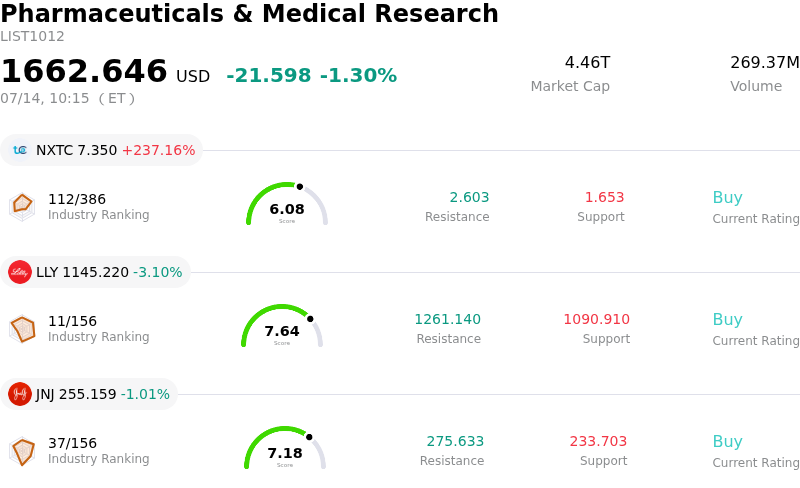

Eli Lilly and Co Stock (LLY) Moved Down by 3.10% on Jul 14: Facts Behind the Movement

Eli Lilly and Co (LLY) moved down by 3.10%. The Pharmaceuticals & Medical Research sector is down by 1.30%. The company underperformed the industry. Top 3 stocks by turnover in the sector: NextCure Inc (NXTC) up 237.16%; Eli Lilly and Co (LLY) down 3.10%; Johnson & Johnson (JNJ) down 1.01%.

What is driving Eli Lilly and Co (LLY)’s stock price down today?

The downward pressure on Eli Lilly and Company today stems largely from a confluence of sector-wide profit taking and intensifying competitive concerns within the metabolic health space. After a period of significant outperformance driven by the success of its weight-loss and diabetes portfolio, institutional investors appear to be recalibrating their exposure. This shift is partly a response to a broader market rotation where capital is flowing out of high-multiple growth leaders and into cyclical sectors that have lagged behind, reflecting a shift in tactical asset allocation for the second half of the year.

The competitive landscape is providing a catalyst for this retreat as recent data from smaller biotech rivals suggests a narrowing gap in the development of next-generation obesity treatments. Reports of successful mid-stage trials for oral non-peptide GLP-1 agonists from competitors have introduced questions regarding the long-term pricing power and market share of Eli Lilly’s injectable offerings. While the company maintains a dominant position, the prospect of a more crowded market by the end of the decade is forcing analysts to reconsider the terminal value assumptions used in their valuation models.

Regulatory headwinds are also playing a significant role in dampening investor enthusiasm. Increased rhetoric from federal agencies regarding the cost of blockbuster medications has heightened fears of more aggressive price negotiations. Specifically, concerns that state and federal insurance programs may implement stricter reimbursement hurdles for weight-loss drugs have created an overhang on the stock. Investors are weighing the risk that volume growth may eventually be offset by mandatory price concessions, which would impact the high-margin profile that has historically justified the stock’s premium valuation.

From an operational standpoint, any perceived friction in the scaling of manufacturing capacity remains a sensitive point for the market. Despite massive capital expenditures to increase output for its primary growth drivers, the complexity of the global supply chain for biologics leaves little room for error. Observations of supply inconsistencies or delays in facility certifications can lead to swift adjustments in earnings expectations. When combined with the technical exhaustion of the stock after reaching record highs earlier in the year, these fundamental pressures have triggered a period of heightened intraday volatility as the market seeks a more sustainable floor.

Technical Analysis of Eli Lilly and Co (LLY)

Technically, Eli Lilly and Co (LLY) shows a MACD (12,26,9) value of -6.937, indicating a neutral signal. The RSI at 55.651 suggests neutral condition and the Williams %R at 39.699 suggests buy condition. Please monitor closely.

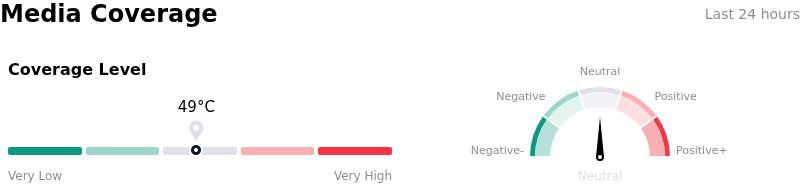

Media Coverage of Eli Lilly and Co (LLY)

In terms of media coverage, Eli Lilly and Co (LLY) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Eli Lilly and Co (LLY)

Eli Lilly and Co (LLY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $65.18B, ranking 4 in the industry. The net profit is $20.64B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $1237.54, a high of $1500.00, and a low of $850.00.

More details about Eli Lilly and Co (LLY)

Company Specific Risks:

- Intensifying Competitive Landscape: Recent positive clinical data from competitors, notably Roche’s oral GLP-1 candidate, has heightened investor concerns regarding the long-term market share dominance of Eli Lilly’s incretin franchise, potentially compressing valuation multiples as the obesity market becomes more crowded.

- Legislative and Pricing Scrutiny: Renewed pressure from the U.S. Senate Health, Education, Labor, and Pensions (HELP) Committee regarding the high domestic cost of Zepbound and Mounjaro compared to international markets creates a significant regulatory risk that could lead to mandatory price concessions or unfavorable reimbursement shifts.

- Persistent Supply Chain Volatility: Despite massive capital investments, ongoing FDA-listed shortages for specific doses of tirzepatide limit the company’s ability to meet current peak demand, resulting in lost revenue opportunities and allowing competitors to capture patients through improved availability.

- Product Liability and Safety Litigation: An increasing number of legal filings alleging "stomach paralysis" (gastroparesis) and other severe gastrointestinal side effects associated with GLP-1 receptor agonists present a growing tail risk for unexpected legal settlements and the potential for more restrictive FDA warning labels.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.