Bristol-Myers Squibb Co Stock (BMY) Closed Up by 3.07% on Jul 13: Key Drivers Unveiled

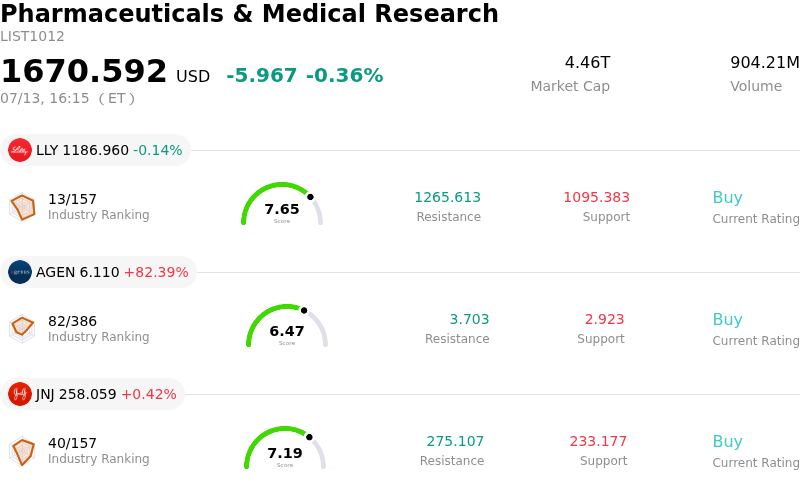

Bristol-Myers Squibb Co (BMY) closed up by 3.07%. The Pharmaceuticals & Medical Research sector is down by 0.36%. The company outperformed the industry. Top 3 stocks by turnover in the sector: Eli Lilly and Co (LLY) down 0.14%; Agenus Inc (AGEN) up 82.39%; Johnson & Johnson (JNJ) up 0.42%.

What is driving Bristol-Myers Squibb Co (BMY)’s stock price up today?

Bristol-Myers Squibb has experienced a notable uptick in market valuation as investors react to a series of positive catalysts within its oncology and immunology divisions. The primary driver appears to be the release of favorable clinical data regarding a high-potential pipeline candidate, which reinforces the company strategy to diversify its revenue streams ahead of looming patent expirations for its legacy blockbusters. This development significantly mitigates long-term growth concerns that have historically weighed on the stock multiple.

Market sentiment has been further bolstered by progress regarding regulatory milestones in international markets. These expansions for the company newer product portfolio, particularly in the cell therapy and precision medicine segments, signal a robust trajectory for global market share gains. Institutional investors have responded by increasing their weightings in the stock, viewing it as a defensive play with significant upside potential relative to its peers in the large-cap pharmaceutical space.

Furthermore, the broader macroeconomic environment has favored high-dividend-yielding pharmaceutical stocks as participants seek stability amidst fluctuating interest rate expectations. Analysts have recently adjusted their earnings forecasts upward, citing better-than-expected margin expansion resulting from the company recent restructuring initiatives and cost-optimization programs. The successful integration of recent acquisitions has also demonstrated management ability to execute on its long-term strategic vision, providing a clearer path for sustainable cash flow.

The combination of pipeline de-risking and improved operational efficiency has led to a renewed sense of confidence among retail and institutional participants. As the market shifts its focus toward companies with strong balance sheets and proven research and development capabilities, Bristol-Myers Squibb stands out as a beneficiary of this flight to quality. The current momentum reflects a fundamental reassessment of the company valuation as it transitions from its traditional reliance on older assets to a more diversified, innovation-driven growth model.

Technical Analysis of Bristol-Myers Squibb Co (BMY)

Technically, Bristol-Myers Squibb Co (BMY) shows a MACD (12,26,9) value of 0.410, indicating a buy signal. The RSI at 52.872 suggests neutral condition and the Williams %R at 26.612 suggests buy condition. Please monitor closely.

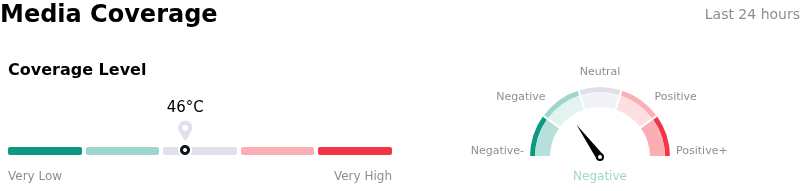

Media Coverage of Bristol-Myers Squibb Co (BMY)

In terms of media coverage, Bristol-Myers Squibb Co (BMY) shows a coverage score of 46, indicating a moderate level of media attention. The overall market sentiment index is currently in bearish zone.

Fundamental Analysis of Bristol-Myers Squibb Co (BMY)

Bristol-Myers Squibb Co (BMY) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $48.19B, ranking 11 in the industry. The net profit is $7.05B, ranking 12 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $61.90, a high of $75.00, and a low of $33.10.

More details about Bristol-Myers Squibb Co (BMY)

Company Specific Risks:

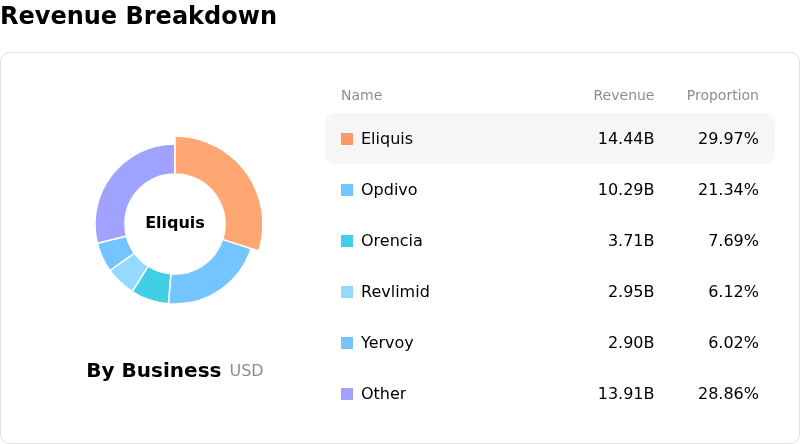

- Patent Expiry Concentration: The company faces a looming "patent cliff" for its primary revenue drivers, Eliquis and Opdivo, later this decade; analysts remain concerned that the new product portfolio's current growth trajectory is insufficient to offset the projected multi-billion dollar revenue void.

- Medicare Price Negotiation Pressure: Under the Inflation Reduction Act (IRA), Eliquis has been targeted for the first round of CMS price negotiations, which is expected to result in significant downward pressure on domestic net pricing and margin compression starting in the 2026 fiscal cycle.

- High Commercialization Hurdles: Intraday volatility is linked to skepticism regarding the launch ramp for Cobenfy (KarXT); despite FDA approval, the high costs of sales and marketing, combined with the slow pace of gaining broad formulary access, present immediate risks to short-term earnings targets.

- Elevated Debt and Interest Burdens: Following the aggressive acquisition strategy involving Karuna Therapeutics and RayzeBio, the company's balance sheet carries substantial debt, leading to increased interest expenses and recurring acquired in-process research and development (IPRD) charges that weigh on GAAP profitability.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.