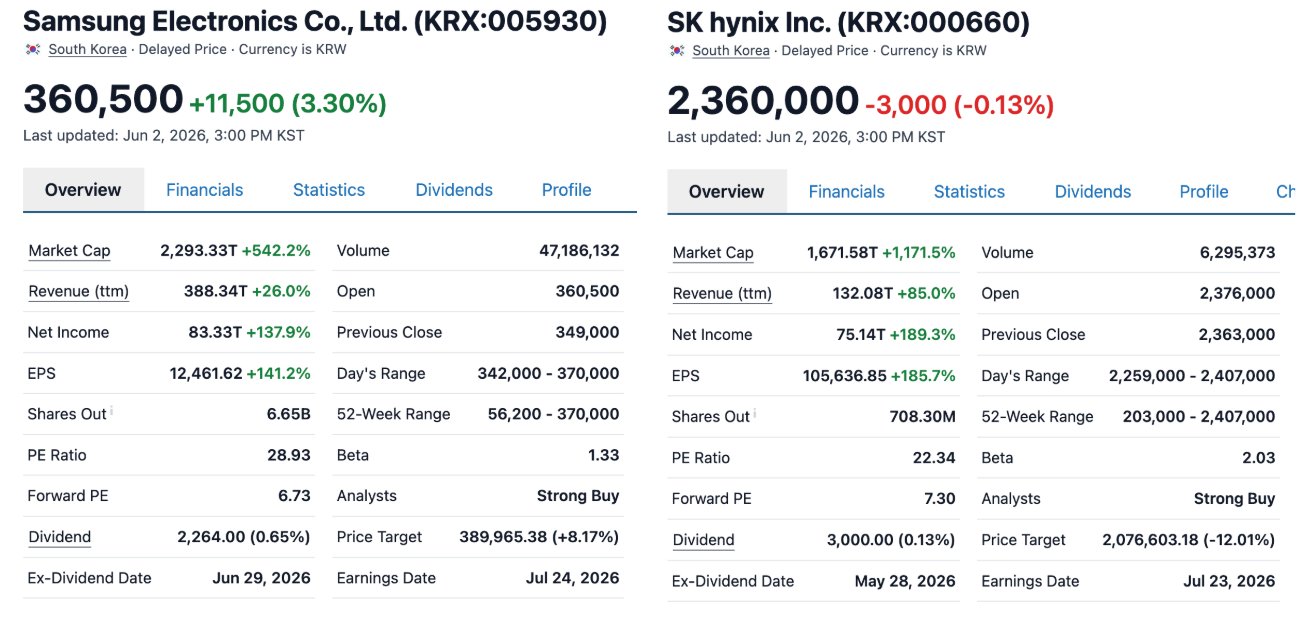

The current share price corresponds to a trailing P/E ratio of nearly 77x and a P/B ratio of 30.2x; its 2026 rolling P/E ratio of 8.8x remains higher than Samsung's 5.7x and SK Hynix's approximately 6x.

[Forward P/E for Samsung Electronics and SK Hynix; Source: Stockanalysis]

Market analysts are deeply divided over Kioxia. Among the 14 analysts who provided price targets, the most optimistic gave a target of 80,000 yen, while the most pessimistic cited only 17,000 yen, representing a gap of nearly fivefold. This extreme divergence implies that the market has yet to reach a consensus on the feasibility and sustainability of Kioxia's future earnings.

Upside potential and downside risk coexist.

The duration of the supply-demand gap is the primary source of upside elasticity. Previously, Kioxia management clearly stated that "the NAND market will remain very tight in both 2026 and 2027," with new capacity not expected to come online until late 2027 or even 2028 at the earliest. This suggests that the pricing environment continues to have support for sustained improvement in the short term.

Meanwhile, consistent with the logic applied to SK Hynix, Kioxia's secondary listing in the U.S. represents a structural catalyst for further valuation upside. Kioxia has announced plans for an ADS listing in the U.S. If successfully listed, the accessibility for international investors to allocate to the NAND sector will significantly improve, potentially driving its valuation framework closer to U.S.-listed peers such as Micron and SanDisk.

Investors should note that market bears believe NAND is a classic cyclical commodity, where the supply-demand gap could shift from "shortage" to "surplus" at any point—a risk repeatedly confirmed by historical experience. Massive AI orders have crowded out NAND capacity; if signals of marginal deceleration in AI capital expenditure emerge, current premiums could quickly dissipate.

Furthermore, some analysts believe the current quarterly operating profit target of approximately 1.3 trillion yen, equivalent to more than 5 trillion yen annualized, "is likely more than double Toyota’s peak profits," and whether this can be sustained in the short term still requires verification through earnings results.

Summary

From an optimistic standpoint, the supply-demand gap is expected to persist until at least 2028. A U.S. ADS listing is poised to widen the valuation premium, while guidance for a 74% operating margin and sustained 80% gross margins provides a solid foundation for high profitability.

Looking at positioning, there is minimal margin for error between the current price and the target price. For short-term investors, the current liquidity environment means that entry and exit costs have been systematically raised, resulting in an unfavorable risk-reward profile for new positions. For long-term investors, the accelerated upward revisions to earnings and the widening supply-demand gap continue to provide long-term support for core fundamentals.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.