This Dow Dividend Growth Stock Just Delivered Record Results and Raised Its Dividend to An All-Time High. Here's Why It's a Screaming Buy in November.

Visa (NYSE: V) stock touched a new all-time intraday high on Oct. 31, just two days after the financial services giant reported blowout fourth-quarter and full-year fiscal 2024 results. The Dow Jones Industrial Average component has been a long-term winner, but has underperformed the S&P 500 so far this year.

Here's why Visa stands out to me as a high-conviction Dow stock to buy in November, and why its fiscal 2024 was a year to remember.

Image source: Getty Images.

Visa's keeps growing no matter the challenges

Visa has really outdone itself the past few years. During a period when many consumer-facing companies have delivered poor results, its top and bottom lines still grew. Sure, its growth has slowed a bit. But its strong results illustrate the power of its diversified revenue streams, network effects, and its ability to win new customers.

Every time a credit or debit card is swiped, tapped, or processed digitally using its network, Visa makes money. Its fee structure is based on payment volume and the number of processed transactions, so it earns fees even if consumers and business clients are spending less.

There is no shortage of companies that have pointed to inflation, higher interest rates, and the complicated macroeconomic backdrop as reasons for a pullback in consumer discretionary spending. So if there had ever been a year for Visa to report weak results, it would have been this one. But its total payments volume still rose by 8%, processed transactions rose by 10%, and cross-border volume increased by 15%. These results show that Visa's international business helped compensate for a little changed domestic business, and that it isn't just relying on a higher number of processed transactions. In other words, overall, customers are spending more with Visa cards and using them more often.

Network effects refer to a platform or system increasing in value the more it is used. The more merchants that accept Visa as a form of payment and the more consumers and businesses that use Visa as their preferred payment method, the stronger the overall network. More users mean more revenue for the payment processor, and more cash flow that it can use to strengthen the security of its network, run marketing campaigns and promotions, and win deals with big clients.

In its fiscal fourth quarter, which ended Sept. 30, Visa renewed its largest clients in Latin America, Asia-Pacific, Canada, Central Europe, the Middle East, and Africa. It also extended its partnerships with U.S. Bank and USAA.

"Across all of our regions and all of our fintech partners from early stage to mature, we signed over 650 commercial partnerships, up 30% from last year," Chief Executive Officer Ryan McInerney said on the earnings call.

Visa value-added services revenue rose by 22% in fiscal 2024. Valued-added services help target digital-first payment experiences, streamline checkout experiences, process account-to-account payments, and more. For example, Visa Alias Directory can help protect sensitive information by assigning an alias to a linked bank account or debit card so that financial institutions, service providers, networks, governments, and businesses can protect their customers.

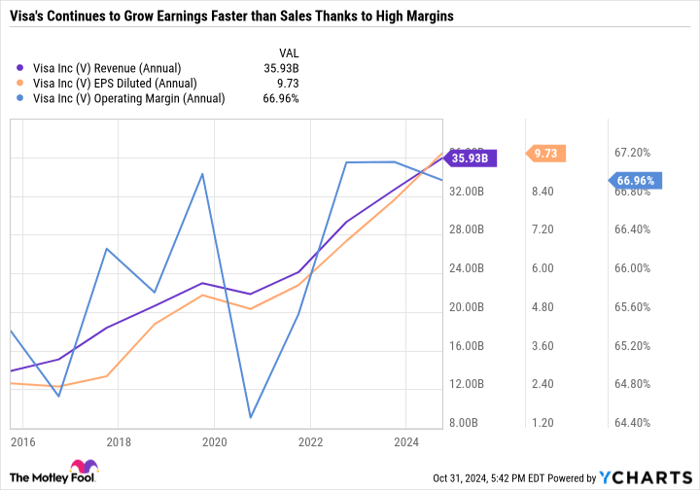

All told, Visa's annual revenue and diluted earnings per share (EPS) reached all-time highs, and operating margins of 67% remained near all-time highs -- showing how the company continues to deliver top- and bottom-line strength.

V Revenue (Annual) data by YCharts

Visa's huge capital return program

Visa returned $20.9 billion to shareholders in fiscal 2024 -- including $16.71 billion in stock repurchases and $4.22 billion in dividends. In conjunction with the recent report, it hiked its quarterly payout by 13% to $0.59 per share. In October 2019, Visa raised its dividend to $0.30, meaning it has essentially doubled the payout in the past five years. Buybacks have reduced its share count outstanding by 11.1% during the past five years and 21.2% in the past decade.

The company is able to pass along so much profit to shareholders because it has a strong balance sheet, and it generates so much more profit than it needs to run and expand the business.

It finished its fiscal year with cash and cash equivalents of $11.98 billion, investment securities of $3.2 billion, and long-term debt of $20.84 billion. With a low net-debt position, it doesn't feel pressure to use excess profits to pay down debt, so it can instead pass them along to shareholders.

Visa has the type of cash cow business model that gives it a high-quality earnings profile. As the company just proved, it can grow even when macroeconomic factors are working against it. It's a much more predictable business than a company that must spend a ton of money building cars, drilling oil, selling shoes, or producing shows and movies.

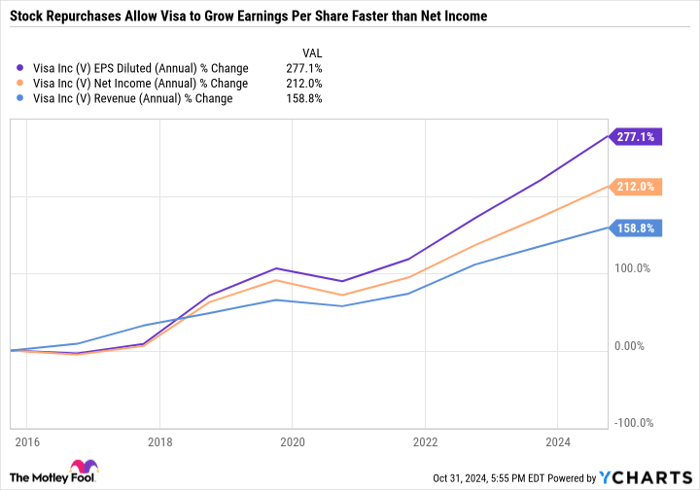

The following chart showcases the impact of high-margin growth paired with stock buybacks over time.

V EPS Diluted (Annual) data by YCharts.

During the past decade, Visa's revenue has increased by 159%. However, its net income grew even more because its network can handle more business with minimal increases in operating costs. Even better, diluted EPS grew faster than net income because buybacks reduced the share count. Visa pulls three levers to boost its EPS -- artificially through buybacks, organically through its own innovations and growth, and inorganically through mergers and acquisitions.

Visa is still a great value

Despite hovering near an all-time high, Visa isn't expensive. The company sports a price-to-earnings (P/E) ratio of 29.8, which is only slightly higher than the S&P 500 P/E ratio of 29.1. And yet, its business model and the strength of its earnings are significantly above the average S&P 500 component.

Visa has proven it can overcome challenges and remains committed to returning capital to shareholders through dividends and buybacks. It stands out as one of the best Dow components, and best stocks in general, to buy now.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,292!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,169!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $407,758!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of October 28, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Visa. The Motley Fool has a disclosure policy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.