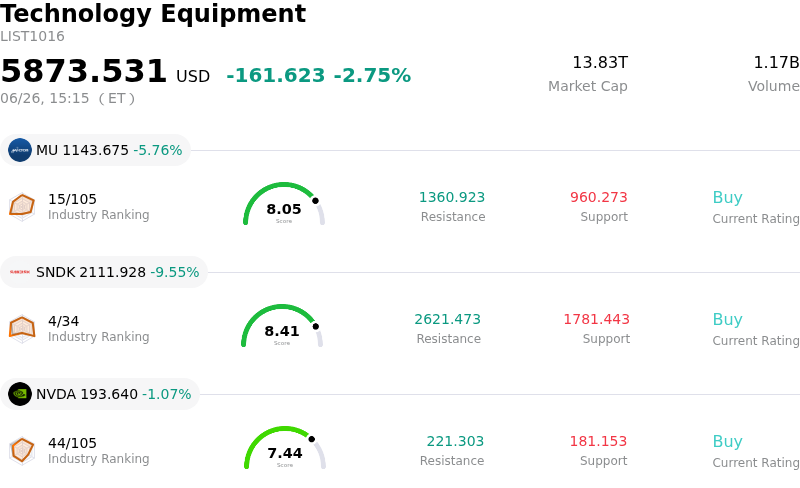

Qualcomm Inc Stock (QCOM) Moved Down by 5.12% on Jun 26: What Investors Need To Know

Qualcomm Inc (QCOM) moved down by 5.12%. The Technology Equipment sector is down by 2.75%. The company underperformed the industry. Top 3 stocks by turnover in the sector: Micron Technology Inc (MU) down 5.76%; SanDisk Corporation (SNDK) down 9.55%; NVIDIA Corp (NVDA) down 1.07%.

What is driving Qualcomm Inc (QCOM)’s stock price down today?

Qualcomm's stock experienced significant downward volatility on Friday, reflecting a "sell-the-news" reaction following its highly anticipated June 24 Investor Day, combined with a broader correction across the semiconductor sector. While the company presented an ambitious long-term roadmap to diversify away from its smartphone roots and capture a larger slice of the artificial intelligence boom, investors ultimately focused on the lengthy timeline required to bring these plans to fruition. This mismatch between immediate valuation expectations and distant revenue realization drove profit-taking.

A primary driver of the downward pressure is the execution gap associated with Qualcomm's new AI data center offerings. Although management outlined a major push into data center AI chips, including a multi-generation CPU partnership with Meta Platforms, the actual chips powering these initiatives do not yet exist in shipping form. For instance, the newly announced Dragonfly architecture is not slated for commercial production until late 2028. This long development cycle leaves Qualcomm highly vulnerable to intermediate smartphone market cyclicality before these data center catalysts can generate meaningful cash flows.

The delay in AI-related revenue diversification has magnified concerns over Qualcomm's core smartphone business, which still accounts for nearly two-thirds of its product revenue. The handset segment continues to face structural headwinds, including supply-chain constraints, inflation in memory chips, and weakness in key Chinese markets. Furthermore, the company faces client attrition risks as major customers like Apple progress with plans to develop their own in-house modems. These near-term headwinds contrast sharply with the distant growth promises of its data center initiatives.

Additionally, some market participants expressed caution regarding Qualcomm’s announced acquisition of AI software company Modular. While strategically aimed at building a robust software moat to compete with established giants like Nvidia, the substantial purchase price has triggered concerns over potential margin compression, increased integration costs, and near-term share dilution.

Finally, macroeconomic pressures and broader market dynamics amplified the stock's slide. Stronger-than-expected economic data has recently fueled worries of sustained higher interest rates, prompting institutional investors to rotate out of high-multiple technology and AI growth stocks. Given that Qualcomm's stock had run up significantly ahead of the Investor Day, the combination of macroeconomic de-risking and localized profit-taking triggered a sharp reversal in short-term momentum.

Technical Analysis of Qualcomm Inc (QCOM)

Technically, Qualcomm Inc (QCOM) shows a MACD (12,26,9) value of -7.436, indicating a neutral signal. The RSI at 47.694 suggests neutral condition and the Williams %R at 69.384 suggests sell condition. Please monitor closely.

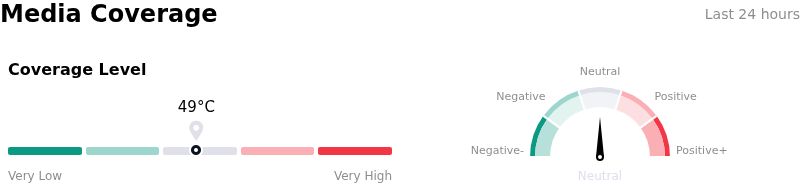

Media Coverage of Qualcomm Inc (QCOM)

In terms of media coverage, Qualcomm Inc (QCOM) shows a coverage score of 49, indicating a moderate level of media attention. The overall market sentiment index is currently in neutral zone.

Fundamental Analysis of Qualcomm Inc (QCOM)

Qualcomm Inc (QCOM) is in the Technology Equipment industry. Its latest annual revenue is $44.28B, ranking 5 in the industry. The net profit is $5.54B, ranking 7 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as Hold, with an average price target of $206.78, a high of $300.00, and a low of $100.00.

More details about Qualcomm Inc (QCOM)

Company Specific Risks:

- Speculative Roadmap and Delayed Product Delivery: Although Qualcomm set an ambitious $15 billion data center revenue target for FY2029 during its June 24, 2026 Investor Day, the core chips driving this projection, such as the Dragonfly C1000 server CPU and Dragonfly AI300 inference accelerator, are not scheduled for production and shipping until 2028. This creates a massive multi-year gap where investors must underwrite a speculative roadmap with no near-term revenue to offset high development costs.

- Immediate Equity Dilution via Modular Inc. Acquisition: To support its AI software strategy, Qualcomm announced a $3.92 billion acquisition of software company Modular Inc. on June 24, 2026. Funded entirely via private placement of up to 19.2 million shares of common stock, the deal introduces immediate equity dilution risks for existing shareholders alongside substantial integration and regulatory hurdles.

- Persistent Weakness in the Core Handset Segment: Despite aggressive long-term diversification plans, Qualcomm's near-term financial health remains highly dependent on its core smartphone segment. In the most recent financial disclosures, handset revenues fell 13% year-over-year to $6.024 billion, severely dragged down by memory supply constraints and weakening demand from Chinese original equipment manufacturers (OEMs).

- Intense Competitive Barriers Against Dominant Incumbents: Entering the scale-out data center CPU and AI inference market forces Qualcomm to directly challenge NVIDIA's massive hardware dominance and entrenched CUDA software ecosystem. Analysts warn that attempting to break NVIDIA's software lock-in represents a high-risk, capital-intensive venture with no guarantee of successful market share capture, even with the newly announced Modular acquisition.

This article may include AI-generated content that is human-reviewed, which is for reference and general information purposes only and does not constitute investment advice.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.