Booking Holdings Inc Stock (BKNG) Moved Up by 3.99% on Jul 15: What Investors Need To Know

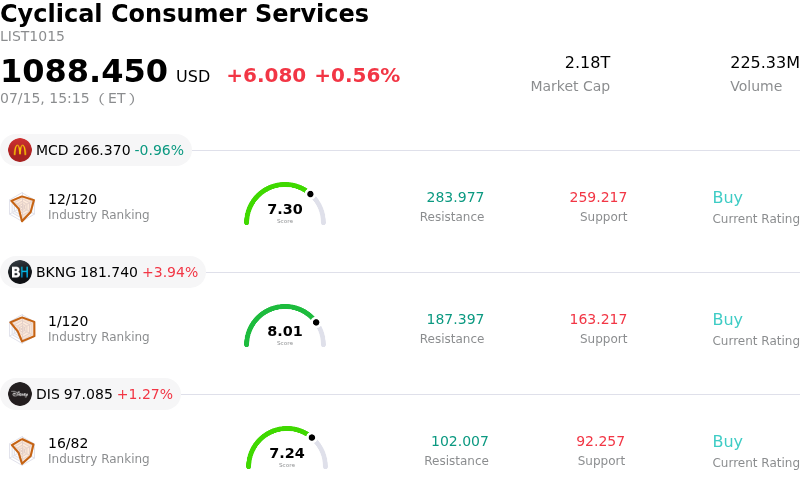

Booking Holdings Inc (BKNG) moved up by 3.99%. The Cyclical Consumer Services sector is up by 0.56%. The company outperformed the industry. Top 3 stocks by turnover in the sector: McDonald's Corp (MCD) down 0.96%; Booking Holdings Inc (BKNG) up 3.99%; Walt Disney Co (DIS) up 1.28%.

What is driving Booking Holdings Inc (BKNG)’s stock price up today?

Booking Holdings is experiencing upward momentum as the mid-July peak travel season demonstrates stronger-than-expected resilience in global consumer discretionary spending. Investors are responding positively to high-frequency travel data indicating that international flight volumes and hotel occupancy rates in key European and North American markets are tracking ahead of historical seasonal norms. This macro-level strength provides a supportive backdrop for the company, which remains a primary beneficiary of the ongoing shift toward experience-based consumption.

The current market enthusiasm is further bolstered by favorable macroeconomic signals, particularly cooling inflationary pressures that have eased concerns regarding a potential slowdown in household leisure budgets. As the Federal Reserve signals a more stable policy environment, the broader travel and leisure sector has seen a rotation of institutional capital into high-quality growth names. Booking Holdings, with its dominant market share and robust margins, is capturing a significant portion of this sector-wide re-rating.

Anticipation ahead of the upcoming quarterly earnings cycle is also playing a critical role in the current price action. Analysts have recently issued several notes highlighting strong alternative data metrics, including accelerated mobile app engagement and increased alternative accommodation listings. These indicators suggest that the company is effectively capturing market share from traditional competitors while maintaining pricing power in its core agency model. This positive sentiment is leading to preemptive positioning by institutional investors who expect a beat-and-raise scenario for the remainder of the fiscal year.

Despite the intraday volatility, the underlying technical structure remains constructive. The movement reflects a convergence of short-term seasonal demand and a longer-term strategic shift toward the Connected Trip initiative, which integrates flights, stays, and ground transportation into a single ecosystem. While geopolitical uncertainties and currency fluctuations remain persistent risks for global travel aggregators, the current trajectory is driven by fundamental confidence in the company’s ability to leverage its scale and technological edge in a highly competitive digital landscape.

Technical Analysis of Booking Holdings Inc (BKNG)

Technically, Booking Holdings Inc (BKNG) shows a MACD (12,26,9) value of -1.540, indicating a neutral signal. The RSI at 50.203 suggests neutral condition and the Williams %R at 74.778 suggests sell condition. Please monitor closely.

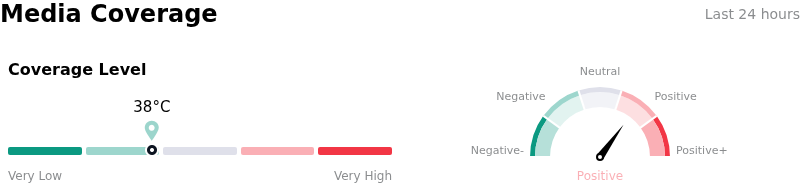

Media Coverage of Booking Holdings Inc (BKNG)

In terms of media coverage, Booking Holdings Inc (BKNG) shows a coverage score of 38, indicating a low level of media attention. The overall market sentiment index is currently in bullish zone.

Fundamental Analysis of Booking Holdings Inc (BKNG)

Booking Holdings Inc (BKNG) is in the Cyclical Consumer Services industry. Its latest annual revenue is $26.92B, ranking 2 in the industry. The net profit is $5.40B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $225.67, a high of $298.00, and a low of $175.00.

More details about Booking Holdings Inc (BKNG)

p>Company Specific Risks:

- Regulatory Fines and Legal Headwinds: The Spanish competition regulator (CNMC) is proceeding with a proposed $530 million fine for alleged anti-competitive practices, signaling increased legal liabilities and potential contagion of regulatory scrutiny across other European jurisdictions.

- DMA Compliance Impacts: Following its formal designation as a 'gatekeeper' under the EU's Digital Markets Act, the company must eliminate price parity clauses, which risks diluting its value proposition to consumers and reducing its overall take-rate from hotel partners.

- Growth Normalization Concerns: Recent analyst commentary points to a deceleration in room-night growth as the 'revenge travel' cycle concludes, raising the risk of future guidance downgrades if consumer discretionary spending in the Eurozone continues to soften.

- Rising Customer Acquisition Costs: Intensified competition from alternative lodging and direct-booking initiatives by major hotel chains is forcing higher outlays in performance marketing, creating downward pressure on adjusted EBITDA margins.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.