Rio Tinto PLC Stock (RIO) Moved Down by 3.13% on Jul 8: Drivers Behind the Movement

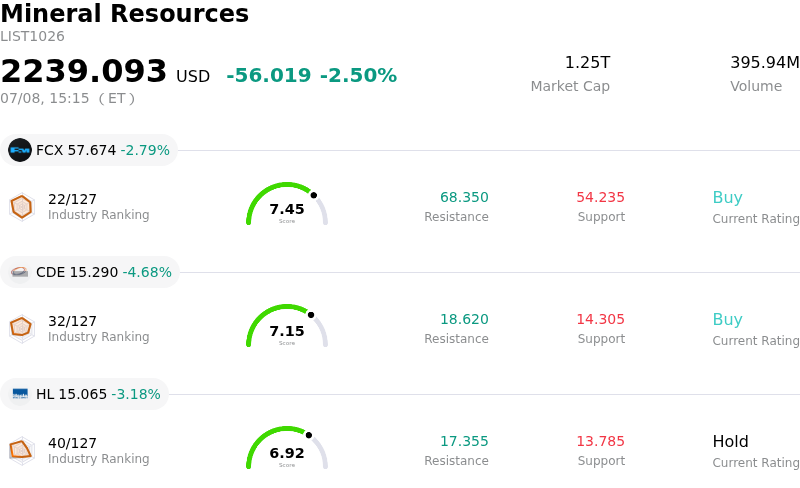

Rio Tinto PLC (RIO) moved down by 3.13%. The Mineral Resources sector is down by 2.50%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Freeport-McMoRan Inc (FCX) down 2.79%; Coeur Mining Inc (CDE) down 4.68%; Hecla Mining Co (HL) down 3.13%.

What is driving Rio Tinto PLC (RIO)’s stock price down today?

The downward movement in Rio Tinto shares is primarily driven by escalating geopolitical tensions in the Middle East. A sudden escalation in hostilities sparked a risk-off sentiment across global equity markets. While oil prices surged as a result of these supply disruption fears, broader industrial metal prices retreated, hitting key resource giants and basic materials producers particularly hard. As a major producer of copper, aluminum, and iron ore, Rio Tinto is highly sensitive to shifts in global commodity pricing and industrial demand forecasts, both of which weakened alongside the geopolitical escalation.

The broader macroeconomic environment also exerted downward pressure on the stock. Treasury yields climbed higher as global inflation and interest rate concerns persisted. Rising yields increase the cost of capital for capital-intensive mining companies and lower the present value of future cash flows, leading to portfolio adjustments by institutional investors away from heavy industry equities. This macro pressure is further exacerbated by anticipated Chinese economic data, which often heavily influences demand projections for key metals like iron ore.

In terms of company-specific events, Rio Tinto announced that it would not exercise its option to become the operator of Sovereign Metals' Kasiya rutile-graphite project in Malawi. While the company maintained that this decision aligns with its refined corporate strategy to narrow its focus strictly to copper, iron ore, lithium, and aluminum, the termination of these development and marketing rights represents a step back from a massive undeveloped mineral deposit. Though Rio Tinto remains the largest shareholder in the project, the decision highlights operational adjustments that may have prompted near-term caution among some market participants.

Ultimately, the confluence of a sharp sell-off in the broader materials sector, falling industrial metal prices due to geopolitical friction, and rising global bond yields created a challenging environment for Rio Tinto. Despite strong underlying fundamentals built on its high-profile copper and iron ore assets, the macro-driven risk-off session triggered the observed intraday volatility and downward trajectory.

Technical Analysis of Rio Tinto PLC (RIO)

Technically, Rio Tinto PLC (RIO) shows a MACD (12,26,9) value of -1.308, indicating a sell signal. The RSI at 33.470 suggests neutral condition and the Williams %R at 97.715 suggests oversold condition. Please monitor closely.

Fundamental Analysis of Rio Tinto PLC (RIO)

Rio Tinto PLC (RIO) is in the Mineral Resources industry. Its latest annual revenue is $57.64B, ranking 2 in the industry. The net profit is $9.97B, ranking 1 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Buy, with an average price target of $100.03, a high of $125.00, and a low of $68.00.

More details about Rio Tinto PLC (RIO)

Company Specific Risks:

- Depressed Iron Ore Prices and Weak Chinese Demand: Rio Tinto's core earnings driver remains highly vulnerable to structural weakness in the Chinese steel sector, with month-to-date iron ore prices slipping approximately 8.3% toward $101 per tonne and Chinese steel mills limiting purchases only to immediate needs.

- Weak Technical Sell Signals and Momentum Deterioration: The stock has entered a negative short-to-medium-term technical posture, trading below major short-term moving averages with deeply negative oscillator indicators (CCI and Stochastic RSI) that signal strong intraday selling pressure.

- Loss of Strategic Assets and Marketing Rights: The company's sudden strategic shift to exit its option to operate Sovereign Metals’ Kasiya rutile-graphite project in Malawi forces it to forfeit vital product marketing rights for over 40% of the project's future output, raising concerns over its long-term critical minerals pipeline.

- Execution and Capital Allocation Risks in Transition: Pivoting away from mature, high-margin iron ore toward high-cost green tech ventures and battery metals (such as lithium and the $1.5 billion AP60 aluminum expansion) increases the company's capital intensity, near-term operational risk, and vulnerability to long execution lead times.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.