This Small-Cap Stock Is Up 63% in 2024. Here's Why a Historic Opportunity Could Send It Even Higher.

LendingClub (NYSE: LC) has gone on a tear this year and outpaced the broader market, with the stock gaining almost 60% since the start of 2024. The consumer lender is in an excellent position to benefit from falling interest rates as consumers grapple with record-high credit card debt. According to a First Tech Federal Credit Union survey, 38% of consumers have considered consolidating their debt to save money on interest.

The Federal Reserve kicked off its interest rate easing cycle in September, dropping its benchmark interest rate by 50 basis points (or 0.5%) -- its first rate cut since the pandemic. With further interest rate cuts in the pipeline, LendingClub could capitalize on a potentially historic opportunity.

Consumer credit card debt is at a record level

Consumers have been incredibly resilient. Despite recessionary calls from economists during the past two years, the U.S. economy has held up quite well. The consumer has been a key source of strength, as people continue spending despite the Fed engaging in its most aggressive interest rate hiking cycle in four decades.

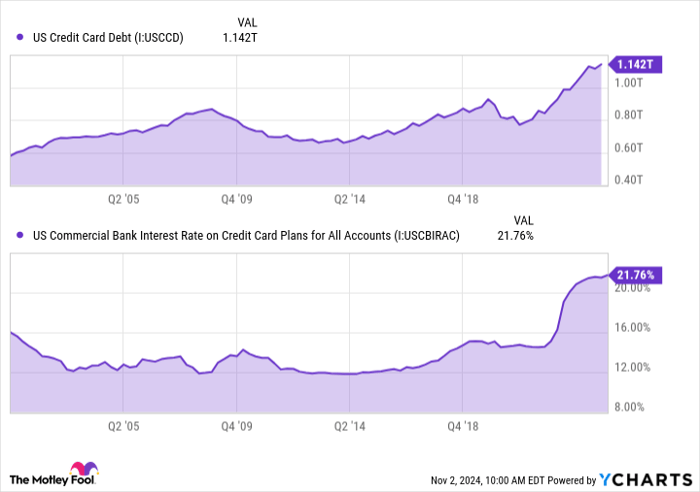

One way consumers have been able to keep up their spending habits is with credit cards. According to the Federal Reserve Bank of New York, consumers owe a record $1.142 trillion on credit cards through the end of the second quarter. These rising balances come when average credit card interest rates are near the highest on record.

US Credit Card Debt data by YCharts

How LendingClub can capitalize on a historic refinance opportunity

LendingClub, which started as a peer-to-peer lending platform, has carved out a niche in personal lending. The company acquired Radius Bancorp in 2021, letting it hold on to more of its loans against a base of low-cost deposits.

The company holds between 15% to 25% of its best-quality loans and sells the remainder to investors in the open market. When it sells loans, it earns revenue from origination and servicing fees. For loans it holds on to, it earns net interest income.

The combination of record-high credit card debt and falling interest rates could be a powerful tailwind for LendingClub's business. During the past year, LendingClub Chief Executive Officer Scott Sanborn has been preparing the company for what he calls "the historic refinance opportunity ahead."

The company has developed different products to help its members efficiently manage and consolidate their debts. One product it offers lets members sweep credit card balances into payment plans and top up existing loans. This can make it simple and easy for members to secure more funds to maintain a single payment on their consolidated debt.

In addition, LendingClub has partnered with Pagaya to acquire Tally Technologies' assets. The acquired assets include technology that simplifies credit card management and helps users optimize payments, reduce interest, and improve their credit. In a press release, LendingClub says it will "accelerate the evolution of LendingClub's member engagement platform to drive future growth."

Image source: Getty Images.

Be mindful of its credit quality

One potential concern for LendingClub and other lenders is rising net charge-offs for uncollectible loans, which could potentially signal increasing stress for its borrowers. Charge-offs across the banking sector have increased during the past year and a half. However, bank executives have said credit conditions are normalizing to pre-pandemic levels -- not due to systemic weakness among borrowers.

LendingClub's net charge-off rate fell from 6.2% of loans outstanding in the previous quarter to 5.4% in the most recent quarter. This was the second consecutive quarter in which its net charge-off rate fell. Its provision for credit losses decreased $17 million from one year ago to $47.5 million, and net income grew from $5 million a year ago to $14.5 million.

LendingClub is a buy today

LendingClub management projects it will originate $1.8 billion to $1.9 billion in loans in the fourth quarter. This would be little changed quarter over quarter but an increase from last year's fourth quarter, when originations were $1.6 billion.

Looking further down the road, the company should benefit from lower interest rates in 2025. According to the CME FedWatch Tool, market participants are pricing in another 100 basis point (1%) decrease in the federal funds rate during the next year.

With credit card debt at a record high and interest rates declining, LendingClub is in a prime position to benefit from a potentially huge tailwind to its lending business.

Should you invest $1,000 in LendingClub right now?

Before you buy stock in LendingClub, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and LendingClub wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $829,746!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of November 4, 2024

Courtney Carlsen has positions in LendingClub. The Motley Fool recommends CME Group and Pagaya Technologies. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.