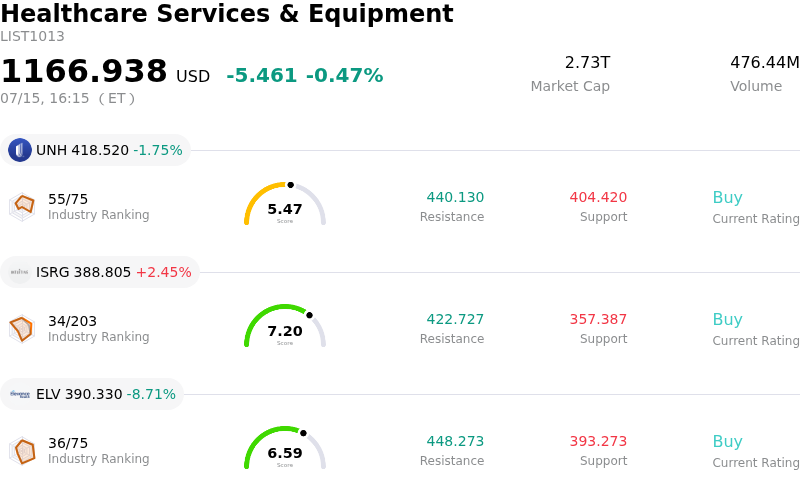

Elevance Health Inc Stock (ELV) Closed Down by 8.71% on Jul 15: Key Drivers Unveiled

Elevance Health Inc (ELV) closed down by 8.71%. The Healthcare Services & Equipment sector is down by 0.47%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Unitedhealth Group Inc (UNH) down 1.75%; Intuitive Surgical Inc (ISRG) up 2.45%; Elevance Health Inc (ELV) down 8.71%.

What is driving Elevance Health Inc (ELV)’s stock price down today?

The sharp decline in Elevance Health shares reflects deepening investor concerns regarding the rising medical loss ratio across the managed care sector. Institutional selling accelerated following reports that healthcare utilization rates, particularly within the senior and Medicaid populations, have exceeded internal projections. This uptick in medical costs suggests that the pricing power previously enjoyed by large insurers is being eroded by persistent inflation in clinical services and outpatient procedures.

A primary driver behind this volatility is the updated guidance regarding the company's benefit expense ratio. Elevated utilization in specialty pharmacy and orthopedic surgeries has forced a reassessment of full-year margin targets. For a company like Elevance Health, which maintains a significant footprint in government-sponsored programs, even a marginal increase in the cost-to-premium ratio can have a disproportionate impact on net income expectations. Analysts are now questioning whether the premium hikes implemented in the last enrollment cycle are sufficient to offset the current pace of medical spend.

Regulatory headwinds are also weighing heavily on market sentiment. Recent communications from the Centers for Medicare and Medicaid Services indicate a more stringent environment for reimbursement rates and risk adjustment scores. As the federal government seeks to tighten fiscal spending, managed care organizations face the prospect of lower-than-anticipated funding for Medicare Advantage plans. This creates a challenging outlook for upcoming cycles, as the gap between government payments and actual care costs continues to widen, prompting institutional investors to de-risk their portfolios in favor of less regulated sectors.

The broader macroeconomic environment adds another layer of complexity to the downward pressure. While the labor market remains relatively stable, shifts in commercial enrollment patterns and the potential for increased Medicaid redetermination challenges are creating uncertainty. As several prominent research firms have revised their price targets downward in response to these operational hurdles, the prevailing narrative has shifted from steady growth to margin preservation. Until the company can demonstrate a stabilization in medical cost trends or receive more favorable regulatory clarity, the stock is likely to face continued headwinds from both algorithmic trading and fundamental re-evaluation by long-term holders.

Technical Analysis of Elevance Health Inc (ELV)

Technically, Elevance Health Inc (ELV) shows a MACD (12,26,9) value of 4.145, indicating a buy signal. The RSI at 62.914 suggests neutral condition and the Williams %R at 17.182 suggests overbought condition. Please monitor closely.

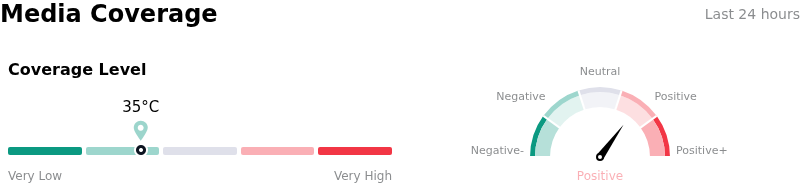

Media Coverage of Elevance Health Inc (ELV)

In terms of media coverage, Elevance Health Inc (ELV) shows a coverage score of 35, indicating a low level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Elevance Health Inc (ELV)

Elevance Health Inc (ELV) is in the Healthcare Services & Equipment industry. Its latest annual revenue is $199.12B, ranking 4 in the industry. The net profit is $5.66B, ranking 4 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $440.60, a high of $498.00, and a low of $331.00.

More details about Elevance Health Inc (ELV)

Company Specific Risks:

- Dramatic Guidance Revision: Management slashed full-year 2024 adjusted EPS guidance to approximately $33.00 from the previously expected $37.20, reflecting a severe deterioration in earnings visibility and a sudden shift in the company's profitability outlook.

- Escalating Medicaid Medical Costs: The company is experiencing a significant "mismatch" in the Medicaid segment, where state reimbursement rates have failed to keep pace with the higher-than-anticipated health acuity of members remaining after the post-pandemic redetermination process.

- Substantial Earnings Miss: Reported third-quarter adjusted EPS of $8.37 fell sharply below the consensus estimate of $9.66, highlighting an immediate failure to manage medical loss ratios (MLR) effectively within its core insurance business.

- Lagging Regulatory Rate Adjustments: There is a heightened risk that state-negotiated rate increases will be insufficient or too delayed to offset persistent medical cost trends, threatening margin recovery and operational performance through the first half of 2025.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.