Eli Lilly and Co Stock Opened Up by 3.36% on Feb 23: What Investors Need To Know

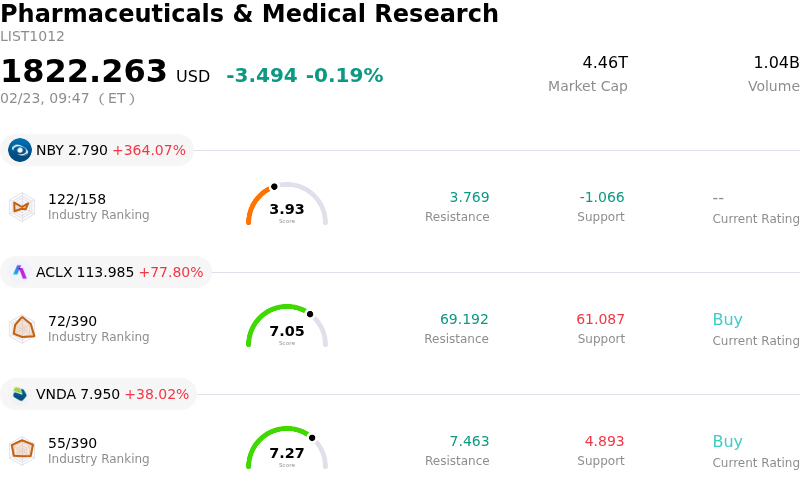

Eli Lilly and Co (LLY) opened up by 3.36%. The Pharmaceuticals & Medical Research industry is down by 0.19%. The company outperformed the industry. Top 3 gainers of the industry: NovaBay Pharmaceuticals Inc (NBY) up 364.07%; Arcellx Inc (ACLX) up 77.80%; Vanda Pharmaceuticals Inc (VNDA) up 38.02%.

Eli Lilly and Company's stock experienced significant intraday volatility and an upward movement on February 23, 2026, primarily driven by developments in the competitive landscape of the lucrative weight-loss drug market and a key product announcement.

A major catalyst for the positive movement was the news that rival Novo Nordisk's experimental obesity drug, CagriSema, failed to meet its primary endpoint in a clinical trial. The trial indicated that CagriSema did not achieve non-inferiority to Eli Lilly's Tirzepatide (marketed as Mounjaro and Zepbound) in terms of weight reduction, further solidifying Eli Lilly's leading position in this high-growth sector. This competitive setback for Novo Nordisk directly benefited market sentiment for Eli Lilly.

Adding to the positive momentum, Eli Lilly announced on the same day the FDA approval and immediate availability of a new multi-dose KwikPen for its popular weight-loss medication, Zepbound. This new pen delivers a month's supply of the drug and can be purchased by cash-paying customers through LillyDirect, the company's direct-to-customer website. This enhancement in product delivery and accessibility is expected to further boost sales and market penetration for Zepbound.

These immediate positive developments occurred against a backdrop of strong financial performance and bullish future outlook. Earlier in February, Eli Lilly reported robust fourth-quarter 2025 earnings, significantly exceeding revenue and earnings per share estimates. The company also provided optimistic financial guidance for fiscal year 2026, projecting substantial revenue and earnings growth, largely attributed to the continued success of its GLP-1 product portfolio. Analyst firms have consistently maintained or upgraded their ratings and raised price targets for Eli Lilly throughout February, reflecting strong confidence in the company's pipeline and market leadership. The company has also been actively engaged in legal actions to protect its intellectual property concerning its GLP-1 drugs from compounded versions, aiming to secure its market dominance.

Technically, Eli Lilly and Co (LLY) shows a MACD (12,26,9) value of [-5.48], indicating a sell signal. The RSI at 44.22 suggests neutral condition and the Williams %R at -86.76 suggests oversold condition. Please monitor closely.

Eli Lilly and Co (LLY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is 65.18B, ranking 4 in the industry. The net profit is 20.64B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as BUY, with an average price target of 1202.91, a high of 1500.00, and a low of 830.00.

Company Specific Risks:

- Eli Lilly faces significant financial risk due to over-reliance on its GLP-1 drugs, Mounjaro and Zepbound, which constituted 56% of its revenue in 2025, making the company vulnerable to market shifts or increased competition.

- Intensifying competition in the GLP-1 market, particularly from Novo Nordisk's oral GLP-1 pill which preceded Lilly's oral version, threatens Eli Lilly's market share and pricing power.

- The company's stock is perceived as having a high valuation (P/E of 44.2x versus peers at 19x), increasing susceptibility to profit-taking and potential sharp declines if growth or GLP-1 demand falls short of optimistic investor expectations.

- Rapid expansion of manufacturing capacity for GLP-1 products introduces execution risks, including potential for FDA scrutiny, production delays, and quality control issues, which are exacerbated by past regulatory observations at key facilities.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.