Meet the Newest Member of the $1 Trillion Stock Club

The $1 trillion valuation club is a fairly exclusive level few stocks have ever reached. Only 10 companies worldwide have achieved this level at the time of writing. One of the latest companies stepping through the doorway of this club is Taiwan Semiconductor (NYSE: TSM), although it can fluctuate under that mark based on day-to-day trading.

Taiwan Semiconductor is the world's largest contract chip manufacturer, and it has grown significantly over the past few years as we use more advanced technological devices. The latest surge that pushed it to the $1 trillion market cap threshold has come from chips used in artificial intelligence (AI), and the surge doesn't look like it's ending anytime soon.

New technology is a key driver in the future

Part of the reason Taiwan Semiconductor rose to the top is its culture of continuous innovation. While some chip fabricators struggled to produce certain technologies, Taiwan Semiconductor has often been at the forefront of these advances.

For example, the most advanced chip technology available currently is 3 nanometer (nm) chips. The distance describes the spacing between electrical traces on the chip. The smaller the number, the more transistors can be packed onto a chip to achieve greater power or improved energy consumption, depending on how it is configured.

3nm technology only started contributing to TSMC's revenue during last year's Q3 but has quickly risen to 30% of its overall revenue in this year's Q3. While 3nm technology is impressive, TSMC isn't resting on its laurels. It's actively working on 2nm chips, which management projects will start to contribute in 2025 and see a huge ramp in 2026. Early demand for these 2nm chips is greater than management saw for 3nm and 5nm chips, which likely comes from the fact that 2nm chips can be configured to consume 25% to 30% less energy when configured for the same output level.

This is huge for energy-thirsty computing tasks like AI processing, as the energy costs to run a data center are incredibly high. It's also useful for smartphones, as consumers always demand longer-lasting batteries.

Still, demand for AI chips is impressive right now, even with that innovation on the horizon.

Massive revenue growth is expected over the next few years

In the second quarter of 2023, management predicted that AI revenue would grow at a 50% compound annual growth rate (CAGR) for the next five years, when it would then make up a low-teens percentage of revenue. However, TSMC quickly exceeded those expectations.

Management now expects AI-related products to triple in revenue this year and make up a mid-teens percentage of overall revenue. That's a quick rise on an already aggressive growth projection and further strengthens Taiwan Semiconductor's investment thesis.

Overall, the company's guiding light has been management's projection that revenue will grow at a 15% to 20% CAGR over the "next several years." That's a quick growth projection considering TSMC's size, and the massive amount of AI revenue is likely pushing TSMC's CAGR toward the high end of that target range.

Considering the market (measured by the S&P 500) usually grows at a 10% CAGR over the long term, management's projection would indicate that Taiwan Semi has a strong chance of beating the market going forward, as long as it can be purchased at a reasonable price.

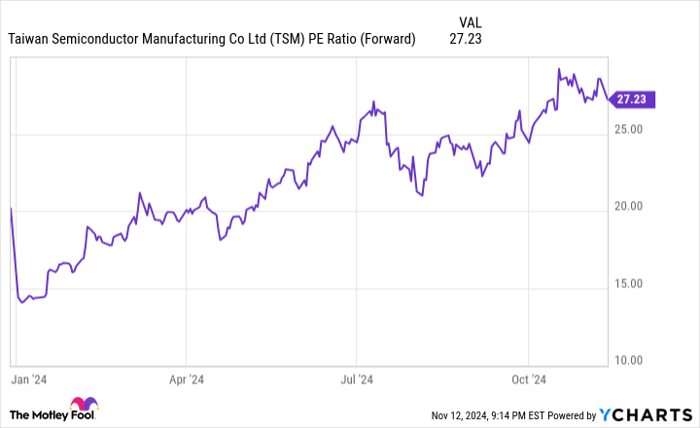

If the stock already has this growth priced into it, then investors have nothing more to gain from owning it. However, the stock is fairly priced from a forward price-to-earnings (P/E) perspective.

TSM PE Ratio (Forward) data by YCharts

Compared to the S&P 500's forward P/E ratio of 24.6, Taiwan Semi's stock isn't all that expensive, especially considering it's projected to grow faster than the S&P 500.

With the stock trading at a reasonable level plus strong growth projected ahead, Taiwan Semiconductor isn't done growing even though it has reached the $1 trillion valuation mark. I think Taiwan Semi is a top buy now, as it has several key growth drivers on the horizon, and it is one of my top ways to invest in the AI arms race.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $870,068!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 11, 2024

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.