AstraZeneca PLC Stock (AZN) Moved Down by 3.50% on Jul 10: Key Drivers Unveiled

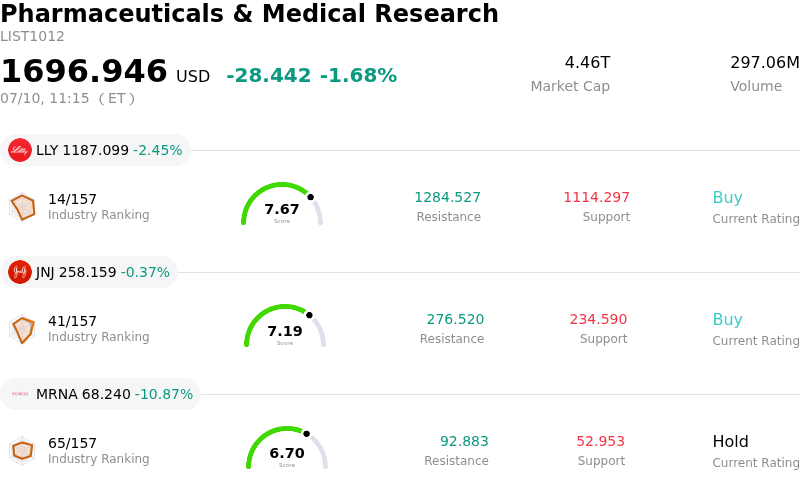

AstraZeneca PLC (AZN) moved down by 3.50%. The Pharmaceuticals & Medical Research sector is down by 1.68%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Eli Lilly and Co (LLY) down 2.45%; Johnson & Johnson (JNJ) down 0.37%; Moderna Inc (MRNA) down 10.87%.

What is driving AstraZeneca PLC (AZN)’s stock price down today?

AstraZeneca has experienced a notable decline in share price during today's session, primarily driven by disappointing clinical data from a high-stakes late-stage trial. Investor sentiment shifted negatively following the release of topline results for an experimental oncology treatment, which failed to meet its primary endpoint of progression-free survival compared to the current standard of care. This setback is particularly impactful as the market had priced in significant future revenue growth from this specific therapeutic pathway, leading to a swift reassessment of the company’s near-term growth trajectory in its key oncology portfolio.

The pharmaceutical giant is also facing broader headwinds stemming from increased regulatory scrutiny and pricing pressures. Reports suggest that federal health authorities are intensifying their review of drug pricing structures, which could potentially compress margins for top-tier biological products. This regulatory uncertainty, combined with today's clinical miss, has prompted several institutional desks to adjust their risk-weighted models, resulting in an uptick in selling volume and heightened intraday volatility as funds rebalance their exposure to the healthcare sector.

Market sentiment was further dampened by a cautious outlook from analysts who had previously maintained buy ratings on the stock. Several investment banks have updated their notes to reflect a more conservative valuation, citing the increased execution risk following the recent trial outcome. While the company maintains a robust pipeline and diversified revenue streams across biopharmaceuticals and rare diseases, the immediate focus of the market has shifted toward the potential for downward revisions in earnings guidance for the upcoming fiscal periods.

External macroeconomic factors have also played a role in the day's movement. As investors react to shifting interest rate expectations and currency fluctuations, multinational entities with significant overseas exposure like AstraZeneca are seeing increased sensitivity to dollar strength. The combination of specific clinical disappointments and a broader rotation out of defensive healthcare stocks has created a challenging environment, leaving the stock vulnerable to further technical pressure until more definitive positive catalysts emerge from its remaining pipeline candidates.

Technical Analysis of AstraZeneca PLC (AZN)

Technically, AstraZeneca PLC (AZN) shows a MACD (12,26,9) value of 0.460, indicating a buy signal. The RSI at 43.530 suggests neutral condition and the Williams %R at 75.772 suggests sell condition. Please monitor closely.

Fundamental Analysis of AstraZeneca PLC (AZN)

AstraZeneca PLC (AZN) is in the Pharmaceuticals & Medical Research industry. Its latest annual revenue is $58.74B, ranking 8 in the industry. The net profit is $10.22B, ranking 6 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $224.36, a high of $250.69, and a low of $187.55.

More details about AstraZeneca PLC (AZN)

Company Specific Risks:

- Strategic Execution Risk: The newly announced target to reach $80 billion in total revenue by 2030 has introduced significant volatility as analysts question the feasibility of launching 20 new medicines and maintaining high margins without dilutive acquisitions.

- China Regulatory Investigations: Ongoing probes into the company’s regional leadership in China regarding potential data privacy violations and illegal drug distribution continue to pose a threat to the stability of a key growth market that contributes over 13% of total revenue.

- Oncology Pipeline Underperformance: Recent clinical data for datopotamab deruxtecan (Dato-DXd) failed to show statistically significant overall survival in some lung cancer trials, leading to downward revisions in peak sales expectations and increased regulatory approval risk.

- Margin Compression from Manufacturing Expansion: Plans to invest billions in new manufacturing facilities in the US and Singapore are expected to weigh on short-term free cash flow and operating margins, especially if global pricing pressures in the pharmaceutical sector intensify.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.