AMD Stock Slides. Are There Cracks in the AI Infrastructure Story?

When it comes to chips for artificial intelligence (AI), Advanced Micro Devices (NASDAQ: AMD) continues to play second fiddle to leader Nvidia. However, it still benefits from the overall AI infrastructure build-out, as customers look to at least keep Nvidia (NASDAQ: NVDA) honest by getting some of their chips elsewhere.

While AMD put up strong AI-related growth, investors nonetheless sold off the stock. The shares now trade just in positive territory on the year.

Let's take a closer look at the chipmaker's third-quarter results to see if this is a buying opportunity or if this is a sign there could be some cracks in the AI buildout story for AMD.

Data-center growth

For the third quarter, AMD saw its sales rise 18% year over year to $6.8 billion. Adjusted earnings per share (EPS) came in at $0.92, up 31%. That was a nice acceleration in growth from Q2 when it saw sales rise 9% and adjusted EPS up 19%.

Its data center business once again led the way as revenue soared 122% year over year to $3.5 billion and 25% sequentially. The segment was driven by sales of its Instinct graphics processing units (GPUs) and EPYC central processing units (CPUs). AMD said that its EPYC CPUs have gained big deployments at large cloud companies, such as Microsoft and Meta Platforms, as well as with enterprise customers such as Adobe, Boeing, and Nestle.

Its client segment also showed strong growth, up 29% to $1.9 billion. This was led by demand for its Zen 5 processors. However, it saw big revenue declines in gaming, down 69% to $462 million, and embedded, down 25% to $927 million. Adjusted gross margins rose 250 basis points to 53.6% and were up 50 basis points sequentially.

For the quarter, AMD generated free cash flow of $496 million. It ended the quarter with net cash and short-term investments of $4.5 billion and $1.7 billion in debt.

Looking ahead, the company guided for Q4 revenue of $7.5 billion, give or take $300 million. That would represent growth of 22% at the mid-point, showing continued acceleration. It increased its full-year GPU data center revenue forecast from revenue of more than $4.5 billion to revenue now exceeding $5 billion.

Looking out toward 2025, AMD said it remains positive about continued data-center growth as companies continue to make significant investments to build out their infrastructure to run AI workloads. It also said that customers are beginning to broaden their workloads running its GPUs.

Image source: Getty Images.

Is now the time to buy the dip?

Like its larger rival Nvidia, AMD is seeing its growth driven by continued demand from the buildout of AI infrastructure. However, the company has found more success with AI inference, although it has made some inroads into large language model (LLM) training. While AMD is unlikely to challenge Nvidia's dominance, it is carving out a nice niche. Meanwhile, given how quickly the AI infrastructure market is growing, if it is able to gain just a little share, it will equal a lot of growth for the company moving forward.

The impending acquisition of ZTE Systems (which designs and builds server, storage, accelerator, and other equipment for data centers) will help the company compete even better in the data center, allowing it to sell end-to-end system solutions that can incorporate its GPUs, CPUs, and networking equipment. This should also allow for faster deployments, which is something that should attract companies that have been racing to build out their data center infrastructure.

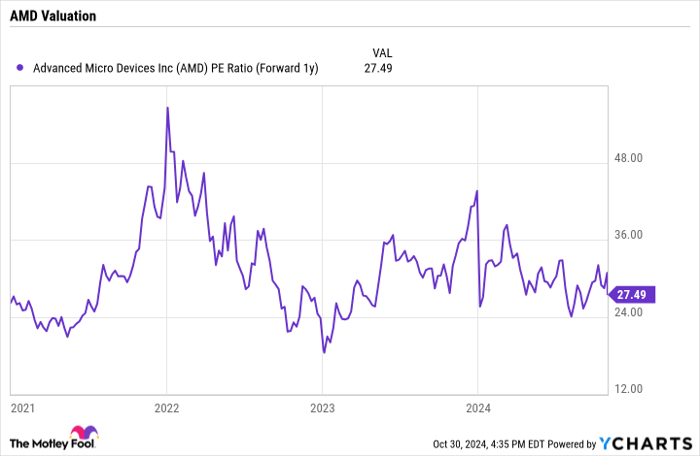

From a valuation perspective, AMD trades at a forward price-to-earnings ratio (P/E) of 27.5 times next year's analyst estimates. Given the growth opportunities in front of it, that is a pretty reasonable valuation.

AMD PE Ratio (Forward 1y) data by YCharts.

While I still would prefer Nvidia in the space given its extraordinary growth, I do think AMD should continue to benefit from the AI-powered data center build-out. Also, the ZTE acquisition could set it up to make more inroads in the data center space.

As such, I think investors can buy the stock on the recent dip, as I see no indication of any cracks in the AI infrastructure story.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,292!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,169!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,758!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Advanced Micro Devices, Meta Platforms, Microsoft, and Nvidia. The Motley Fool recommends Nestlé and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.