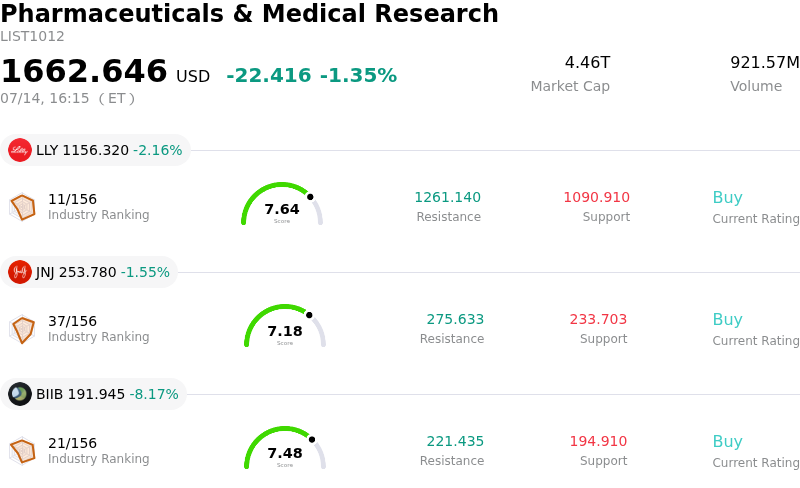

Bristol-Myers Squibb Co Stock (BMY) Closed Down by 3.99% on Jul 14: Drivers Behind the Movement

Bristol-Myers Squibb Co (BMY) closed down by 3.99%. The Pharmaceuticals & Medical Research sector is down by 1.35%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Eli Lilly and Co (LLY) down 2.16%; Johnson & Johnson (JNJ) down 1.55%; Biogen Inc (BIIB) down 8.17%.

What is driving Bristol-Myers Squibb Co (BMY)’s stock price down today?

Bristol-Myers Squibb is experiencing notable downward pressure following a series of clinical and strategic developments that have dampened investor enthusiasm. The primary driver appears to be disappointing data from a late-stage clinical trial involving a key candidate in the companys oncology pipeline. As a major player in the immunotherapy space, any setback in a Phase 3 study intended to diversify its portfolio beyond its aging blockbuster treatments is viewed as a significant hurdle to long-term revenue sustainability.

The market is also reacting to heightened concerns surrounding the impending patent cliff for several of the companys highest-grossing medications. With generic competition looming for critical revenue drivers, investors are scrutinizing the pace at which newer product launches can offset these losses. Todays sentiment suggests that the current growth trajectory of the newer commercial portfolio may not be sufficient to bridge the fiscal gap projected for the latter half of the decade.

External analyst commentary has added to the bearish sentiment, as multiple research firms have adjusted their price targets downward. These revisions often cite tightening margins due to increased research and development spending and the potential impact of government-led drug price negotiations. Such regulatory headwinds continue to weigh on the pharmaceutical sector, particularly for companies with high exposure to Medicare-heavy revenue streams.

Broader market dynamics are also playing a role in the stocks performance. A rotation of capital away from defensive healthcare names into more cyclical or growth-oriented sectors has limited the buying support for Bristol-Myers Squibb. This shift in institutional positioning, combined with the company-specific news, has led to increased volatility and a reduction in the stocks valuation multiple as the market reassesses its risk-adjusted outlook.

Technical Analysis of Bristol-Myers Squibb Co (BMY)

Technically, Bristol-Myers Squibb Co (BMY) shows a MACD (12,26,9) value of 0.563, indicating a buy signal. The RSI at 59.102 suggests neutral condition and the Williams %R at 2.144 suggests overbought condition. Please monitor closely.

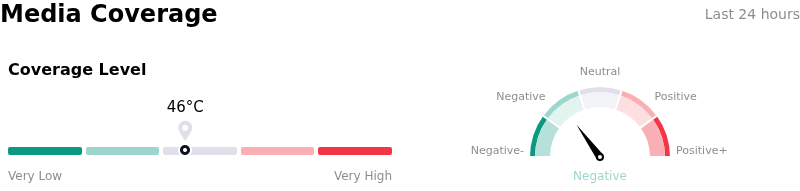

Media Coverage of Bristol-Myers Squibb Co (BMY)

In terms of media coverage, Bristol-Myers Squibb Co (BMY) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Bristol-Myers Squibb Co (BMY)

Bristol-Myers Squibb Co (BMY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $48.19B, ranking 11 in the industry. The net profit is $7.05B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $61.90, a high of $75.00, and a low of $33.10.

More details about Bristol-Myers Squibb Co (BMY)

Company Specific Risks:

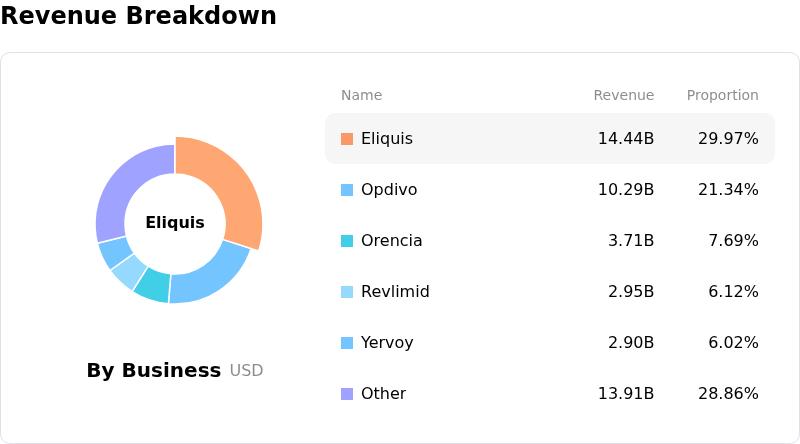

- Medicare Price Negotiation Headwinds: As a primary target of the Inflation Reduction Act’s (IRA) initial price negotiations for Eliquis, the company faces imminent downward pressure on its top-line revenue and net pricing power, creating significant valuation uncertainty among institutional investors.

- Concentrated Patent Cliff Exposure: Bristol-Myers Squibb is approaching a critical "revenue hole" as its two largest blockbusters, Opdivo and Eliquis, face loss of exclusivity (LOE) in the 2026–2028 window, with current pipeline assets failing to provide a clear path to fully offset the projected multi-billion dollar revenue decline.

- M&A Integration and EPS Dilution: The recent multibillion-dollar acquisitions of Karuna Therapeutics and RayzeBio have resulted in massive one-time Acquired In-Process Research and Development (IPRD) charges, which have severely diluted 2024–2025 EPS guidance and restricted the company's near-term dividend growth potential.

- Regulatory Challenges to Patent Listings: Recent Federal Trade Commission (FTC) scrutiny regarding the "improper" listing of patents in the FDA's Orange Book has targeted BMY’s portfolio, increasing the risk of accelerated generic entries and threatening the extended lifecycle management of key therapeutic franchises.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.