BHP Group Ltd Stock (BHP) Moved Down by 4.05% on Jul 8: Drivers Behind the Movement

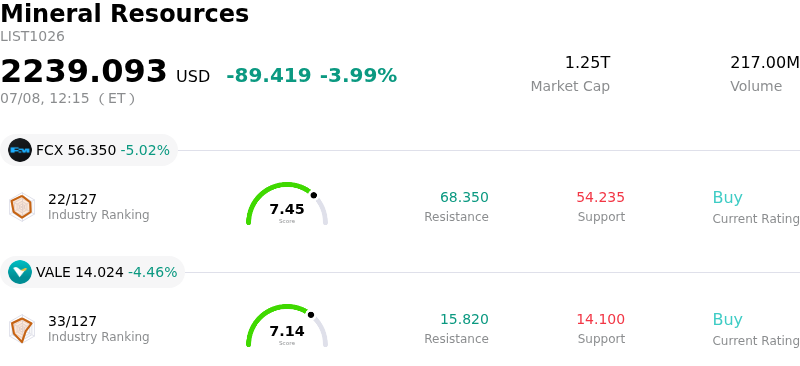

BHP Group Ltd (BHP) moved down by 4.05%. The Mineral Resources sector is down by 3.99%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Freeport-McMoRan Inc (FCX) down 5.02%; Vale SA (VALE) down 4.46%; Rio Tinto PLC (RIO) down 4.39%.

What is driving BHP Group Ltd (BHP)’s stock price down today?

Significant intraday volatility and downward pressure on BHP Group shares have materialized due to a combination of localized operational disruptions, shifting labor dynamics, and broader commodity market corrections.

The most immediate domestic headwind is the looming threat of industrial action at Western Australia's Port Hedland, which serves as the world's largest bulk iron ore export terminal. A coalition of local unions announced a planned strike after months of wage and condition negotiations failed to yield an agreement. Given Port Hedland's critical role in blending and loading BHP's massive iron ore output, any prolonged operational stoppage carries substantial financial risk. Prior warnings from management indicate that even a temporary halt at the terminal could incur exorbitant daily losses. This labor friction introduces unwanted execution risk, especially as the company is currently navigating a major executive leadership transition.

Simultaneously, pressure on BHP's core revenue generators is intensifying as key global commodity prices soften. Following a period of exceptional gains earlier this year, prices for both copper and iron ore have retreated from their recent peaks. Iron ore is steadily trending downward toward psychological support levels, driven by cooling demand from the Chinese property sector, slowing steel production, and persistent macroeconomic inflation concerns. Additionally, efforts by China’s state-backed purchasing body to negotiate lower raw material costs for its steel mills have further dampended the pricing outlook for major global mining firms. Copper futures have also pulled back as broader market optimism cools, directly impacting BHP's near-term earnings potential.

Compounding these external headwinds, internal capital allocation and project execution concerns continue to weigh on investor sentiment. While the company recently signed a long-term contract to advance its South Australian copper expansion, markets remain highly sensitive to development costs. This sensitivity is heightened by the massive write-down and production delay previously announced at the Jansen potash project. These combined factors have prompted institutional profit-taking and contributed to a notable contraction in valuation multiples, causing the stock to trade lower on the day.

Technical Analysis of BHP Group Ltd (BHP)

Technically, BHP Group Ltd (BHP) shows a MACD (12,26,9) value of -1.078, indicating a sell signal. The RSI at 40.684 suggests neutral condition and the Williams %R at 96.454 suggests oversold condition. Please monitor closely.

Fundamental Analysis of BHP Group Ltd (BHP)

BHP Group Ltd (BHP) is in the Mineral Resources industry. Its latest annual revenue is $51.26B, ranking 3 in the industry. The net profit is $9.02B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $72.58, a high of $91.00, and a low of $50.00.

More details about BHP Group Ltd (BHP)

Company Specific Risks:

- Looming Port Hedland Labor Strike: Workers represented by the Combined Ports Unions have announced an eight-hour strike scheduled for July 16, 2026, following six months of stalled contract negotiations. This industrial action threatens operations at the critical Western Australia iron ore export terminal, with BHP previously estimating that a full terminal shutdown could cost the company up to $83 million (A$120 million) per day in lost exports.

- Severe Project Cost Blowouts and Delays: BHP is experiencing significant execution risk in its long-term growth pipeline, highlighted by a recent review of its flagship Jansen Stage 2 Potash project in Canada. The company has expanded the capital expenditure estimate for Stage 2 by $2 billion—ballooning the total investment to $6.9 billion—alongside a two-year production delay and a massive $2.3 billion asset impairment write-down.

- Margin Compression from Falling Commodity Benchmarks: The company's profitability remains heavily exposed to declining prices for its core commodities. Iron ore has continued its downward trajectory, dropping below $98 a tonne due to soft Chinese industrial and construction demand, while copper futures have also pulled back from their mid-June highs, directly squeezing BHP's near-term operational margins.

- Execution Risk Amid Leadership Transition: The heightened volatility and looming labor tensions coincide with a critical transition in executive leadership, as Brandon Craig officially assumed the role of Chief Executive Officer on July 1, 2026. Managing these industrial disputes and capital-heavy projects during a management handover amplifies operational execution risks.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.